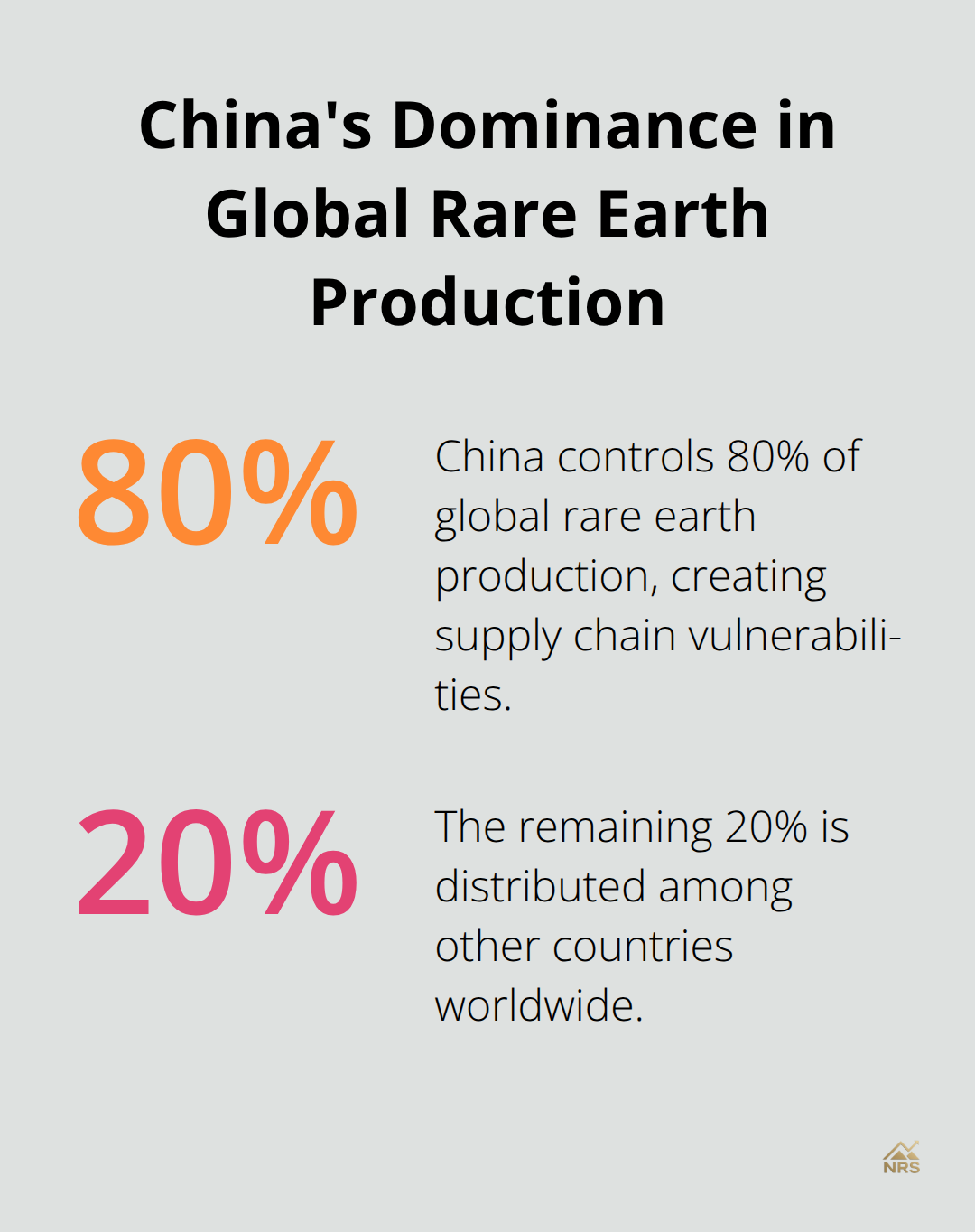

Rare earth elements power everything from smartphones to wind turbines, making them essential for modern technology. China controls 80% of global rare earth production, creating supply chain vulnerabilities that smart investors recognize.

We at Natural Resource Stocks see growing opportunities as governments push for supply diversification. This guide examines the top rare earth stocks to buy for investors seeking exposure to this strategic sector.

Why Rare Earths Control Modern Technology

Seventeen metallic elements form the rare earth family, yet their scarcity lies not in abundance but in extraction complexity. Neodymium and praseodymium power smartphone speakers and electric vehicle motors, while dysprosium strengthens wind turbine magnets against temperature extremes. Europium creates red phosphors in LED displays, and terbium enables green lights in smartphones. The global rare earth metals market was valued at USD 5,139.1 million in 2024 and is projected to reach USD 7,386.3 million by 2030 at a 6.2% CAGR.

