Nuclear power is experiencing a genuine resurgence. Governments worldwide are committing billions to new reactor construction, and energy security concerns are pushing nations to reduce fossil fuel dependence.

At Natural Resource Stocks, we believe uranium investment opportunities are emerging across multiple sectors-from mining stocks to ETFs. This guide shows you where to look and what factors matter most.

Why Nuclear Demand Is Outpacing Supply Right Now

Demand Projections Signal Massive Growth Ahead

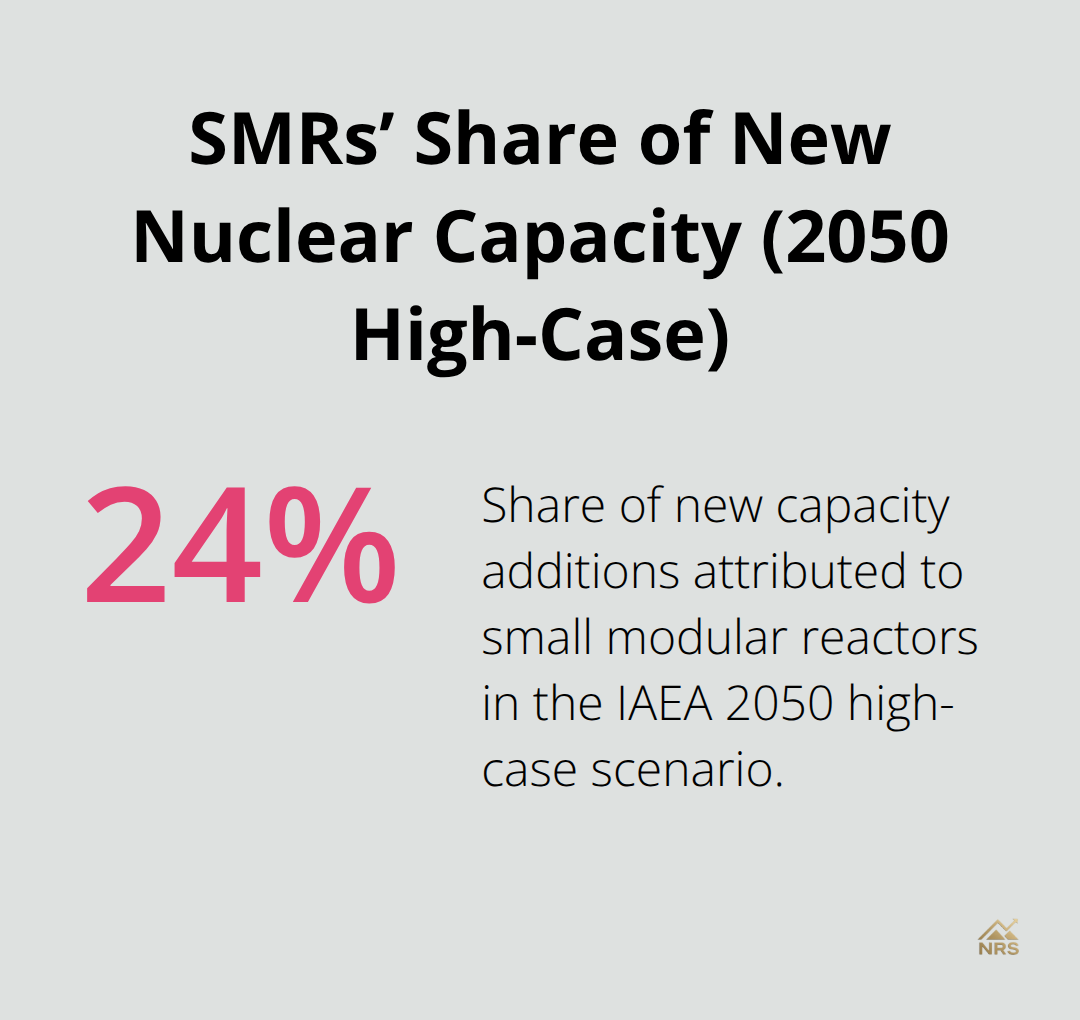

The IAEA’s 2024 projections show nuclear capacity could reach 992 gigawatts by 2050 in the high-case scenario, up from 377 gigawatts today. That represents a 2.6x expansion. Small modular reactors alone will account for 24 percent of new capacity additions in this scenario, fundamentally reshaping how uranium gets consumed. This demand is not theoretical.

