Rare earth elements power everything from electric vehicles to wind turbines, making them essential for the global energy transition. Supply chain disruptions and geopolitical tensions have created significant opportunities for investors.

We at Natural Resource Stocks have identified the best rare earth stocks positioned to benefit from surging demand. This analysis covers top companies, key investment factors, and market trends shaping the sector’s future.

Top Rare Earth Stocks to Consider

Lynas Rare Earths and Market Position

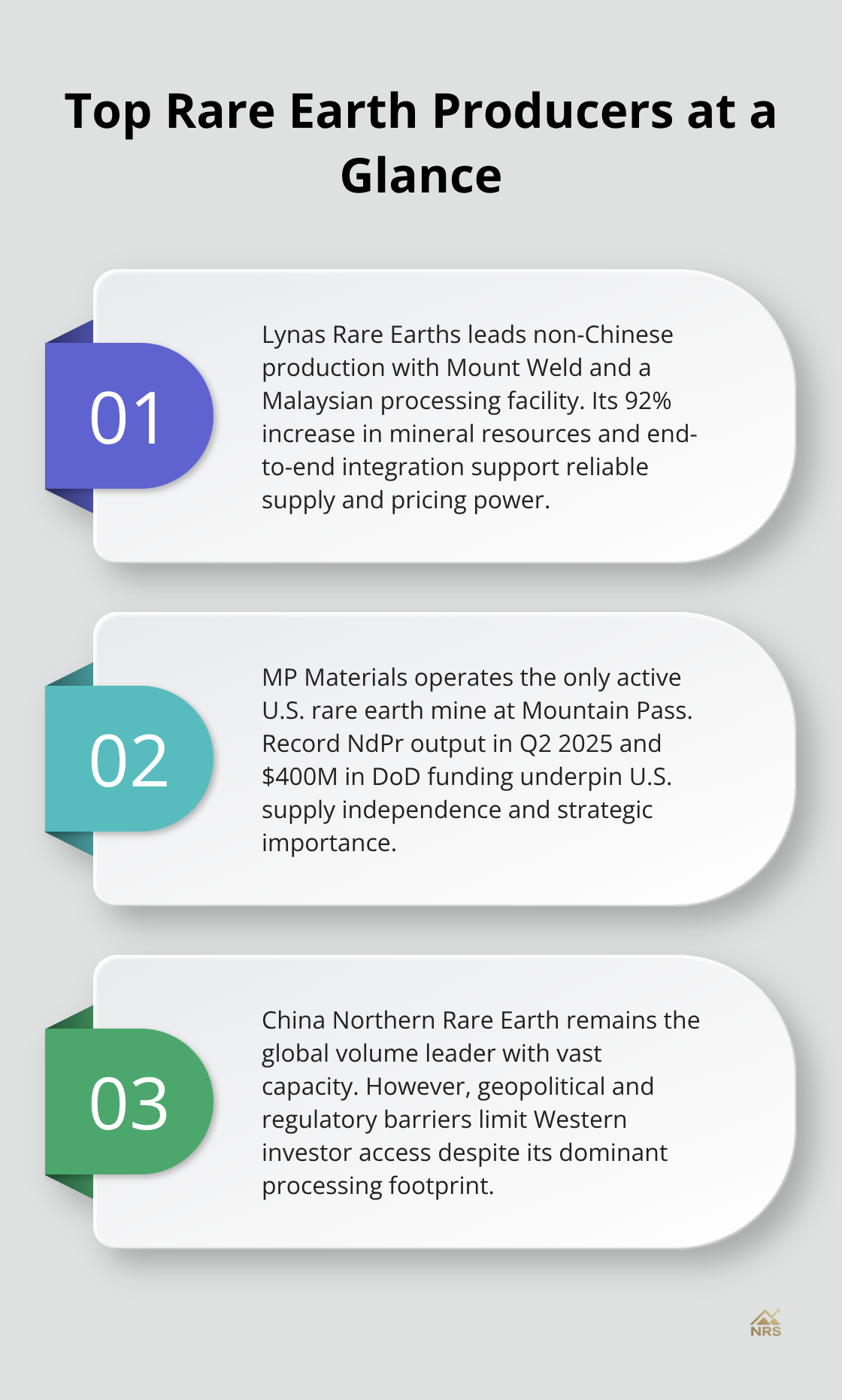

Lynas Rare Earths leads the non-Chinese market with superior operational strength. The Australian company operates the Mount Weld mine and reported a 92% increase in mineral resources, which establishes it as the top producer outside China. Lynas provides comprehensive financial reporting and maintains its position as the most dependable alternative to Chinese supply chains.

The company’s Malaysian processing facility provides complete vertical integration (a competitive advantage most competitors cannot match). This end-to-end control over production gives Lynas pricing power and supply chain reliability that investors value highly.

