Rare earth elements power everything from wind turbines to smartphones, yet most investors overlook these critical materials. China controls 85% of global rare earth processing, creating both supply risks and investment opportunities.

Are rare earth stocks a good investment in today’s market? We at Natural Resource Stocks examine the potential returns and significant risks facing this specialized sector.

What Makes Rare Earth Elements So Valuable

Seventeen metallic elements form the rare earth group, with neodymium, dysprosium, and terbium commanding prices that exceed $400 per kilogram. These materials possess unique magnetic and catalytic properties that make them irreplaceable in modern technology. Each electric vehicle requires 1-2 kilograms of rare earth elements, while a single wind turbine consumes up to 200 kilograms of neodymium for its permanent magnets.

China’s Manufacturing Stranglehold Creates Investment Opportunity

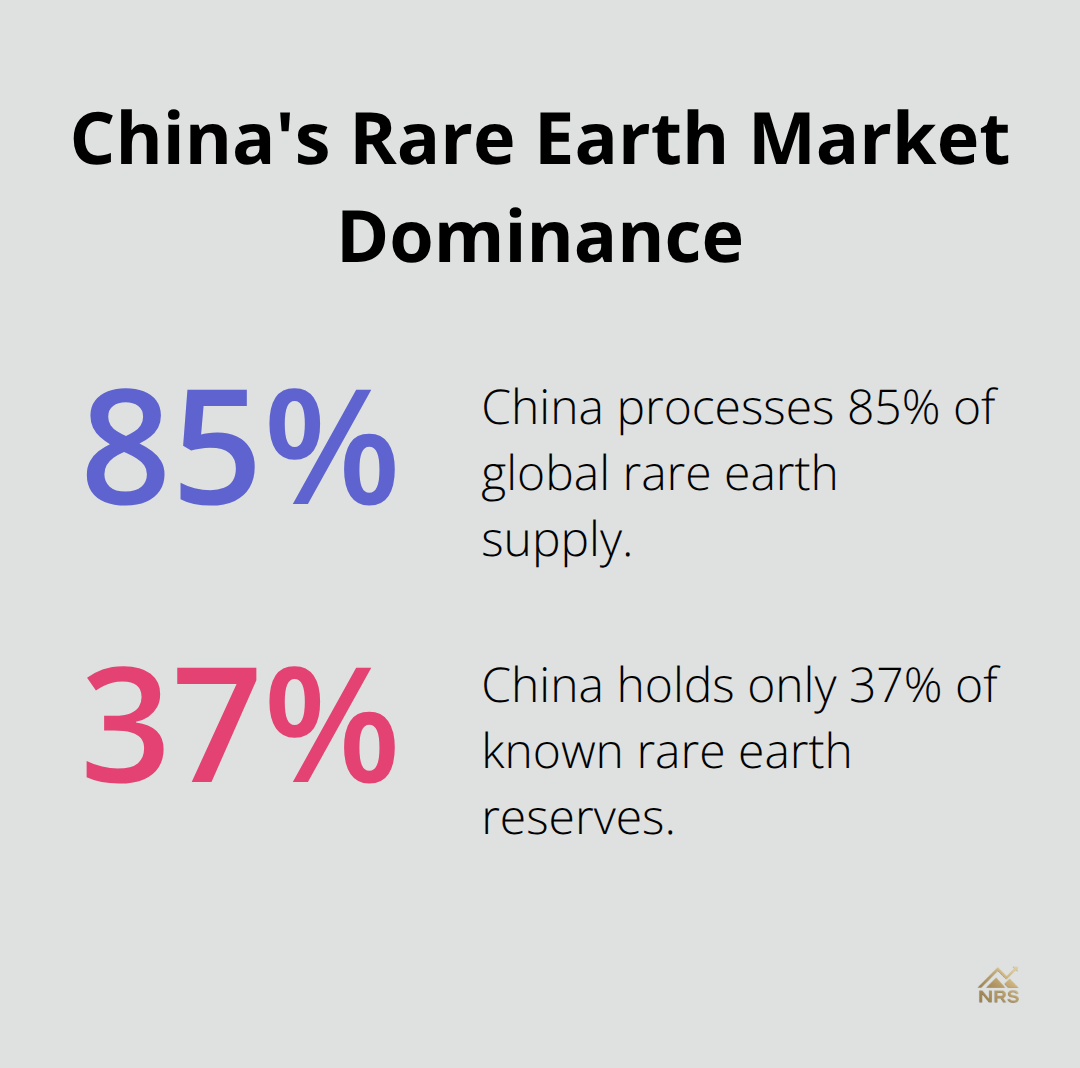

China processes 85% of global rare earth supply despite holding only 37% of known reserves (according to the US Geological Survey). This concentration stems from decades of aggressive pricing that drove Western competitors out of business during the 1990s. The Mountain Pass mine in California shut down in 2002 after Chinese producers flooded markets with below-cost materials. Today, even mines that operate outside China must ship concentrates to Chinese facilities for processing, which creates a bottleneck that smart investors can exploit.

