Paradigm, Velocity & Beacon Analyst Updates

Paradigm Capital – Mercur Drilling Broadly in Line, with a Few Higher-grade Surprises

Download Full Paradigm Capital Revival Gold Flash Note PDF

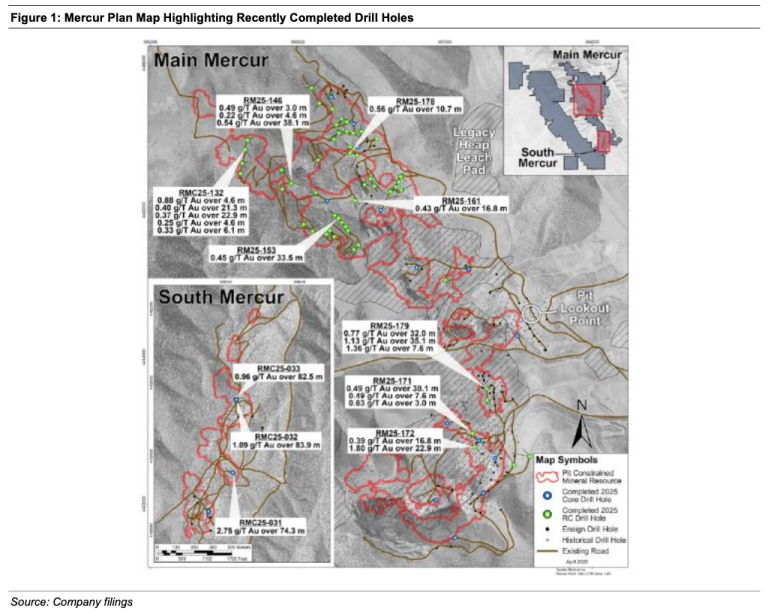

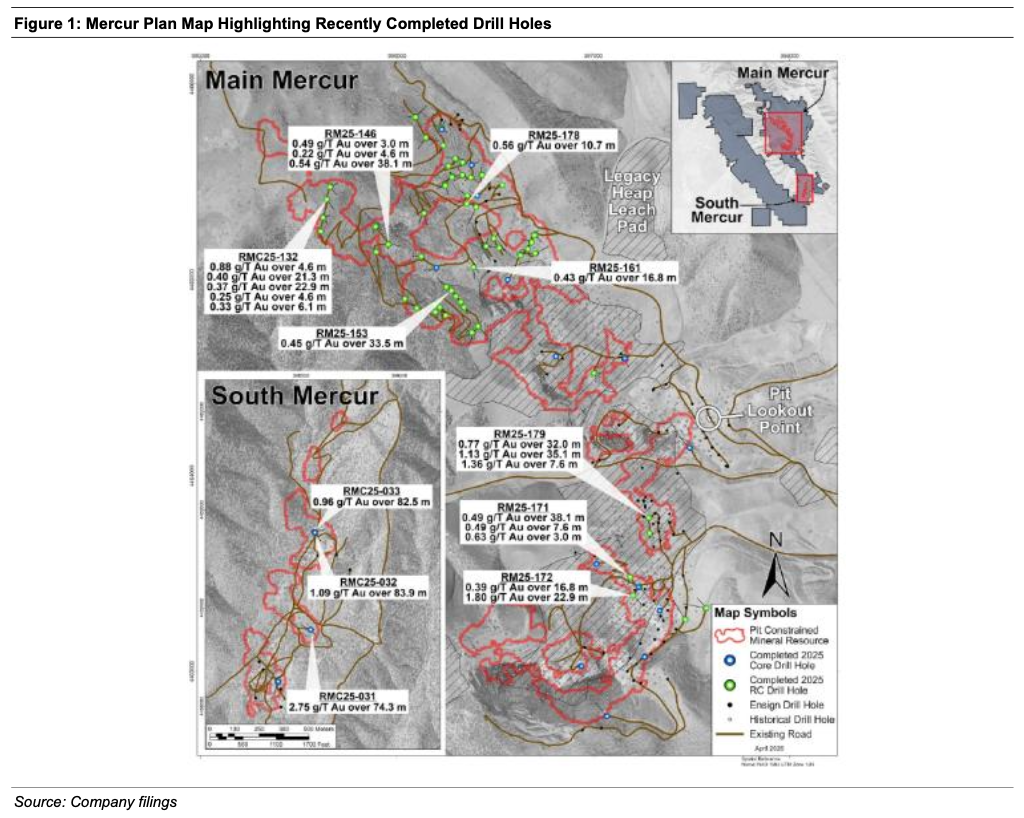

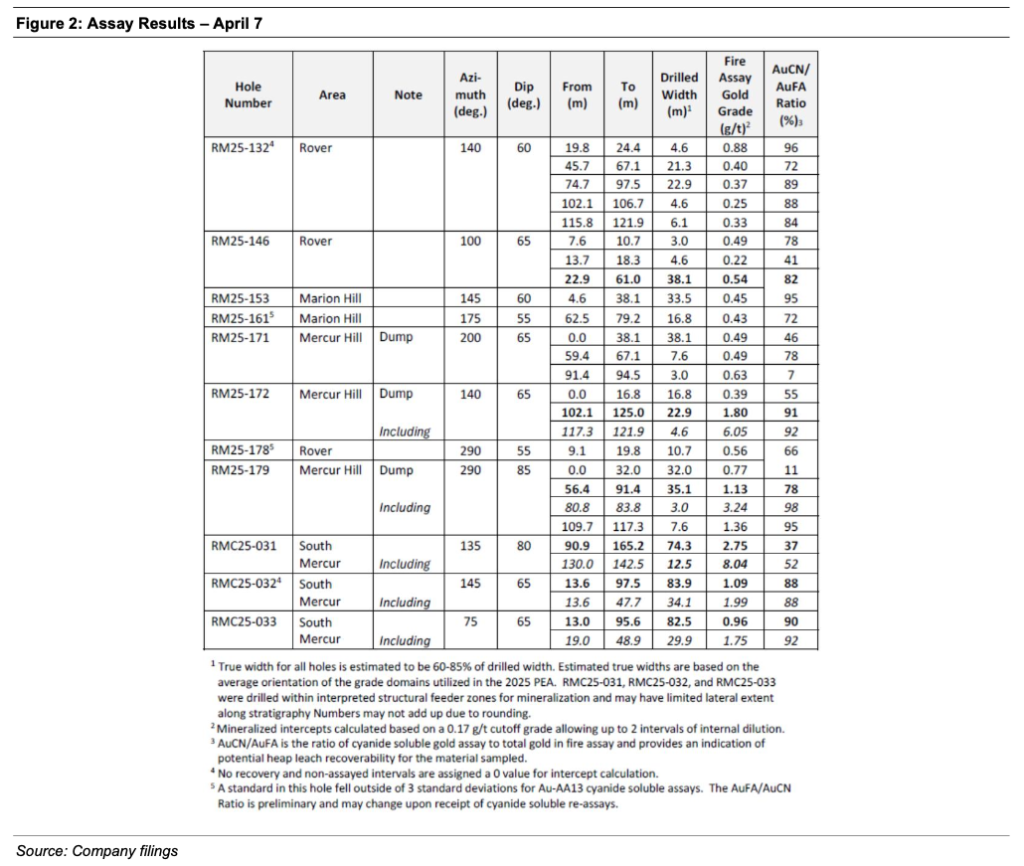

Revival provided final results from the 2025 drilling program at the Mercur Gold Project in Utah.

Details

- Several notable intercepts at South Mercur, including:

o RMC25-031: 74.3m @ 2.75 g/t (at 91m downhole), including 12.5m @ 8.04 g/t (at 130m downhole)

o RMC25-032: 83.9m @ 1.09 g/t (at 14m downhole)

o RMC25-033: 82.5m @ 0.96 g/t (at 13m downhole) - Drilling also encountered mineralized waste rock from the historical in-pit backfill, which is currently considered waste that would need to be moved. This suggests some waste-to-ore conversion, lowering the overall project strip ratio. Notable intercepts include:

o RM25-171: 38.1m @ 0.49 g/t (starting at surface)

o RM25-172: 16.8m @ 0.39 g/t (starting at surface)

