Platinum prices swing wildly based on forces most investors overlook. Supply constraints in South Africa, shifts in industrial demand, and currency movements all play outsized roles in determining where this metal trades.

At Natural Resource Stocks, we’ve identified the platinum price drivers that actually matter for your portfolio. Understanding these factors gives you an edge when positioning for what comes next.

Platinum Supply Tightness: The Foundation of Price Strength

The Deficit That Reshapes Global Markets

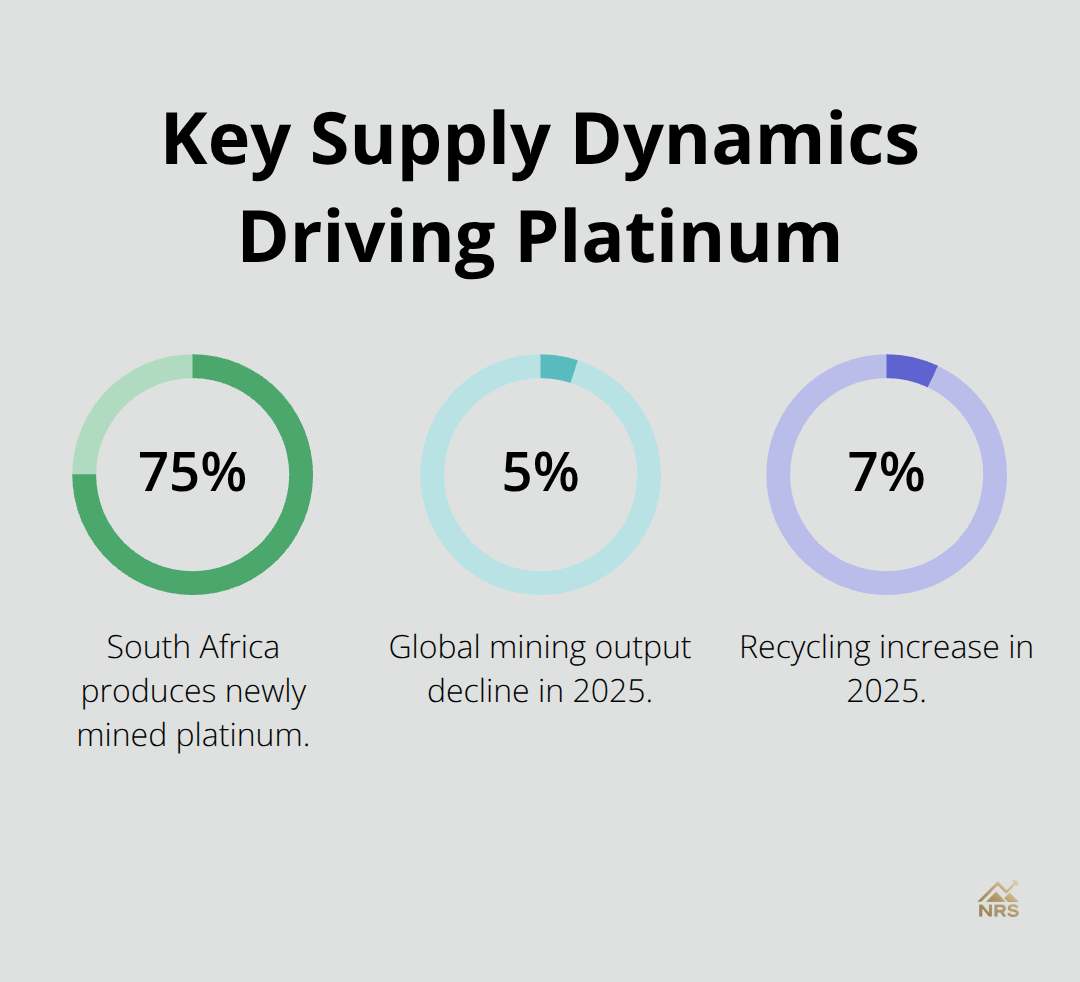

Platinum’s price surge rests on a concrete supply shortage, not speculation. The World Platinum Investment Council reported that the market hit a third consecutive annual deficit in 2025, estimated at 692,000 ounces. Above-ground stockpiles collapsed to just five months of demand cover, down 42 percent from 2024. This structural tightness anchors current pricing because supply cannot flex quickly to meet demand. South Africa produces roughly 75 percent of the world’s newly mined platinum, and that concentration creates real vulnerability. When South African mines face disruptions-whether from labor disputes, power shortages, or equipment failures-global platinum supply takes a hit. Mining output fell 5 percent in 2025 while recycling rose 7 percent, proving that secondary supply cannot offset weakening primary production.

