Rare earth elements have become the backbone of modern technology, yet most investors overlook the opportunities hiding in plain sight. The rare earth elements market is experiencing unprecedented shifts driven by geopolitical tensions and surging demand from clean energy sectors.

At Natural Resource Stocks, we’ve identified critical supply gaps that are reshaping investment landscapes. This guide breaks down where the real opportunities lie for portfolio builders.

Where the World Gets Its Rare Earths

The Supply Concentration Problem

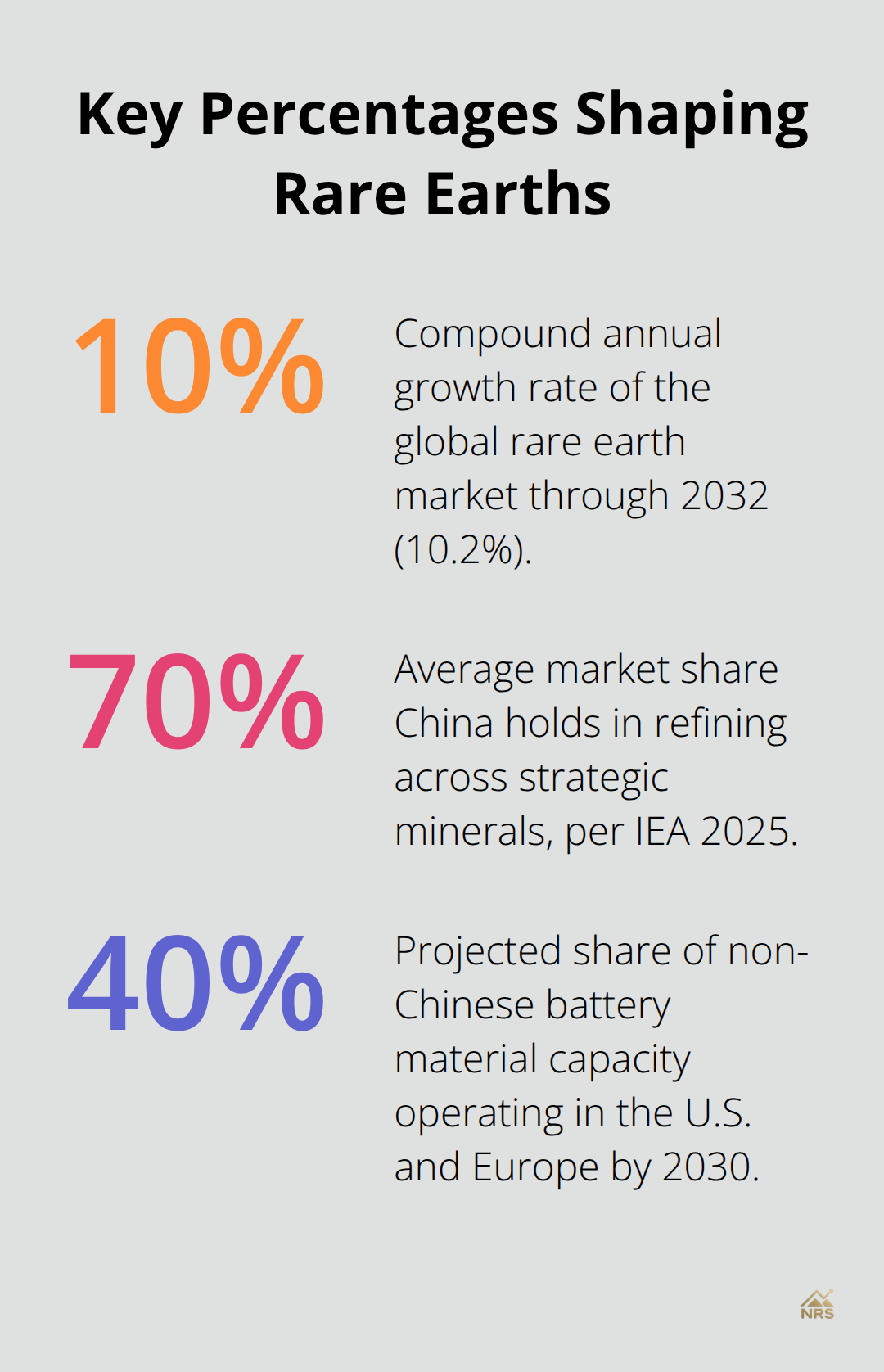

The rare earth elements market operates within a supply system so concentrated it makes oil dependency look diversified. China accounts for roughly 70% of global rare earth magnet production as of 2024, with Myanmar providing most of the remainder. This duopoly controls initial extraction, but the real bottleneck sits downstream. China handles approximately 85% to 90% of all rare earth refining and processing, converting raw ore into usable materials for manufacturers. That processing dominance extends further into finished goods-China now produces about 94% of the world’s permanent magnets, the components that power electric vehicle motors, wind turbines, and defense systems.

