Nuclear power is experiencing a historic resurgence as governments worldwide pivot toward carbon-free energy. This shift is creating unprecedented demand for uranium, the fuel that powers these reactors.

At Natural Resource Stocks, we’re tracking how supply constraints and geopolitical factors are reshaping the uranium market. Understanding the uranium demand outlook is essential for investors positioning themselves in this sector.

Nuclear Power Shifts From Niche to Strategic Priority

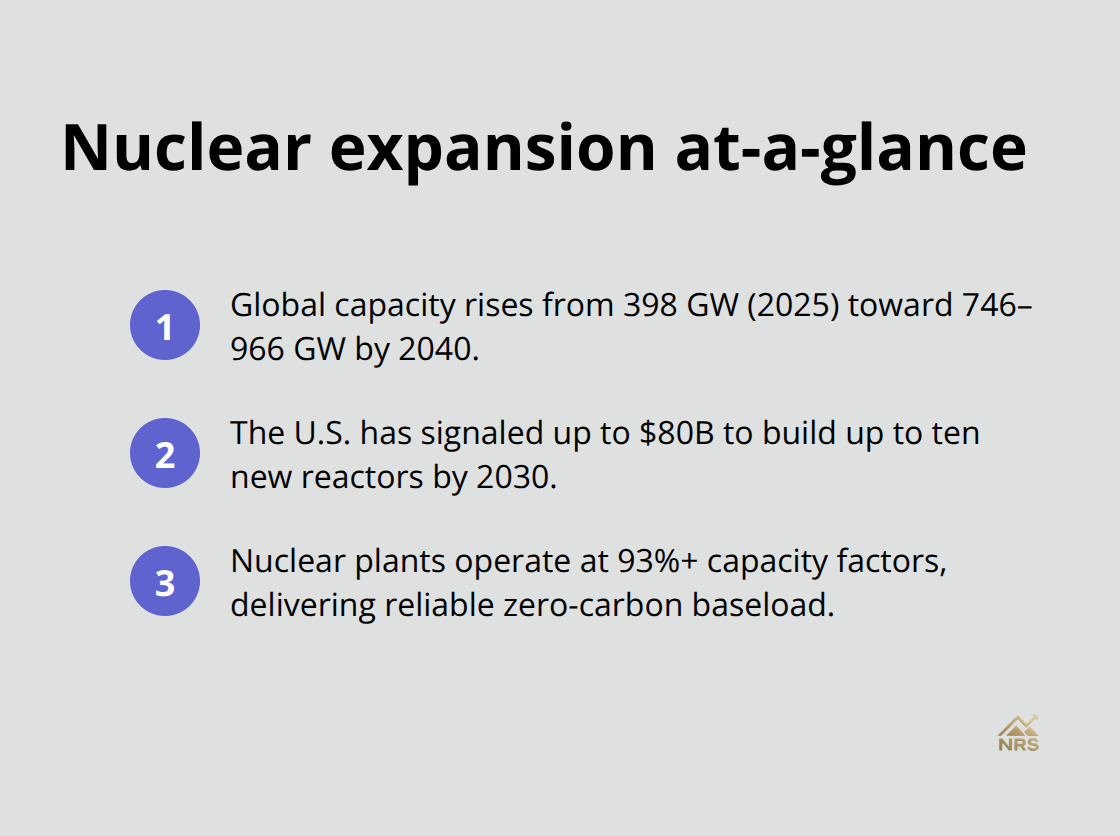

Global nuclear capacity stood at 398 gigawatts as of June 2025, but expansion accelerates rapidly ahead. The World Nuclear Association’s 2025 outlook projects nuclear capacity will reach 746 gigawatts by 2040 under the Reference Scenario, with the Upper Scenario reaching 966 gigawatts. Governments are backing these projections with concrete policy and funding rather than rhetoric alone. The U.S. government has signaled up to 80 billion dollars to construct up to ten new reactors, with construction potentially starting by 2030.

These commitments carry timelines and allocated capital. Nuclear provides firm, around-the-clock, zero-carbon electricity that anchors a grid increasingly dependent on intermittent renewables. Nuclear plants globally maintain capacity factors above 93 percent, meaning they operate near maximum output consistently.