The deficit means the market consumes more platinum than it produces, a pattern the World Platinum Investment Council forecasts will persist through 2029, averaging roughly 727,000 ounces annually. For investors, this deficit translates directly into upward pressure on prices because inventories shrink to meet current demand.

How Automotive and Jewelry Demand Shifted in 2025

Autocatalysts still drive the largest share of platinum consumption at roughly 41 percent of total demand, but the composition of that demand has shifted dramatically. Chinese automakers and consumers now dominate the market. Platinum jewelry demand in China surged 26 percent in the first quarter of 2025, according to the World Platinum Investment Council, as buyers shifted toward platinum as a more affordable alternative to gold. India’s platinum jewelry market strengthens as incomes rise, creating a second growth engine beyond automotive. Industrial applications outside of automotive account for 21 percent of demand and include chemical catalysts, petroleum refining, and hydrogen fuel cells. This diversification matters because platinum demand no longer depends solely on car sales trends. Emission standards like Euro 6 and China VI regulations reinforce platinum’s role in catalytic converters, and fuel cell electric vehicles could require twice the platinum per vehicle compared to traditional engines, creating long-term upside potential.

Investment Demand Signals a Structural Market Shift

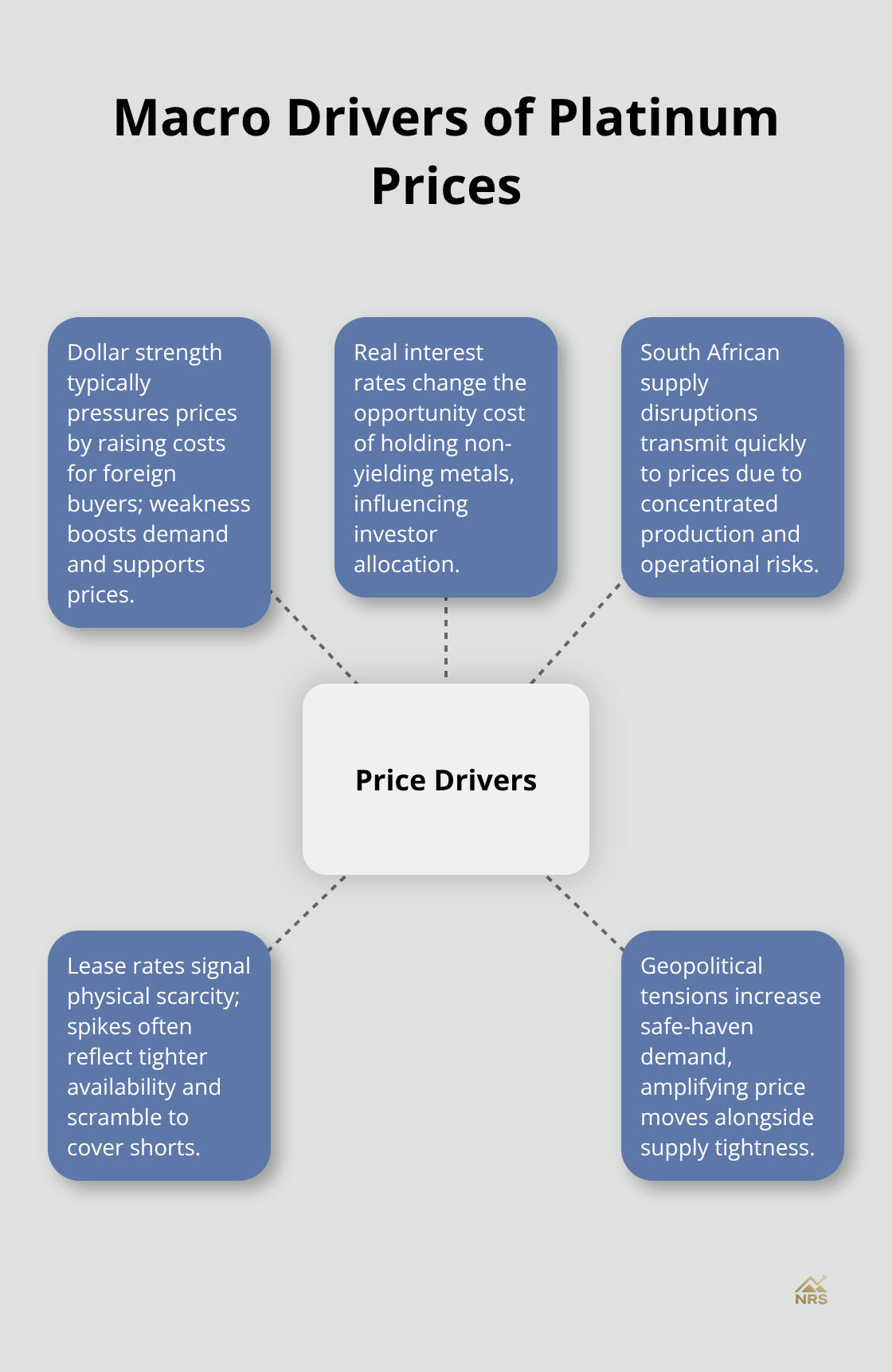

Investment demand tells the real story about market psychology and reveals how platinum is transforming. Investment demand for platinum jumped roughly 300 percent year-over-year in the first quarter of 2025, as investors treated platinum as a safe-haven asset amid market uncertainty. This investor appetite marks a departure from historical patterns and suggests that platinum transitions from a purely industrial metal into an alternative precious metal that competes with gold for portfolio allocation. Lease rates spiked to 12 percent year-to-date in 2025, up from roughly 1 percent in 2024, reflecting tighter physical supply and supporting higher prices. Investors shifted away from leasing toward outright ownership as lease rates climbed, further tightening available supply. This behavioral shift matters because it locks metal into investment portfolios rather than keeping it available for industrial users, which intensifies the supply squeeze. The next section examines how geopolitical tensions and economic forces amplify these supply and demand pressures.

Geopolitical and Economic Factors Affecting Platinum Prices

South Africa’s Mining Dominance Creates Structural Vulnerability