Market Growth and the Pricing Challenge

The global rare earth elements market reached USD 3.39 billion in 2023 and will hit USD 8.14 billion by 2032, according to Fortune Business Insights, representing a compound annual growth rate of 10.2%. This growth masks a critical vulnerability: supply concentration creates price volatility that investors struggle to track. Unlike oil or gold, rare earth elements lack a single transparent price benchmark. Spot prices fluctuate across regional markets and customer relationships, making it difficult for portfolio builders to gauge true market movements.

Investors monitor supply-demand trends and policy announcements instead of chasing prices, since these signals often reprice markets before spot quotations shift. When China restricted exports on seven heavy rare earth elements in April 2025, European prices spiked to six times Chinese levels within weeks-a move no commodity index captured in real time.

Heavy Rare Earths and Production Timelines

Heavy rare earth elements command premium prices for defense and high-performance applications, yet they come from even fewer sources than light rare earths. Lynas Rare Earths in Australia reported a 92% increase in mineral resources and a 63% increase in reserves at its Mt. Weld mine in 2024, though this Australian capacity still represents only a fraction of global demand. Energy Fuels completed pilot-scale production of dysprosium oxide in Utah, signaling early-stage progress toward domestic US heavy rare earth output.

The challenge investors face is that turning known reserves into commercial production requires eight years on average for permitting, construction, and ramping. During that window, policy shifts can destroy project economics. China’s December 2025 expansion of export controls now covers internationally made products containing Chinese-sourced rare earth materials, effectively extending Beijing’s leverage beyond its own borders.

Policy Risk and Investment Implications

This regulatory escalation forces Western manufacturers to secure non-Chinese supply chains or face production delays. For investors, demand for diversified mining and processing capacity will remain strong for years, but individual project timelines and political risk will dominate stock performance far more than underlying metal prices. The next section examines which emerging producers and Western alternatives offer the most compelling opportunities to capitalize on this structural shift.

How China’s Export Controls Reshape Western Investment Strategy

The April and December 2025 Policy Escalation

China’s export restrictions moved from theoretical risk to operational reality in 2025. In April, China’s export restrictions on heavy rare earth elements took effect, and European prices immediately jumped to six times Chinese levels. Then in December, China expanded controls to require licenses for parts, components, and assemblies containing Chinese rare earth materials, effectively weaponizing supply chains across borders. This isn’t posturing-2024 saw China export 58,000 tonnes of rare earth magnets globally, and licensing delays now threaten revenues and employment across industrial value chains from automotive to aerospace.

For investors, these controls signal that diversification away from Chinese supply is no longer optional but mandatory for companies dependent on rare earth inputs.

Why Concentration Risk Demands Portfolio Action

The IEA Global Critical Minerals Outlook 2025 confirms China dominates refining for 19 of 20 strategic minerals with an average 70% market share, making concentration risk unavoidable without deliberate portfolio positioning. A single policy announcement can halt production across multiple continents. Western manufacturers increasingly require certified non-Chinese supply chains for government contracts, creating sustained demand that will outlast any temporary trade friction.

This structural shift means investors who position early in alternative supply chains capture both price appreciation and the stability premium that comes from serving supply-constrained markets.

The Timeline Challenge for New Producers

MP Materials signed a Defense Department contract to expand US rare earth magnet capacity, while Energy Fuels progressed dysprosium oxide production in Utah. Lynas in Australia expanded reserves by 63% in 2024, yet these projects face an eight-year average timeline from permitting to commercial production. The real investment opportunity lies in supporting companies already past early exploration stages-those with pilot operations, government backing, or joint ventures that can reach production within two to three years rather than waiting for greenfield projects to mature. Companies operating at pilot scale or in joint ventures with established manufacturers move faster and face lower execution risk than pure exploration plays.