Conclusion - Positive. The Mercur deposit is generally low grade (overall average grade of ore used in PEA study is 0.60 g/t), but there are

higher-grade domains within the deposit. Mercur is a Carlin-style gold system, and these are known to generate high-grade ore

shoots that have historically been a significant value driver for many of the gold mines in Nevada. Hole 31 of today’s press release

(12m @ 8 g/t) is showing intact high-grade zones at South Mercur. - We do temper this high-grade result with the observation that the intercept had a low cyanide soluble/fire assay (AuCN/AuFA)

ratio of 52%, suggesting this mineralization is at least partially refractory (and would likely have low to marginal recoveries on a

heap leach). But even low recoveries of high-grade mineralization can be economic, particularly when the grade is more than an

order-of-magnitude better than the average reserve grade. - Such high-grade shoots will not only benefit the current heap leach project but also point to longer-term exploration potential on

Mercur’s large 7,200-ha property. Recall that Revival recently exercised the option to acquire a 100% interest in the Mercur

property. - The high-grade intercepts are important, but the project is low grade (sub-1g/t) on average, so it is important to put the entire 2025

drill campaign into context:

o The weighted average 2025 Mercur intercept grade was 0.77 g/t gold (>25% above the average mineral resource grade).

o The weighted average 2025 intercept cyanide soluble/fire assay ratio was 77% (comfortably within the range of the 75%

recovery assumed in the PEA). - Data collected from drilling in 2025 and 2026 will support the company’s planned PFS targeted for release in Q1/27, a major

milestone on the path to restarting gold production at Mercur. Revival Gold is currently mobilizing to restart exploration and

engineering drilling at Mercur later this month with a planned program totaling 16,000m.

PCI’s disclosure policies and research distribution procedures can be found on our website at: www.paradigmcap.com

Velocity Trade Capital – Deeper Intercepts at Mercur; Last of 2025 Drilling Results

NEED TO KNOW

Highlights: 2.8 g/t Au over 74 m (RMC25-031) in the South Mercur area

Mercur drill program of 16,000 m planned for 2026; Beartrack-Arnett drilling ongoing

Trading at 0.15x P/NAV (incl. both assets), C$59 EV/oz M&I, C$31 EV/oz M&I, Inf.

Drilling to Recommence Late April Leading Up to Q1 2027 PFS

We are maintaining our C$2.45/sh target and Outperform rating on Revival Gold Inc. (“Revival”)

after the company announced exploration results from its PEA-ready Mercur Au project (100%,

UT, see Figure 1), marking the last 11 holes of the 115 hole program (from three rigs). Highlight

intercepts include 2.8 g/t Au over 74 m (RMC25-031) in the South Mercur area, a traditionally

higher-grade area, representing exploration potential at depth with intercepts reaching 165 m

from one of three known ore shoots as evidenced by historical underground mining (while

most results have been within 100 m from surface). Also, 0.54 g/t Au over 38.1 m from near

surface in the Rover area (RM25-146) along with mostly lower 0.25 g/t Au to 0.5 g/t Au to the

north at Rover, Marion Hill. Of note, the company reported 0.49 g/t over 38.1 m (RM25-171)

and 0.4 g/t Au over 16.8 m (RM25-172) from in-pit backfill, not currently counted in the

resource (ie. potentially crushable material that could be immediately placed on pad with no

mining costs, thereby reducing stripping/waste costs). The company continues to advance two

past-producing gold assets, Mercur and Beartrack-Arnett (100%, ID) with an eye on a strategic

goal of +150,000 oz/yr Au.

Mercur Program for 2026: The company has outlined a 16,000 m program for 2026

commencing latter half of April, focused on 12,000 m exploration and delineation drilling and

4,000 m for geotech and condemnation purposes. We estimate results to be released through

Q2 2026 (drilling continues at Beartrack-Arnett’s Joss underground target and we also are

expecting results from this program) as the company starts drilling at Main Mercur, moving

north to Rover followed by South Mercur. The program is based on two drill rigs.

Mercur Barrick Agreement: In December 2025, Revival announced that it gave notice to

exercise its option to acquire 100% of Barrick Mining Corporation’s interest in the Mercur Au

project, with an estimated closing in April 2026. As per the closing, terms included US$5.0M at

closing (paid) and US$5.0M on first, second and third anniversaries of commercial production.

