Rare earth minerals power nearly every piece of modern technology, from smartphones to wind turbines. Despite their name, these 17 chemical elements aren’t actually rare in Earth’s crust.

We at Natural Resource Stocks see growing investor interest in this sector as global demand surges. This rare earth minerals definition guide covers everything from basic properties to investment opportunities in this strategic market.

What Exactly Are Rare Earth Elements

Rare earth elements form a group of 17 metallic elements on the periodic table that share unique magnetic, luminescent, and electrochemical properties. These elements include the 15 lanthanides plus scandium and yttrium. The lanthanide series spans from lanthanum (atomic number 57) to lutetium (atomic number 71), while scandium and yttrium possess similar chemical characteristics that place them in this category.

The Complete List of 17 Elements

The light rare earth elements include lanthanum, cerium, praseodymium, neodymium, promethium, samarium, and europium. Heavy rare earth elements consist of gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium, plus scandium and yttrium. Neodymium commands the highest market value due to its magnetic properties in permanent magnets. Cerium represents a significant portion of rare earth production globally.

Why the Name Misleads Investors

The term “rare earth” creates massive confusion among investors and the general public. These elements aren’t rare at all in Earth’s crust. Cerium appears more frequently than copper, while neodymium exists in higher concentrations than gold or silver. The real challenge lies in locating economically viable deposits where these elements concentrate in mineable quantities.

Most rare earth elements scatter throughout common rocks at low concentrations. This distribution makes extraction expensive and technically complex. Economic reality, not geological scarcity, drives the supply constraints that create investment opportunities in rare earth companies.

Physical and Chemical Properties

These elements share similar atomic structures that give them distinctive properties. They exhibit strong magnetic characteristics, produce specific colors when excited, and conduct electricity efficiently. Heavy rare earth elements (particularly dysprosium and terbium) maintain their magnetic strength at high temperatures, making them valuable for advanced applications.

The next section examines where these valuable elements concentrate naturally and how companies extract them from the ground.

Where Are Rare Earth Elements Actually Mined

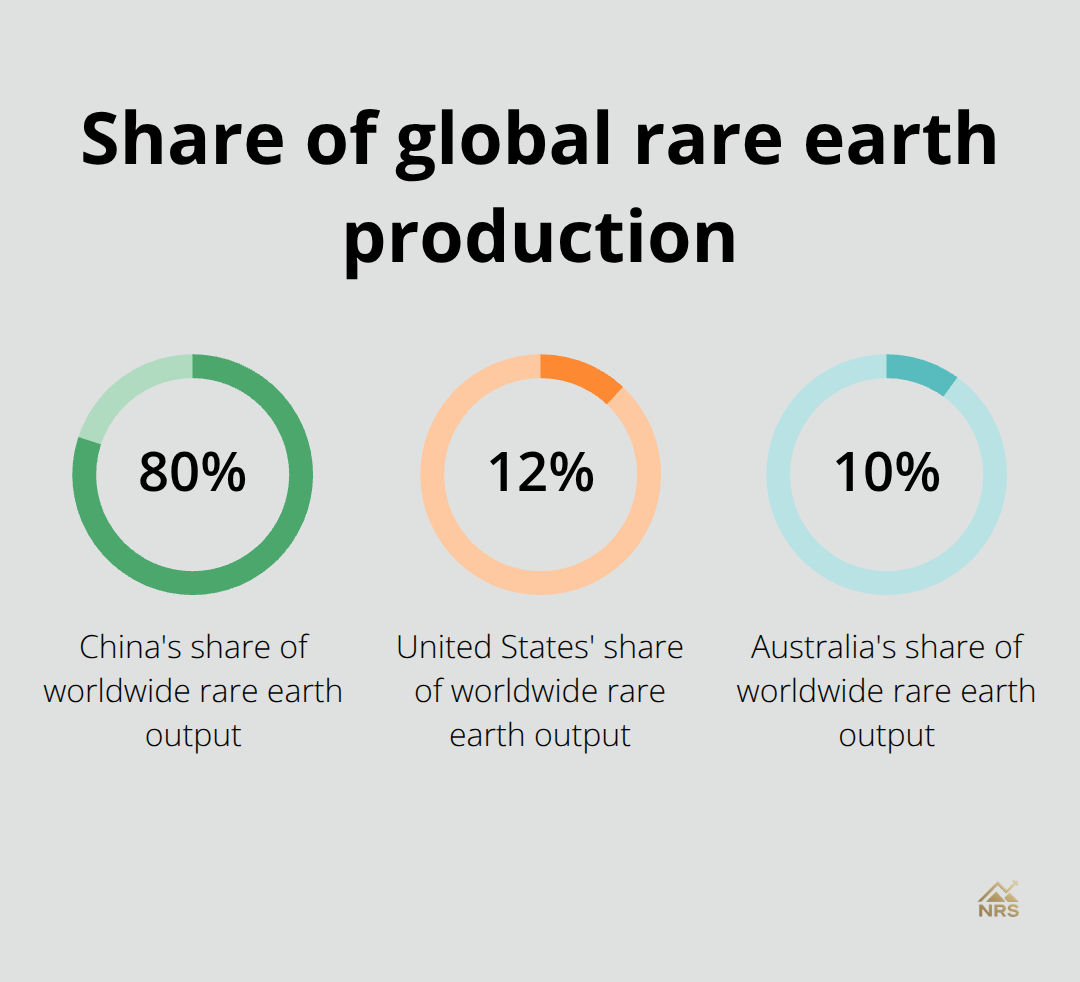

China dominates global rare earth production with 80% of worldwide output, primarily from the Bayan Obo mine in Inner Mongolia and ion-adsorption clay deposits in southern provinces. The United States produces roughly 12% through the Mountain Pass mine in California, which Molycorp reopened in 2012 after environmental upgrades. Australia contributes 10% mainly from the Mount Weld operation, while Myanmar supplies about 5% through informal networks that often bypass environmental regulations.