China’s Strategic Chokehold

China produces nearly 70% of global rare earth mine output and controls over 80% of refining capacity. This creates dangerous supply dependencies that Beijing exploits through strategic export restrictions. Recent controls on five additional rare earth elements beyond previous limits demonstrate weaponized resource control.

The 2010 Rare Earths Crisis showed how quickly prices spike when China restricts exports-some rare earth prices increased 10x within months. Over 800 potentially minable deposits exist outside China, yet most remain undeveloped due to environmental challenges and capital requirements.

Technology Demand Explosion Ahead

Permanent magnet applications dominate rare earth consumption and account for the largest market share through 2030. Electric vehicle production requires 200-400 grams of rare earths per vehicle, while offshore wind turbines need up to 600 kilograms each. The International Renewable Energy Agency projects renewable energy could constitute over 90% of global power capacity by 2050, which will massively increase rare earth demand. Smartphone production consumes 16 different rare earth elements per device (with global smartphone shipments that exceed 1.2 billion units annually).

Investment Implications

These supply-demand dynamics create compelling investment opportunities for companies that can secure reliable rare earth sources outside China’s control. The U.S. government imposed 25% tariffs on Chinese rare earth magnets and allocated billions toward domestic production capabilities. This shift toward supply chain security makes rare earth mining companies attractive investment targets for the next chapter’s analysis of top performers.