Technology Demand Surge Outpaces Supply Growth

The global rare earth elements market was estimated at USD 3.95 billion in 2024 and is projected to reach USD 6.28 billion by 2030, growing at a CAGR of 8%, driven by electric vehicle production that increased 55% in 2022 alone. Wind turbine installations require 1,000 tons of neodymium annually per gigawatt of capacity, while smartphone production consumes 500 tons of rare earths yearly. Defense applications add another layer of demand, with each F-35 fighter jet containing 417 kilograms of rare earth materials. Supply expansion lags significantly behind this growth trajectory, which creates pricing pressure that benefits mining companies with operational assets.

This supply-demand imbalance has sparked a global race to develop alternative sources outside China’s control, opening new opportunities for investors who understand which companies lead this charge.

Which Rare Earth Stocks Offer the Best Investment Potential

Lynas Corporation Leads Western Production

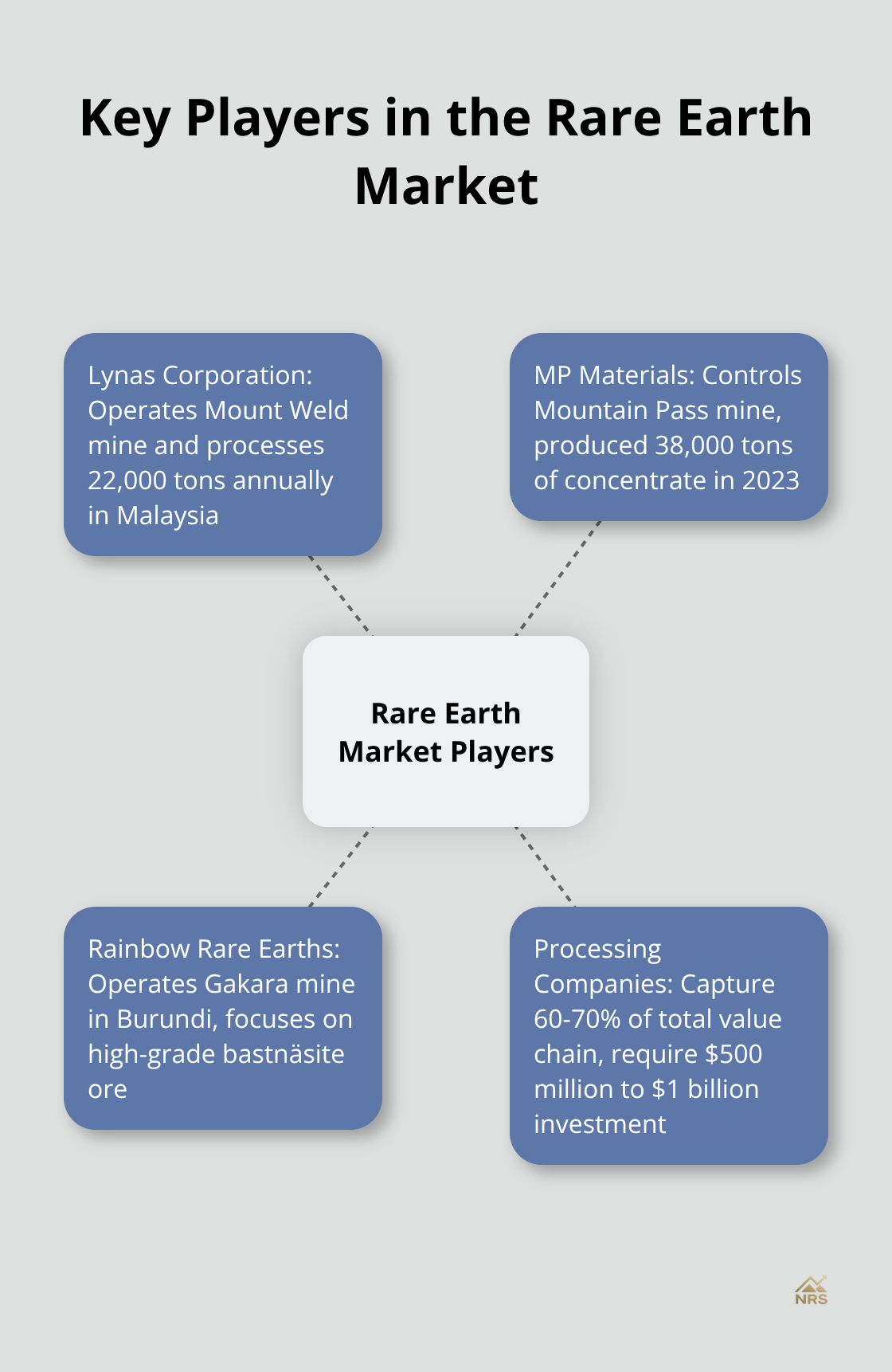

Lynas Corporation operates the Mount Weld mine in Western Australia and runs the world’s largest rare earth processing facility outside China in Malaysia. The company delivered record annual concentrate production in 2023 and generated revenue of $588 million. Lynas trades on both the Australian Securities Exchange and NASDAQ, which provides access to international investors. The Malaysian facility processes 22,000 tons annually and serves as the primary alternative to Chinese processing capacity.