South Africa’s grip on global platinum supply creates a structural vulnerability that directly moves prices. The country produces roughly 75 percent of the world’s newly mined platinum, meaning disruptions there cascade through the entire market. In 2025, South African platinum group metals output fell 24.1 percent year-over-year in April alone, according to data from Novus Group, with seven of twelve mining divisions posting declines. Equipment breakdowns, supply chain failures, and rain-related outages compound the operational chaos. When these disruptions hit, lease rates spike because traders scramble to cover short positions. Lease rates hit 22.7 percent in June 2025 before settling around 11-12 percent year-to-date, reflecting how quickly physical scarcity translates into borrowing costs.

Labor Disputes and Supply Shocks

Labor disputes and supply shocks remain the wildcard that reshapes platinum prices overnight. The 2014 platinum strikes cut roughly 40 percent of global output, a reminder that wage negotiations or work stoppages can reshape prices within weeks. For investors, tracking South African mining reports monthly matters more than following broader commodity trends. Watch for union activity announcements and mining division production reports from companies operating in South Africa, as these signal incoming supply shocks before prices react. A single labor action can tighten lease rates and push prices higher across the entire market within days.

Currency Strength and Dollar Dynamics

Currency movements operate as powerful price drivers that most retail investors underestimate. A stronger US dollar typically pressures platinum prices because international buyers face higher costs when converting their local currency. Conversely, dollar weakness makes platinum cheaper for foreign buyers, boosting demand and supporting prices. Monitor the DXY dollar index as a leading indicator alongside South African mine output reports. When the dollar weakens, platinum typically responds positively within one to three months as foreign demand accelerates.

Interest Rates and Inflation Expectations

Real interest rates matter equally because platinum, like gold, competes with interest-bearing assets for portfolio space. When real rates rise, the opportunity cost of holding non-yielding platinum increases, weighing on prices. Lower interest rates could support ongoing demand for platinum as portfolio diversification in 2026 and beyond. Inflation expectations also influence behavior because investors seeking inflation hedges rotate into platinum alongside gold and energy commodities. Track the yield spread between nominal and inflation-protected US Treasury bonds as a proxy for inflation expectations. A widening spread suggests rising inflation expectations, which historically supports higher platinum prices.