As of end-2024, 417 reactors operated globally, with roughly 90 more under construction or on order and 300 plus in proposal stages. China and India are driving much of this growth, with China alone planning massive reactor deployments to meet energy security goals. The International Energy Agency states the nuclear industry must double in size over the next two decades to hit net-zero targets. This isn’t ambition-it’s a hard requirement baked into climate commitments across multiple nations.

Production Timelines Stretch Years Into the Future

Here’s where the opportunity emerges for uranium investors: actual uranium production is falling behind these demand projections. Industry leaders like David Cates at Denison Mines and Mark Chalmers at Energy Fuels point to a persistent supply constraint. New mines face multi-year permitting delays, with projects like Denison’s flagship development potentially not seeing an Environmental Impact Statement decision until 2026 at the earliest, and NexGen’s final permits slipping toward 2030 and beyond. Even faster in-situ recovery projects require staged, multi-year ramp-ups. Uranium spot prices reached $83-85 per pound in January 2026, marking 17-month highs, yet this remains below the replacement cost for many producers. This gap signals that current economics cannot justify new production at scale.

The Illusion of Supply Meets Reality

Utilities are seeing less supply materialize than forecasts advertise. Industry observers call this the illusion of supply-projections look rosy on paper, but actual deliveries fall short. Grassroots exploration becomes economically untenable at current prices, meaning the pipeline of future projects dries up. This combination of robust demand, delayed supply, and rising production costs creates a structural advantage for investors positioned in established or advanced-stage uranium assets in politically stable jurisdictions. The next section examines where these opportunities actually exist and how investors can access them.

How to Access Uranium Exposure Across Three Core Strategies

Direct Physical Uranium vs. Equity Exposure

Investors can pursue uranium through physical commodity holdings or equity positions, each offering distinct advantages. Physical uranium trades around $83–85 per pound as of January 2026, but storage costs consume carrying expenses, reducing net returns substantially. Mining stocks deliver superior exposure because producers capture upside when prices rise above their all-in production costs, typically $40–50 per pound for established operations. Cameco trades at $120.21 per share with a market cap of $52.48 billion, making it the largest uranium equity globally. Kazatomprom sits at $80.27 per share with $24.08 billion in market cap. Smaller developers like Denison Mines offer direct leverage to the supply gap identified earlier. Physical uranium positions make sense only if you possess secure storage infrastructure and can absorb carrying costs.

Mining Stocks: Where Leverage Concentrates

Uranium mining equities amplify returns when spot prices climb. A producer with $45 per pound all-in costs sees profit margins expand dramatically as prices move from $65 to $85 per pound. Cameco, Kazatomprom, and advanced-stage developers benefit most from the structural supply shortage outlined in the previous section. These operators sit in politically stable jurisdictions with established permitting pathways, reducing execution risk compared to early-stage explorers. The top uranium companies by market cap represent roughly 70% of the listed universe, concentrating capital in proven operators. Smaller-cap names offer higher risk and reward but demand deeper due diligence on project timelines and capital discipline.

ETFs: Instant Diversification Across the Sector

The Global X Uranium ETF holds $8.2 billion in assets with a 0.69% expense ratio and paid a 3.79% dividend yield as of January 2026. The Sprott Uranium Miners ETF manages $2.75 billion with a 0.75% expense ratio and targets mining operations exclusively. The Global X fund concentrates 69.43% of assets in its top ten positions, while Sprott concentrates 61.46% in its top ten. Both trade commission-free on major platforms and issue standard 1099 tax forms. Your choice between them depends on risk tolerance: the Global X fund provides broader exposure across producers and ancillary uranium businesses, while Sprott targets pure mining upside. ETFs eliminate single-company risk and simplify tax reporting for U.S. investors.

Building a Diversified Uranium Portfolio

A balanced approach weights exposure across mining stocks and ETFs rather than physical holdings, since equities capture both spot price upside and operational leverage as production ramps. Start with a core position in one of the two major ETFs to establish baseline sector exposure (roughly 40–50% of uranium allocation). Layer in 2–3 individual mining stocks representing different geographies and project stages to add conviction around specific supply gaps. Monitor uranium prices and track reactor construction timelines in China and India to time entry points around supply announcements or policy shifts. This structure lets you participate in the supply shortage while managing concentration risk across individual operators.