Which Rare Earth Companies Lead the Investment Race

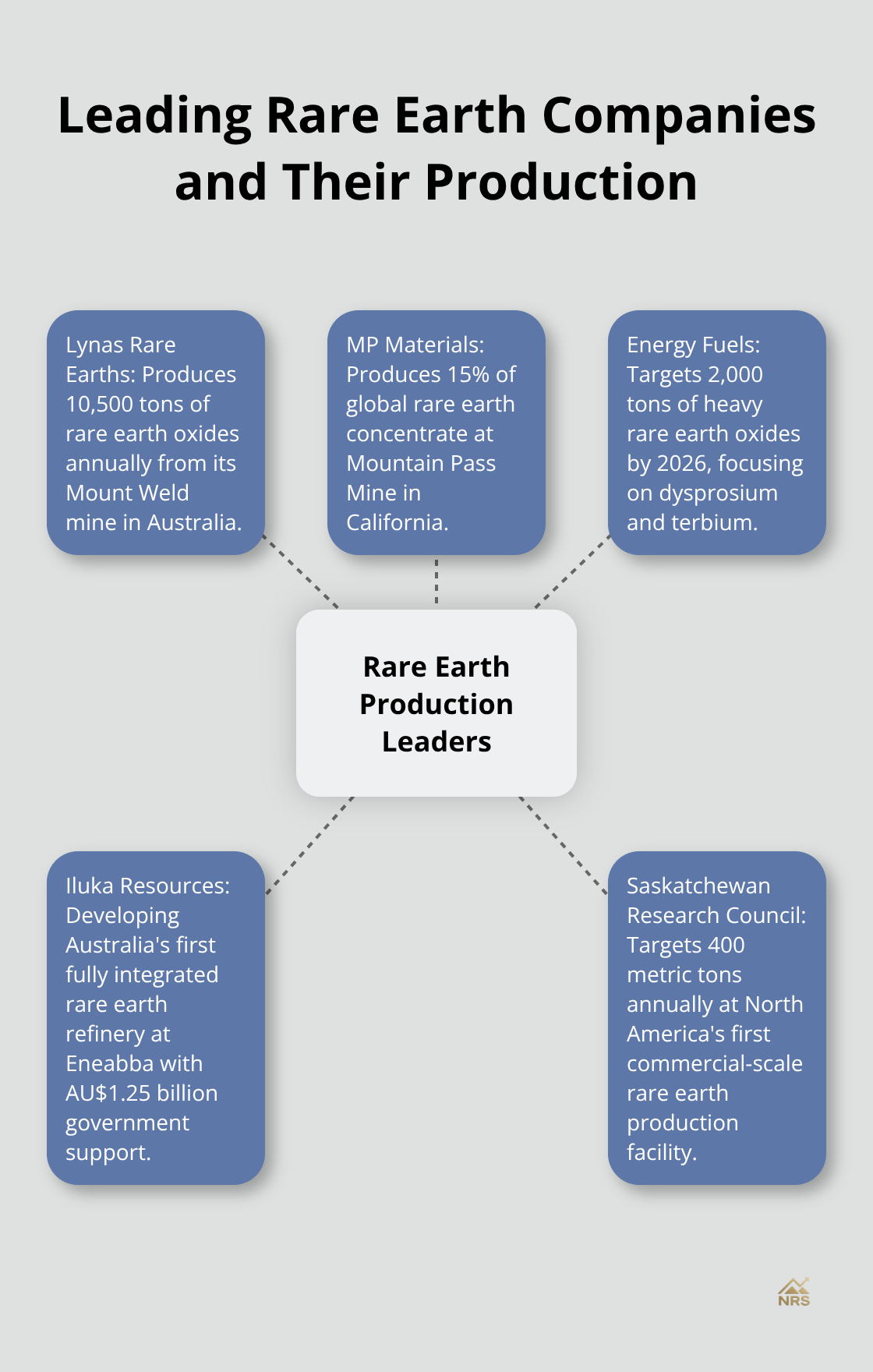

Lynas Rare Earths dominates as the world’s largest rare earth producer outside China and operates the Mount Weld mine in Western Australia with 92% increased mineral resources reported in 2024. The company processes concentrate at its Malaysian facility and produces 10,500 tons of rare earth oxides annually. MP Materials revived California’s Mountain Pass Mine and achieved record neodymium-praseodymium oxide production with 84% year-on-year revenue growth as of August 2025. The facility produces 15% of global rare earth concentrate and targets full vertical integration by 2025.

Production Leaders Set Market Standards

Energy Fuels targets commercial heavy rare earth oxide production by late 2026 and secured partnerships with South Korean firm POSCO Holdings for automotive supply chains. The company focuses on heavy rare earth elements that command premium prices due to their scarcity and specialized applications. Aclara Resources operates its environmentally friendly Penco Module project in Chile and produces rare earth concentrate through ionic clay extraction methods. This approach reduces environmental impact compared to traditional hard rock extraction methods.

Processing Capabilities Drive Valuations

Iluka Resources develops Australia’s first fully integrated rare earth refinery at Eneabba with AU$1.25 billion in government support and focuses on heavy mineral sands extraction. The facility will process monazite concentrate into separated rare earth oxides and targets production start in 2025. NioCorp Developments integrates rare earth magnet recycling into its Elk Creek project and extends mine life through improved ore grades.

Ucore Rare Metals develops a commercial processing facility in Louisiana with US$18.4 million Department of Defense support (targeting 2026 production start).

Geographic Diversification Reduces China Risk

The Saskatchewan Research Council announced North America’s first commercial-scale rare earth production facility and targets 400 metric tons annually. Arafura Resources secured AU$200 million in support for its Nolans project in Australia and focuses on high-grade neodymium and praseodymium deposits. These companies benefit from government support programs, including Canada’s nearly $4 billion critical minerals allocation and U.S. Defense Department stockpiling worth $1 billion.

Mkango Resources signed recycling technology deals to create sustainable permanent magnet supply chains. Companies with processing capabilities outside China command premium valuations as governments prioritize supply chain security over cost optimization. These operational advantages and government support create the foundation for evaluating investment potential in the next section.