Where Investment Capital Flows Next

Western governments now fund rare earth infrastructure as national security priorities, not market-driven commodities. This policy backing removes traditional project finance constraints and accelerates timelines for companies with credible pathways to production. Investors who track government procurement announcements and defense department contracts identify opportunities before equity markets price them in. The companies positioned to capture this demand shift are those already producing materials or components, not those still years away from first ore.

The next section examines which specific producers and supply chain alternatives offer the most compelling risk-adjusted returns as Western manufacturers race to secure non-Chinese sources.

Where to Find Production Outside China

The Near-Term Producers Setting the Pace

MP Materials operates the Mountain Pass mine in California, the only active rare earth mining operation in the United States, and signed a Defense Department contract in 2025 to expand magnet production capacity using Texas-based facilities and California processing. This vertically integrated approach matters because it compresses timelines-the company controls mining, refining, and magnet manufacturing within the US supply chain, eliminating the multi-year delays typical of greenfield projects. Energy Fuels completed pilot-scale dysprosium oxide production in Utah, a heavy rare earth critical for defense applications and EV motors. These pilot operations signal progress, but scaling to commercial volumes requires capital deployment and equipment validation that typically takes 24–36 months rather than the eight-year average for entirely new mines.

Resource Expansion and Single-Asset Risk

Lynas Rare Earths in Australia expanded mineral resources by 92% and reserves by 63% at Mt. Weld during 2024, making it the largest rare earth resource outside China. However, Lynas still operates as a single-asset company dependent on one mine, creating concentration risk despite reserve expansion. Arafura Rare Earths in Australia and Ucore Rare Metals in Canada offer diversified geographic exposure, but both remain in advanced development stages rather than production. For investors, the practical distinction is clear-companies already operating pilot facilities or possessing Defense Department contracts move faster and face lower execution risk than pure exploration plays still years from commercial production.