MP Materials Controls America’s Strategic Asset

MP Materials controls the Mountain Pass mine in California, America’s only operational rare earth mine. The facility produced 38,000 tons of concentrate in 2023 and ships most material to China for processing. MP Materials announced a transformational public-private partnership with the Department of Defense in 2025, which creates the first fully integrated US rare earth supply chain since the 1990s. The company’s stock trades on the New York Stock Exchange and benefits from Pentagon contracts worth $45 million for heavy rare earth separation technology.

Rainbow Rare Earths Targets African Resources

Rainbow Rare Earths operates the Gakara mine in Burundi, which produces high-grade bastnäsite ore with significant concentrations of neodymium and praseodymium. The mine generated 2,800 tons of concentrate in 2023 with grades that average 47% rare earth oxides. African deposits typically contain higher concentrations of heavy rare earths like dysprosium and terbium, which command premium prices that exceed $300 per kilogram (these elements power high-performance magnets in electric vehicle motors and wind turbines).

Processing Companies Present Hidden Value

Companies that focus on processing and refining rare earth concentrates often trade at lower valuations than miners but control the most profitable segment of the supply chain. Processing facilities require $500 million to $1 billion in capital investment and take 5-7 years to build, which creates significant barriers to entry. These companies capture 60-70% of the total value chain compared to 20-30% for raw material extraction alone.

However, investors must also consider the substantial risks that come with these opportunities, particularly the regulatory and environmental challenges that can derail even the most promising projects.

What Are the Major Risks in Rare Earth Investment

Rare earth prices swing 50-80% annually due to limited market depth and speculative patterns that trap inexperienced investors. Neodymium prices dropped from $165 per kilogram to $65 between January and September 2022, while dysprosium fell 40% in the same period according to Shanghai Metals Market data. These dramatic swings occur because global rare earth volumes remain thin compared to base metals like copper or aluminum. A single large order can move prices 10-15% in hours, which makes technical analysis unreliable for entry points.

Environmental Compliance Costs Destroy Profit Margins

Rare earth extraction and processing generates radioactive waste that contains thorium and uranium, which requires specialized disposal facilities that cost $50-100 million per site. Molycorp filed for bankruptcy in 2015 after it spent $1.7 billion on environmental upgrades at Mountain Pass that failed to meet California regulations. Processing rare earth concentrate creates significant environmental problems due to mining and refinement of strategic elements, while separation facilities consume 8-10 tons of water per kilogram of refined elements. These environmental requirements add 30-50% to costs and create regulatory approval delays that stretch 3-5 years for new projects.

China Weaponizes Supply Chains Against Competitors

Beijing restricted rare earth exports to Japan during the 2010 Senkaku Islands dispute, which sent prices up 3,000% in six months and demonstrated how geopolitical tensions translate into immediate market disruption. China has imposed export restrictions on seven rare earth elements and magnets in retaliation for new U.S. tariffs, while state-owned enterprises receive preferential access to raw materials. The US Department of Commerce added 28 Chinese rare earth companies to trade restriction lists in 2021 (which limits technology transfers but forces American companies to develop more expensive domestic alternatives). Investors monitor US-China trade negotiations because any escalation immediately affects rare earth stock valuations, while companies with diversified supply chains outside China command premium valuations that reflect reduced political risk.

Market Manipulation Threatens Small Investors

Large institutional players and sovereign wealth funds control significant portions of rare earth futures markets, which allows them to manipulate prices through coordinated trades. The London Metal Exchange rare earth contracts often see 70% of daily volume concentrated in the final hour of trading (indicating potential price manipulation by major players). Small retail investors lack the capital and information advantages needed to compete against these institutional forces, while thin market liquidity amplifies the impact of large trades on stock prices.

Final Thoughts

Are rare earth stocks a good investment? The answer depends on your risk tolerance and investment timeline. Companies like Lynas Corporation and MP Materials offer exposure to a sector that will grow 8% annually through 2030, driven by electric vehicle production and renewable energy expansion. However, price volatility remains extreme, with neodymium prices that dropped 60% in 2022 alone.

Smart investors focus on companies with processing capabilities rather than pure miners, since processing captures 60-70% of the value chain. Entry timing matters significantly due to thin market liquidity and institutional manipulation. Dollar-cost averaging over 6-12 months reduces the impact of price swings that can reach 50-80% annually.

The long-term outlook favors Western producers as governments prioritize supply chain security. Defense spending and clean energy mandates create sustained demand that outpaces new supply development. We at Natural Resource Stocks provide expert analysis and market insights to help investors navigate these complex dynamics and identify the strongest opportunities in natural resource sectors.