What Makes a Rare Earth Stock Worth Buying

Production Scale Separates Winners from Pretenders

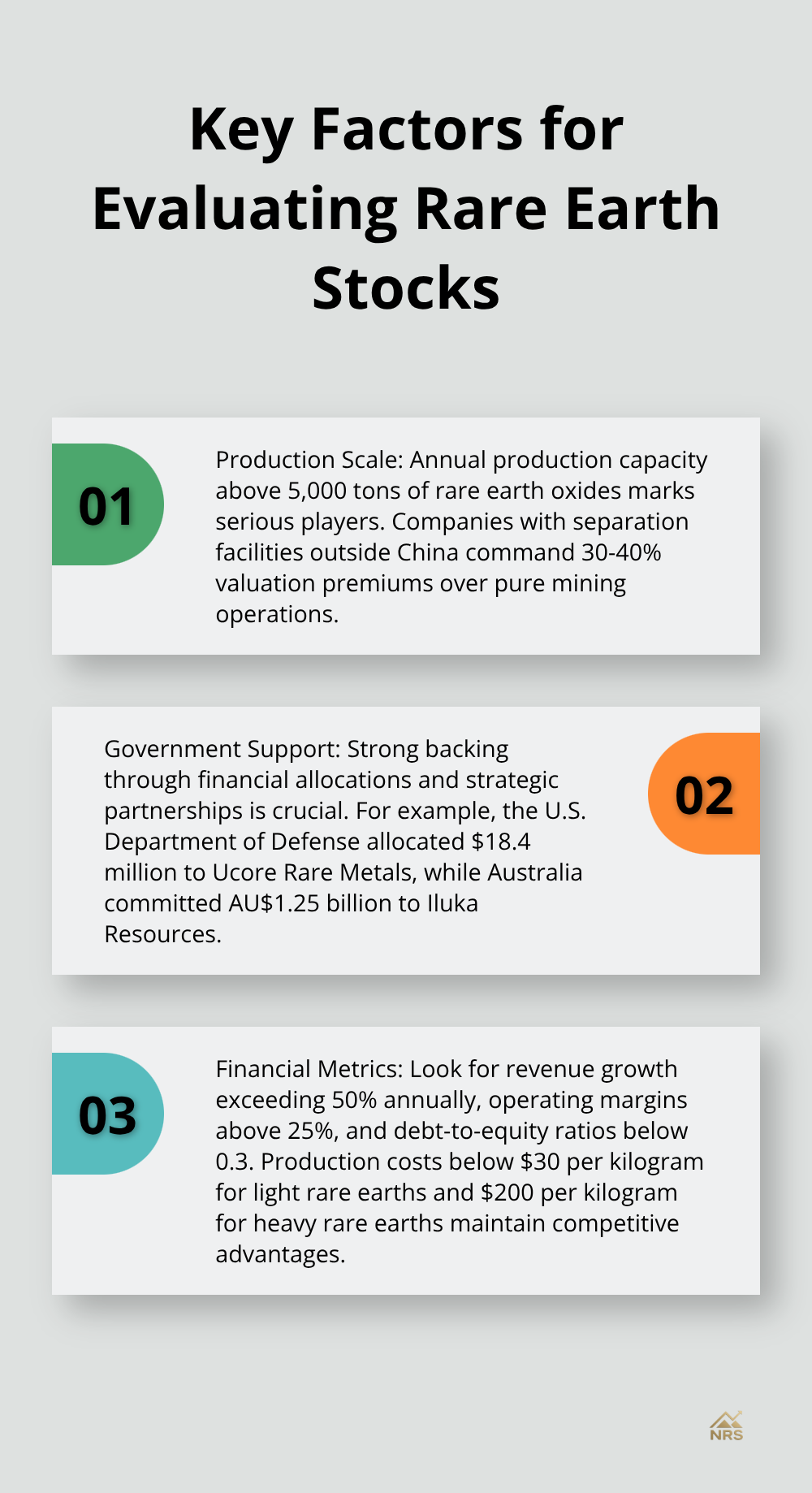

Annual production capacity above 5,000 tons of rare earth oxides marks serious players in this market. MP Materials produces 15% of global concentrate at 38,000 tons annually, while Lynas processes 10,500 tons of finished oxides through its integrated operations. Processing capabilities matter more than mining volume since China accounted for around 69% of the world’s production of rare earth ores in 2023.

Companies with separation facilities outside China command 30-40% valuation premiums over pure mining operations. Energy Fuels targets 2,000 tons of heavy rare earth oxides by 2026, focusing on dysprosium and terbium that sell for $300-400 per kilogram versus $50-80 for light rare earths. Vertical integration from mine to magnet reduces supply chain risk and captures higher margins at each processing stage.

Government Support Determines Long-Term Viability

The U.S. Department of Defense allocated $18.4 million to Ucore Rare Metals and $1 billion for strategic stockpile programs. Australia committed AU$1.25 billion to Iluka Resources for domestic refining capacity, while Canada allocated C$3.8 billion across critical minerals projects.

Geographic location outside China reduces regulatory risk (with Australian and North American operations facing minimal export restrictions). Balance sheet strength becomes secondary when government backing provides capital and guaranteed offtake agreements. Debt-to-equity ratios below 0.3 indicate financial stability, though government-supported projects can operate with higher leverage safely.

Financial Metrics That Signal Success

Revenue growth that exceeds 50% annually signals strong market position, as demonstrated by MP Materials’ 84% year-on-year increase in August 2025. Companies must demonstrate consistent cash flow generation rather than just resource estimates. Operating margins above 25% separate profitable operations from marginal players in this capital-intensive sector.

Market capitalization relative to proven reserves reveals valuation opportunities (with ratios below $100 per ton of contained rare earth oxides often indicating undervalued assets).

Production costs below $30 per kilogram for light rare earths and $200 per kilogram for heavy rare earths maintain competitive advantages during price downturns.

Final Thoughts

Rare earth stocks to buy present compelling opportunities as governments worldwide prioritize supply chain security over cost optimization. The projected market growth to USD 7,386.3 million by 2030 reflects accelerated demand from electric vehicles and renewable energy sectors that require these critical materials. MP Materials and Lynas Rare Earths lead investment opportunities with proven production capabilities and government support.

Energy Fuels and Iluka Resources offer exposure to high-value heavy rare earths that command premium prices. These companies benefit from strategic positions outside China’s control and access to processing facilities that capture higher margins. Risk management requires geographic diversification across Australian, North American, and South American operations (with debt-to-equity ratios below 0.3 and annual production that exceeds 5,000 tons of rare earth oxides).

Government support through defense contracts and strategic stockpile programs reduces operational risk significantly. Companies with separation facilities outside China command 30-40% valuation premiums over pure extraction operations. We at Natural Resource Stocks provide expert analysis and market insights across metals and energy sectors to help investors navigate these complex markets and identify opportunities in critical minerals.