Where Regional Opportunities Emerge

Kazakhstan dominates current production, supplying roughly 40% of global uranium, yet faces its own permitting and cost pressures. African producers in Namibia and Niger offer exposure to emerging supply, though geopolitical risk runs higher. North American projects in Wyoming and New Mexico carry strategic advantages due to fuel-security considerations and stable regulatory environments. Canadian assets like those held by Denison benefit from Western political stability and established mining infrastructure. The next section examines these regional dynamics in detail and shows how geopolitical factors reshape uranium supply chains.

Where Uranium Supply Actually Comes From

Kazakhstan’s Production Dominance and Constraints

Kazakhstan controls roughly 40 percent of global uranium production, a dominance rooted in Soviet-era mining infrastructure and low extraction costs that hover around $30–35 per pound across its major operations. This cost advantage makes Kazatomprom, the state-owned producer, nearly unassailable in a supply-constrained market. However, Kazakhstan’s output faces its own pressure. Production timelines slip due to permitting delays and capital constraints, meaning the country cannot simply ramp up to fill the demand gap identified earlier. Investors should focus on Kazatomprom directly rather than junior explorers, since the government controls licensing and resource allocation.

African Producers and Geopolitical Risk

African producers in Namibia and Niger represent the next tier of supply, but geopolitical risk runs substantially higher. Niger experienced a military coup in 2023, and Namibia’s regulatory environment remains less transparent than North American alternatives. Paladin Energy operates in Namibia and offers exposure to African production, yet currency volatility and political uncertainty create friction that North American producers avoid entirely.

North American and Canadian Advantages

North American projects in Wyoming and New Mexico carry strategic premiums because the United States frames domestic uranium as a national security asset. Companies developing these projects benefit from stable permitting pathways and fuel-security mandates that utilities honor regardless of spot prices. Canadian assets held by Denison Mines sit in politically stable jurisdictions with established mining infrastructure, making them lower-risk alternatives to African or Central Asian exposure.