Locked-In Demand From Multiple Sectors

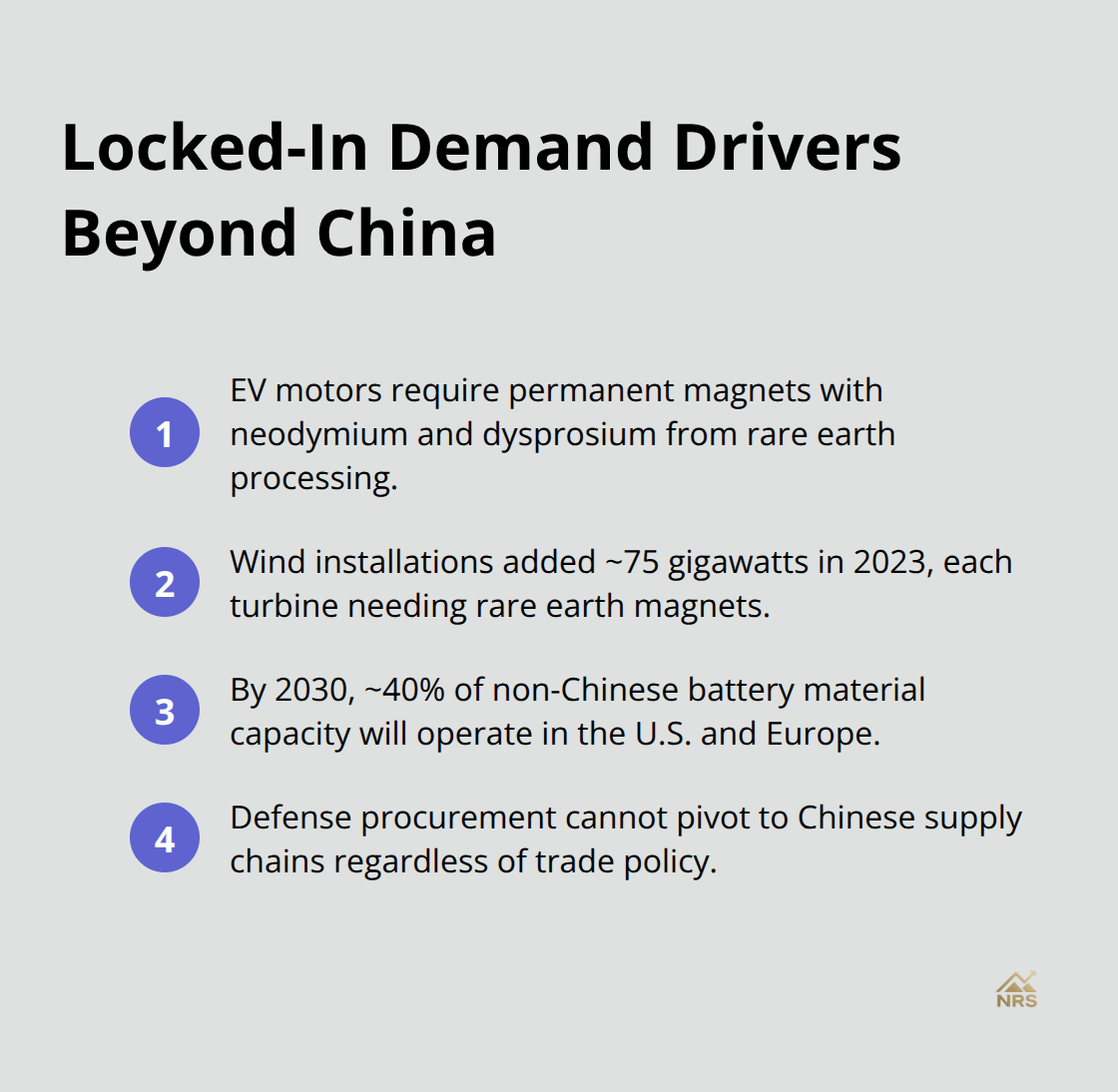

Global electric vehicle sales have continued climbing, with each EV motor requiring permanent magnets containing neodymium and dysprosium sourced from rare earth processing. Wind turbine installations globally added approximately 75 gigawatts of capacity in 2023 alone, and each turbine’s permanent magnet generator demands rare earth magnets. The IEA projects that by 2030, roughly 40% of non-Chinese battery material capacity will operate in the United States and Europe combined, signaling structural demand for Western-sourced materials. This isn’t cyclical demand vulnerable to economic downturns-defense procurement for fighter jets, missiles, and military electronics depends on rare earth magnets and cannot shift to Chinese supply chains regardless of trade policy.

Strategic Positioning for Supply-Constrained Markets

Companies positioned to supply defense contractors, EV manufacturers, and wind turbine producers have locked-in demand visibility extending five to ten years forward, a rarity in commodity markets. The practical investment approach focuses on producers with government contracts, pilot-scale operations approaching commercialization, or joint ventures with established manufacturers. This strategy avoids speculative exploration companies betting on future discoveries or permitting approvals that may never materialize. Investors who track government procurement announcements and defense department contracts identify opportunities before equity markets price them in, positioning portfolios to capture both price appreciation and the stability premium that comes from serving supply-constrained markets.

Final Thoughts

The rare earth elements market stands at an inflection point where geopolitical reality has replaced theoretical supply risk. China’s export controls in 2025 proved that concentration risk is operational, not hypothetical. Western manufacturers now face a choice between securing non-Chinese supply chains or accepting production delays and regulatory uncertainty, and this structural shift creates a multi-year window where companies positioned to supply defense contractors, EV manufacturers, and renewable energy producers command pricing power and demand visibility that commodity markets rarely offer.

The investment case rests on three concrete realities: the eight-year timeline to bring new mines online means existing producers and pilot-scale operations will dominate supply for years; government backing removes traditional project finance constraints and accelerates timelines for companies with credible production pathways; and locked-in demand from defense procurement, electric vehicle motors, and wind turbines creates revenue visibility extending five to ten years forward. Portfolio positioning should prioritize producers already operating pilot facilities or holding Defense Department contracts over pure exploration plays, since companies with joint ventures or established manufacturing partnerships move faster and face lower execution risk than greenfield projects still years from commercialization.

The rare earth elements market will remain volatile and policy-driven for the foreseeable future, and investors who understand supply chain timelines and monitor geopolitical developments gain an edge over those chasing spot prices. Natural Resource Stocks provides expert analysis on how policy shifts and supply dynamics reshape investment opportunities across resource sectors, helping you identify which companies will reward investors who act before consensus catches up.