In addition, Revival granted Barrick Gold a 2.0% NSR royalty over the acquired interests and a

1.0% NSR royalty on all mineral properties of which Revival has an interest within 1.0 km. Post-

transaction conclusion, we estimate 2.0 years to re-permit Mercur including a PFS release in Q1

2027, production to recommence in 2029, ramping up to an average rate of 97,000 oz Au/yr at

AISC of US$1,200/oz over 11 years after modest capital expenditures to re-start operations for

a NPV of C$838M, with annual average EBITDA of ~C$190M.

Au Price Sensitivities to Valuation: At the current ~US$4,700/oz Au price environment, would

equate to ~C$8.50/sh 2025E NAV. In terms of EBITDA, we would expect annual average to

increase from C$267M (at US$3,150/oz Au) to +C$450M (at US$4,800/oz Au).

Valuation: After adjustments to quarterly financials (working capital, shares outstanding)

our NAV/sh (2026E) decreases slightly from C$5.15 to C$5.09 while we maintain our

C$2.45/sh target based on a blended P/NAV target multiple of 0.48x (Figure 2). Revival is

currently trading at 0.15x P/NAV comprised of two past-producing Au mines. Our target

multiple reflects: i) ongoing drilling results from both projects (Mercur and Beartrack-

Arnett); ii) the permitted and past-producing status of both Mercur and Beartrack-Arnett

mines along with existing infrastructure; iii) modest capital required at both to restart

production; iv) near-term permitting completion, construction and ramp-up of production

and cash flow at Mercur (in 2029); iv) upside from additional underground sulphide

resources at Beartrack-Arnett; and v) strong technical backing from EMR Capital (12% holder)

and Dundee Sustainable Technologies (DST).

Download Full Velocity Trade Capital Revival Gold PDF Report

Beacon – Final Assays From 2025…Drills Turning In 2026

Revival Gold controls two past-producing oxide gold deposits in Idaho

(Beartrack) and Utah (Mercur), that it is advancing towards the potential re-

start of heap-leach operations later this decade. Initial economic studies

suggest potential for Revival Gold to become a 150,000-175,000 ounce per

annum gold producer.

Recent Exploration Results: this morning, Revival provided assay results from the

remainder of 2025 drilling completed at Mercur (fig1). Highlights included:

- RMC25-031: 74 metres grading 2.8g/t gold (from 91m depth)

(including 12 metres grading 8.0g/t gold at 130m depth) - RMC25-032: 84 metres grading 1.1g/t gold (from 14m depth)

- RMC25-032: 82 metres grading 1.0g/t gold (from 13m depth

Revival also encountered mineralized waste rock from historical in pit backfill

with interesting gold grades (that are not part of the current resource estimate) - 38 metres grading 0.5g/t gold

- 17 metres grading 0.4g/t gold

Key Takeaways: - Infill drilling confirming existing resource at Mercur

- Infill drilling often delivering higher gold grades than current resource

- New higher-grade interval (12m@8g/t) likely a future exploration target

to follow up - Historical in pit backfill likely of sufficient grade for economic gold

recovery (ie ore not waste)

Mercur Update: on April 2, Revival announced that it had completed

acquisition of a 100% interest in the Mercur project from Barrick Gold (ABX-T,

NR), by completing a US$5 million cash payment and granting a 2% net smelter

return (nsr) royalty to Barrick, as well as assuming environmental surety bonding

requirements for the property. Barrick will also receive US$5MM payments on

each of the first , second, and third anniversaries of commercial production.

2026 Exploration Plans: Mercur Project (Utah): a 12,000-metre drill programme

(RC and core) to upgrade/expand resources, as well as a 4,000-metre drill

programme related to engineering and mine design. Metallurgical testwork will

continue (results expected in Q2/26), along with completion of baseline surveys

as part of a PFS targeted for Q1/2027.

Beartrack/Arnett Creek Project (Idaho): a 3,000-metre drill programme (core)

is currently underway with 2 rigs focused on expanding the higher-grade

underground resources at Joss.

Investment Thesis Intact: we continue to view Revival Gold shares as an

attractive investment opportunity as they move their two main gold projects

towards development. With no changes to our model, we maintain our 12-

month target price of $2.00/sh and our BUY rating for Revival Gold shares.