Western Supply Premiums and Market Dynamics

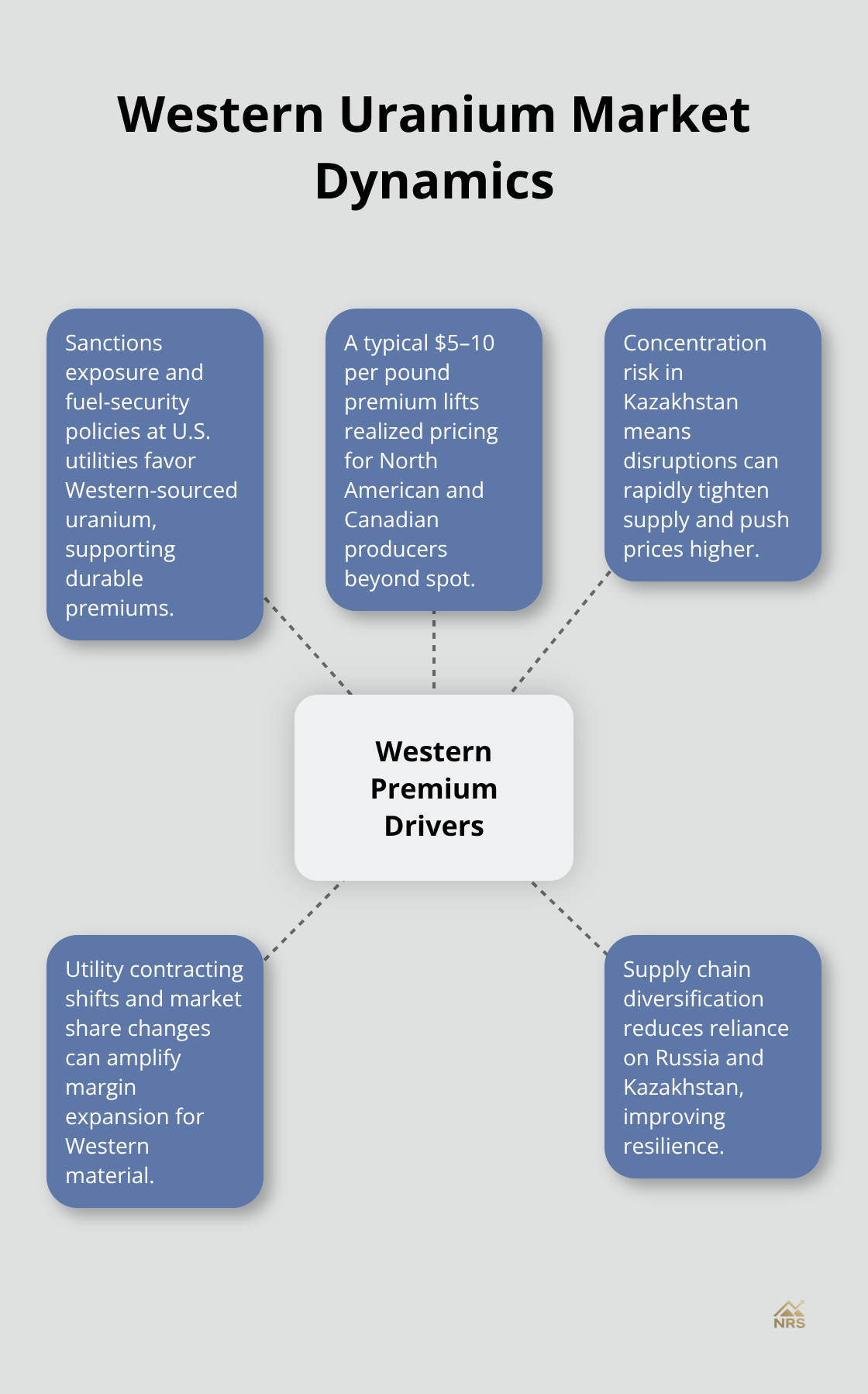

Western uranium commands a premium over equivalent material from Russia or Kazakhstan due to sanctions concerns and fuel-security policies at U.S. utilities. This premium varies but typically adds $5–10 per pound to Western material, meaning a North American or Canadian producer captures real margin expansion beyond spot price moves when market share shifts occur. Supply concentration in Kazakhstan also creates vulnerability; any disruption there tightens markets immediately and pushes prices higher.

Strategic Investment Positioning

Diversifying across geographies reduces single-country risk while positioning you to benefit from Western supply premiums. Try established producers in politically stable regions over early-stage projects in emerging markets, since execution risk compounds when permitting timelines stretch and regulatory changes occur without warning. Companies emphasizing disciplined capital allocation and 100 percent engineering before breaking ground, like Denison Mines, outperform those rushing toward production targets in riskier jurisdictions. The structural supply shortage means even mid-tier producers in stable regions can deliver outsized returns as utilities compete for reliable, Western-sourced uranium over the next five years.

Final Thoughts

The uranium market presents a genuine structural opportunity for investors who act on supply constraints that will persist for years. Demand locks in through government commitments, reactor construction timelines, and net-zero mandates, while supply lags far behind due to permitting delays stretching into 2026 and beyond, elevated production costs, and a drying exploration pipeline. This mismatch creates uranium investment opportunities for those positioned correctly in established producers within politically stable jurisdictions rather than speculative early-stage projects.

Your strategy should combine a core ETF position with 2–3 individual mining stocks representing different geographies to manage concentration while maintaining conviction around specific supply gaps. Cameco and Kazatomprom offer proven production and market dominance, while mining stocks deliver superior leverage compared to physical uranium holdings because operators capture margin expansion as prices climb above their all-in production costs. Western uranium commands premiums over equivalent material from other regions (meaning North American and Canadian producers benefit from structural tailwinds beyond spot price moves), making geopolitical risk in Africa and Central Asia less attractive despite lower production costs.

The next five years will test whether supply meets demand, and current economics suggest it cannot without higher prices or utility-funded development. Either outcome favors investors positioned in quality uranium assets today, so monitor uranium prices, track reactor construction announcements in China and India, and watch for policy shifts around fuel security. We at Natural Resource Stocks track these dynamics continuously through expert analysis and market insights, so explore emerging opportunities across the natural resource sector and stay informed on macroeconomic factors reshaping uranium and energy markets.