Connecting Macro Forces to Market Movement

These macroeconomic forces interact with supply tightness, meaning investors who monitor both South African mine output and Federal Reserve policy statements gain a clearer view of price direction than those tracking platinum in isolation. Geopolitical tensions amplify price movements because they increase demand for safe-haven assets, while rising real rates can offset supply-driven gains. The next section examines how emerging technologies and shifting demand patterns reshape platinum’s long-term price trajectory.

Platinum’s Next Growth Phase

Fuel Cells and Emission Standards Shape Demand

Hydrogen fuel cell technology and electric vehicle adoption reshape platinum demand trajectories, but not in the way most investors assume. Fuel cell electric vehicles require roughly twice the platinum per unit compared to traditional internal combustion engines, according to the World Platinum Investment Council, yet widespread commercial adoption remains years away. What matters now is that China’s 2026 emission standards will keep internal combustion engines and hybrid vehicles dominant through the decade, sustaining autocatalyst demand and preventing the cliff many feared. This regulatory reality means platinum consumption from automotive applications will remain robust even as EV penetration rises globally.

Jewelry Demand Accelerates Across Asia

Chinese platinum jewelry demand grew 26 percent in the first quarter of 2025 as consumers traded gold for platinum at lower price points, and this trend accelerates if prices stabilize. India’s jewelry market adds another growth vector as rising incomes drive purchases across major metropolitan areas. These two markets now represent the primary expansion engines for platinum consumption outside of automotive catalysts.

Industrial Applications Provide Demand Diversification

Industrial applications beyond automotive-including chemical catalysts, petroleum refining, and emerging hydrogen infrastructure projects-account for roughly 21 percent of current demand and provide diversification away from cyclical auto sales. These sectors expand as refineries upgrade equipment and companies invest in hydrogen production capacity, creating steady baseline demand that buffers against automotive downturns.

Supply Deficits Force Inventory Depletion

The structural deficit persisting through 2029 means platinum cannot satisfy all these demand streams without drawing down above-ground inventories further. This is not theoretical. Above-ground stockpiles currently cover less than five months of demand, and deficits averaging 727,000 ounces annually will deplete remaining reserves within years. Investors positioning now benefit from the lag between rising demand signals and market recognition that supply cannot respond.

Practical Indicators for Tracking Demand Shifts

Track quarterly platinum jewelry processing volumes in China and India monthly production reports from refineries as leading indicators of demand acceleration. Monitor hydrogen project announcements from major industrial companies and energy firms, as these signal future platinum requirements before prices reflect the shift. Currency weakness in the Indian rupee and Chinese yuan also matters because it affects jewelry demand elasticity-lower local currency values reduce purchasing power and suppress demand temporarily. The combination of persistent supply tightness, rising jewelry demand, and emerging industrial applications creates a multi-year tailwind for platinum prices that extends well beyond near-term volatility.

Final Thoughts

Platinum’s price movement rests on three interconnected forces that we track continuously. Supply deficits averaging 727,000 ounces annually through 2029 create the foundation for sustained price strength, while South African production volatility introduces unpredictability that amplifies price swings. Automotive demand remains robust despite EV adoption because emission standards keep internal combustion engines dominant through this decade, and jewelry consumption in China and India adds growth momentum that extends beyond cyclical auto sales.

Investment demand shifted dramatically in 2025, with investors treating platinum as a safe-haven asset rather than a purely industrial metal, fundamentally changing how this market behaves. Above-ground inventories covering less than five months of demand mean prices face structural support as deficits continue depleting reserves. Monitor South African mining output reports monthly and track lease rate movements as real-time indicators of physical scarcity, while currency weakness in the dollar typically supports platinum within one to three months.

The practical edge comes from combining multiple signals rather than relying on any single indicator. Watch Chinese platinum jewelry processing volumes quarterly, track hydrogen project announcements from major industrial firms, and cross-reference these demand signals against South African production data and lease rate trends. Visit our platform to access detailed insights into how the platinum price drivers we’ve outlined reshape resource prices across metals and energy sectors.