Why Baseload Power Matters Now More Than Ever

U.S. electricity demand will grow roughly 9 percent by 2028 and as much as 57 percent by 2050, driven by artificial intelligence, data centers, electrification of vehicles, and manufacturing expansion. Current nuclear capacity already supplies roughly half of America’s carbon-free electricity, yet this falls short of coming demand without expansion. No other zero-carbon source delivers the consistent, dense power that modern grids require at the necessary scale. Nuclear plants operate reliably when wind turbines sit idle and solar panels produce nothing at night-a reality that matters enormously as data centers and AI infrastructure demand stable baseload power around the clock.

Geopolitical Pressure Reshapes Energy Strategy

Nations now view energy independence and nuclear capacity as strategic assets, particularly following supply disruptions tied to the Russia-Ukraine conflict. This perspective explains why China continues aggressive uranium stockpiling and why Western governments are reshoring fuel-cycle capabilities rather than relying on Russian enrichment. Energy security concerns have replaced climate sentiment as the primary driver of nuclear expansion in many regions. Governments treat uranium supply chains with the same urgency they apply to military procurement.

The convergence of rising electricity demand, grid reliability requirements, and geopolitical competition has transformed nuclear from a debated option into a policy priority that transcends political cycles. This shift creates immediate pressure on uranium supply chains, which now face the challenge of meeting demand that will accelerate sharply over the next decade.

Where Uranium Demand Accelerates Fastest

Global reactor uranium requirements reached approximately 68,920 tonnes in 2025, according to the World Nuclear Fuel Report 2025. That figure climbs to just over 150,000 tonnes annually by 2040 under the Reference Scenario, representing more than a twofold increase in demand within fifteen years. The Upper Scenario pushes demand to over 204,000 tonnes by 2040.

Small Modular Reactors Drive Higher Enrichment Needs

Small modular reactors represent the first major demand accelerator. These reactors require higher enrichment levels, specifically HALEU at 5 to 20 percent enrichment, compared to traditional reactors. Centrus Energy inaugurated America’s first new enrichment plant since 1954 in 2023 and received roughly 900 million dollars from the U.S. government to build domestic HALEU capacity. The company also holds approximately 2.3 billion dollars in LEU purchase commitments from utilities. This shift toward higher enrichment creates new uranium processing requirements that expand demand beyond simple volume increases.

Data Centers Demand Continuous Baseload Power

Data centers form the second demand source and operate with relentless power requirements. U.S. electricity demand will surge roughly 9 percent through 2028 and potentially 57 percent through 2050, driven primarily by artificial intelligence infrastructure, cloud computing expansion, and vehicle electrification. Data centers operate continuously and require stable baseload power that only nuclear provides consistently. Tech companies increasingly recognize that renewable-only strategies cannot support their computational requirements without nuclear backing. This sector alone will consume substantial uranium volumes as companies lock in long-term power contracts with nuclear operators.

Supply Deficits Create Immediate Market Pressure

The third and most immediate pressure stems from the supply deficit. Global uranium production in 2024 reached 166 million pounds, falling short of the 170 million pounds consumed that year. This shortfall persists despite rising prices that tripled in recent years. Thunder Said Energy’s supply model projects the market will remain adequately supplied from 2026 through 2030 as demand climbs from 170 million pounds annually to 210 million pounds by 2030, but warns that project execution risk remains genuine. In 2026, approximately 20 of 75 uranium projects in the pipeline faced delays, mirroring capital-project risks seen across LNG development.

Geographic Supply Concentration and Production Expansion

Kazakhstan currently supplies roughly 40 percent of global output, with Canada representing 20 percent and expected to double production over the coming decade. Namibia and Australia each contribute roughly 10 percent, while the United States is projected to grow from near-zero production to approximately 10 million pounds annually within ten years. This geographic concentration means supply disruptions in any major producing region ripple across global markets. Utilities deferred significant uranium contracting throughout 2025, creating pent-up demand that industry expects to materialize in 2026. Spot uranium ranged from 63 dollars to 83 dollars per pound in 2025, with term prices beginning to rise after months of stagnation. This price movement signals utilities are willing to pay higher prices for long-term supply contracts, confirming that fundamental tightness in the market will persist for years. As utilities rebuild inventories and secure long-term supply agreements, the uranium market enters a phase where supply constraints will test the ability of producers to meet accelerating demand.