MP Materials and US Production Focus

MP Materials controls North America’s only active rare earth mine at Mountain Pass, California. The company produced 597 metric tons of neodymium and praseodymium in Q2 2025, which set new production records. MP Materials received $400 million from the US Department of Defense in July 2025 to construct a Texas magnet manufacturing facility.

This government support makes MP Materials the strongest investment for US rare earth independence. The company benefits from bipartisan political backing and strategic importance to national security (factors that provide downside protection for investors).

China Northern Rare Earth Industry Group

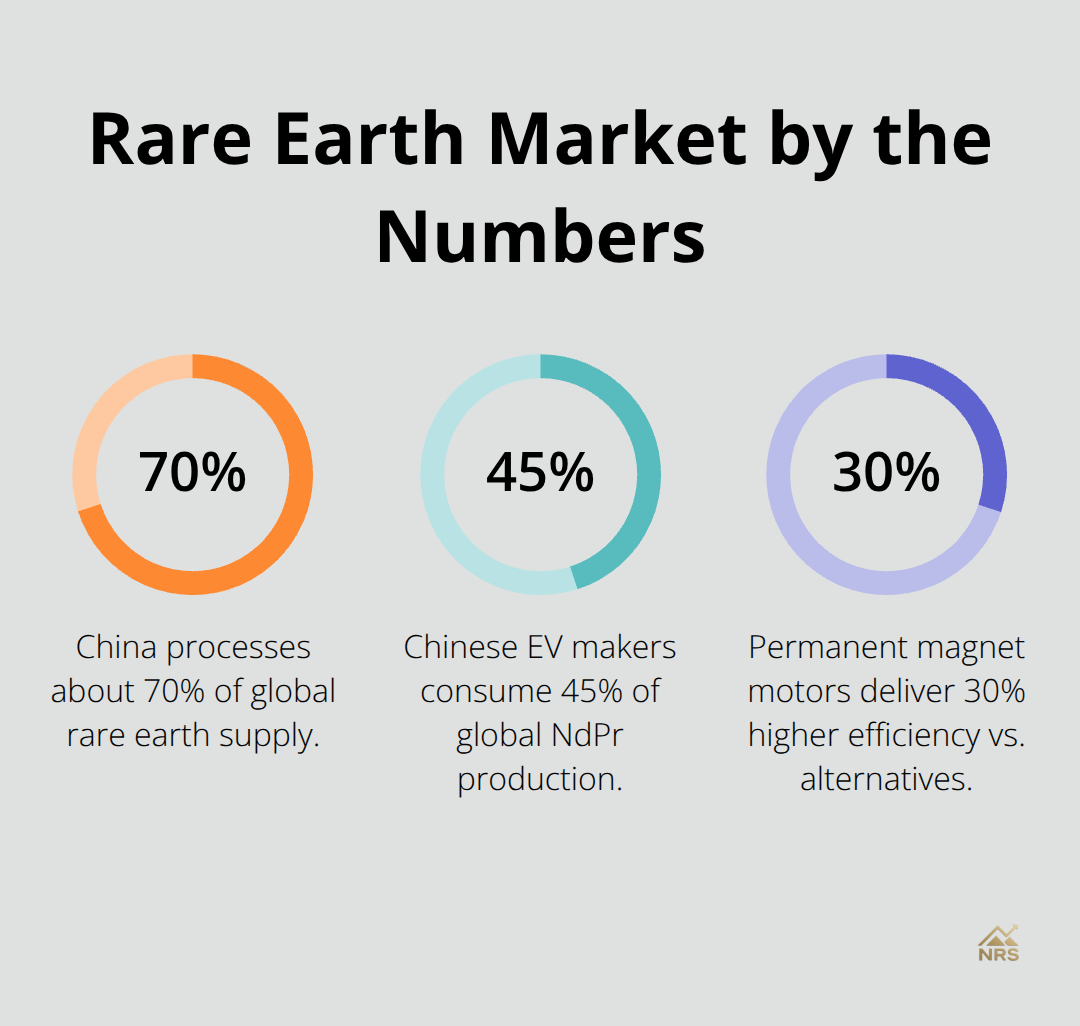

China Northern Rare Earth Industry Group maintains its position as the global production leader with massive capacity, but geopolitical tensions restrict Western investor access. The company processes approximately 70% of global rare earth supply, yet regulatory barriers and trade restrictions make direct investment challenging for most Western portfolios.

Smart investors focus on Lynas and MP Materials as the two companies with proven production records, government support, and expansion plans. These factors become even more important when you consider how production capacity and mining reserves affect investment returns.

Key Factors When Evaluating Rare Earth Investments

Production Capacity and Mining Reserves

Production capacity determines which rare earth companies survive market volatility and which ones fail spectacularly. MP Materials produced 597 metric tons of neodymium-praseodymium in Q2 2025, while most competitors struggle to reach commercial production levels. Companies with proven reserves above 50,000 tons of rare earth oxides provide the scale needed for long-term profitability.

Lynas controls 21 million tons of total rare earth oxide resources at Mount Weld. This massive reserve base gives the company decades of production runway that smaller players cannot match. Investors should focus on companies with both current production and substantial reserves (rather than development-stage projects with uncertain timelines).

Geographic Diversification and Supply Chain Risk

China exported 58,142 metric tons of rare earth magnets in 2024 with a total export value of almost US$2.9 billion, demonstrating its dominance in rare earth processing capacity. This creates massive supply chain vulnerabilities for companies dependent on Chinese facilities. MP Materials operates entirely within US borders and received Defense Department funding, which eliminates Chinese processing risk completely.

Lynas processes materials in Malaysia but faces ongoing regulatory pressure that could disrupt operations. Companies with processing facilities in Australia, Canada, or the United States command premium valuations because investors pay extra for supply chain security. The Center for Strategic and International Studies warns that half of non-Chinese rare earth projects become economically unviable when neodymium-praseodymium prices drop below $60 per kilogram.

Financial Performance and Debt Levels

Debt levels above $500 million signal trouble for rare earth companies because processing facilities require massive capital expenditure with uncertain returns. Energy Fuels completed construction of its separation circuit at White Mesa mill with manageable debt levels, while several competitors borrowed heavily and now struggle with cash flow problems.

Companies with positive operating cash flow and debt-to-equity ratios below 0.5 survive price downturns that destroy overleveraged competitors. Smart investors avoid companies that burn through cash without commercial production because rare earth development takes 7-10 years and costs frequently exceed $1 billion.

These financial metrics become even more important when you consider the market trends that drive rare earth demand and create investment opportunities.

Market Trends That Drive Rare Earth Demand

Electric Vehicle Production Accelerates Consumption

Electric vehicle production creates the most significant demand driver for neodymium and praseodymium, with each Tesla Model 3 requiring approximately 1 kilogram of rare earth magnets for its motor. Global EV sales reached 14 million units in 2024, and the International Energy Agency projects 230 million EVs on roads by 2030. This expansion requires 460,000 tons of additional rare earth magnets annually, which creates supply shortages that benefit companies like MP Materials and Lynas.

Ford and General Motors secured expedited export licenses through China’s green channel program, but this dependency makes Western automakers vulnerable to supply disruptions that could halt production lines within weeks. Permanent magnet motors dominate electric vehicle design because they deliver 30% higher efficiency than alternative technologies.

Wind Energy Infrastructure Demands Heavy Rare Earths

Wind turbine installations drive heavy rare earth consumption, with each 3-megawatt turbine containing 600 kilograms of rare earth magnets in its generator. The US installed 13.2 gigawatts of wind capacity in 2024, which required 2,640 tons of rare earth materials. BMW, Mercedes, and Audi cannot switch to rare earth-free motors without sacrificing performance that customers expect from premium vehicles.

Chinese EV manufacturers like BYD and Tesla’s Shanghai factory consume 45% of global neodymium-praseodymium production, which creates price pressure that reached $140 per kilogram in early 2025.

Defense Applications Command Premium Prices

Defense spending on rare earth applications reached $2.1 billion in 2024, with F-35 fighter jets requiring rare earth elements for fin actuators and missile guidance systems. China’s Announcement 18 export controls target medium and heavy rare earths used in military applications, which forces the Pentagon to fund domestic production through companies like MP Materials. The Department of Defense’s $400 million investment in MP Materials specifically addresses weapons system vulnerabilities that threaten national security readiness.

Advanced missile guidance systems require dysprosium and terbium, with dysprosium trading at $453.90 per kilogram as of 2025. Lynas became the first non-Chinese producer of dysprosium oxide, which positions the company to capture military contracts worth $50-100 million annually. Defense contractors pay 200% premiums for non-Chinese rare earths to meet security requirements (a factor that guarantees sustained profit margins for Western producers).

Final Thoughts

MP Materials and Lynas Rare Earths stand out as the best rare earth stocks for investors who want exposure to this strategic sector. MP Materials receives $400 million in Defense Department support and operates the only US rare earth mine, while Lynas controls 21 million tons of reserves and leads non-Chinese production with 92% resource growth. Smart investors focus on companies with proven production records rather than development-stage projects.

Risk management demands attention to companies with strong balance sheets and established operations. Companies with debt-to-equity ratios above 0.5 face destruction when rare earth price volatility hits their cash flow (a common problem in this sector). Operations outside Chinese processing facilities provide supply chain security that commands premium stock valuations.

Electric vehicle production creates sustained demand for 460,000 tons of additional rare earth magnets annually through 2030. Defense contracts worth $2.1 billion and wind energy expansion support established producers with long-term growth potential. We at Natural Resource Stocks provide comprehensive analysis of natural resource investments to help investors navigate this complex sector.