How Geopolitical Tensions Reshape Uranium Markets

Kazakhstan’s dominance over global uranium production creates vulnerability that geopolitical events exploit immediately. The country supplied roughly 40 percent of the world’s uranium in 2024, making it the single largest producer by a massive margin. When Kazakhstan experiences political instability, currency fluctuations, or policy shifts, uranium prices respond sharply because buyers have limited alternatives. Canada ranks second with approximately 20 percent of global supply, but a 40-percent dependency on one nation means supply shocks there cascade across every reactor fleet worldwide.

How the Russia-Ukraine Conflict Exposed Supply Chain Risks

The Russia-Ukraine conflict demonstrated this vulnerability directly. Since March 2022, geopolitical and geoeconomic factors tied to that war have affected uranium demand and the entire supply chain (conversion, enrichment, and fabrication). Western nations watched Russian enrichment capacity supply their reactors and realized this arrangement represented an unacceptable strategic risk. The U.S. government responded decisively in May 2024 by banning uranium imports from Russia, forcing utilities to source from other producers and accelerating domestic enrichment investments. This shift created immediate pricing pressure because alternative suppliers cannot instantly replace Russian volumes.

Nations Compete for Uranium as Strategic Asset

Nations now treat uranium with the same strategic importance they apply to military hardware. China aggressively stockpiles uranium for its expanding reactor program, removing supply from open markets and locking in future production. The U.S. government explores a Strategic Uranium Reserve through mechanisms including equity investments in mining projects, offtake arrangements, or price floors to support domestic supply. A Section 232 review focused on uranium and other critical materials will release findings in the first half of 2026, assessing vulnerabilities and likely prompting additional policy responses. This shift toward government-directed uranium procurement means market pricing no longer reflects pure supply and demand dynamics. When governments compete for supply alongside utilities, prices rise and spot availability tightens.

Critical Minerals Status Signals Long-Term Policy Commitment

Uranium earned placement on the U.S. Geological Survey’s Critical Minerals list in November 2024, signaling that Washington views uranium supply resilience as essential infrastructure. Policy momentum toward reshoring critical materials extends across lithium, rare earths, cobalt, and other supply chains, creating a broader framework that supports upstream uranium investment. This designation reflects a fundamental shift in how policymakers approach resource security. For investors, this means geopolitical events will remain price drivers for years because uranium supply chains now serve dual civilian and strategic national purposes. Tracking policy announcements from the Section 232 review, monitoring permit approvals for domestic mining projects, and watching for Strategic Reserve developments will provide actionable signals about future uranium availability and pricing direction.

Final Thoughts

The uranium demand outlook over the next fifteen years reflects a fundamental shift in how the world powers itself. Uranium consumption will more than double from current levels, driven by nuclear expansion, data center proliferation, and geopolitical competition for energy security. This trajectory rests on concrete government commitments, reactor construction timelines, and utility procurement patterns already underway.

Supply constraints will persist throughout this period because Kazakhstan’s dominance creates vulnerability, Russia-Ukraine disruptions have redirected supply chains, and project execution delays mean new production capacity arrives slower than demand accelerates. The gap between what utilities need and what producers can deliver will widen before it narrows, creating sustained pricing pressure that rewards investors positioned early. The Section 232 review expected in early 2026 will likely trigger additional policy measures supporting domestic supply, while Strategic Reserve discussions will accelerate and permit approvals for new mining projects will unlock production capacity.

Uranium equities have already responded, with major producers gaining roughly 70 percent in 2025 alone, yet the fundamental drivers-AI-driven electricity demand, SMR deployment, government policy support, and supply deficits-remain in their early stages. The uranium demand outlook reflects genuine scarcity meeting accelerating need, and investors should approach this sector with conviction rather than caution. Access expert analysis and market commentary at Natural Resource Stocks to navigate this opportunity effectively.