China’s Stranglehold on Global Supply

The Bayan Obo deposit contains an estimated 48 million tons of rare earth oxides, which makes it the world’s largest known reserve. Chinese producers benefit from lower labor costs and relaxed environmental standards, which allows them to undercut international competitors by 30-40%. The Chinese government restricts export quotas strategically and creates artificial scarcity that drives up global prices. This monopolistic control explains why rare earth prices spiked 750% between 2010 and 2011 when China temporarily reduced exports.

Complex Extraction Creates Environmental Disasters

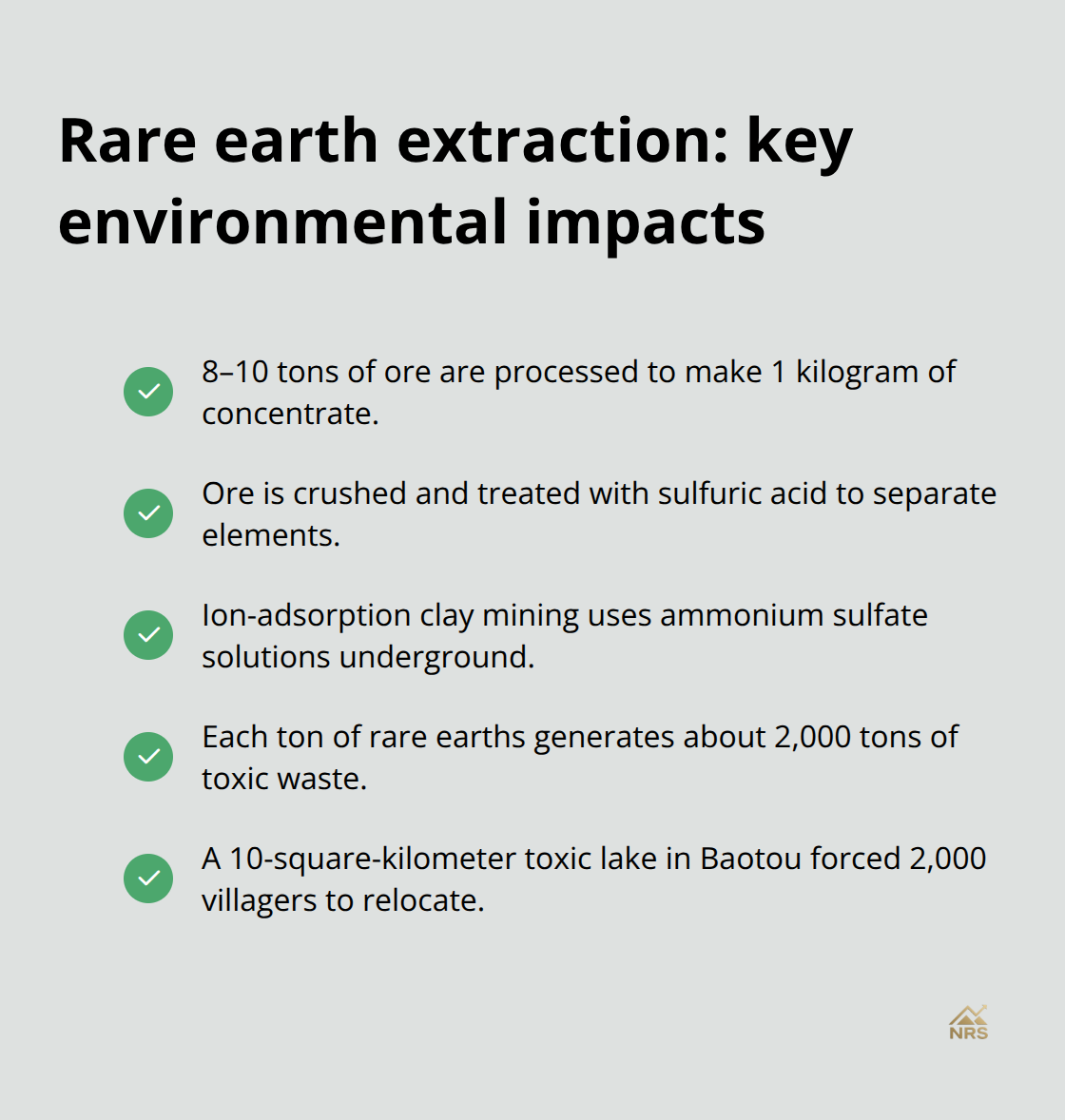

Companies must process 8-10 tons of ore to produce one kilogram of rare earth concentrate. The extraction process involves ore that workers crush, then treat with sulfuric acid and other harsh chemicals to separate elements. Ion-adsorption clay operations pump ammonium sulfate solutions underground and create massive toxic waste pools. Each ton of rare earth elements generates approximately 2,000 tons of toxic waste that contains radioactive thorium and uranium byproducts.

The Baotou region in China now contains a 10-square-kilometer toxic lake from decades of rare earth processing (this forced 2,000 villagers to relocate due to health concerns).

Processing Bottlenecks Beyond the Mine

Even countries with rare earth deposits face serious challenges in processing. Raw ore requires specialized refineries that cost $1-2 billion to build and take 5-7 years to become operational. China controls significant global rare earth processing capacity and creates supply chain vulnerabilities for Western manufacturers. Malaysia’s Lynas Advanced Materials plant represents the only significant non-Chinese facility that handles Australian ore from Mount Weld.

These supply chain constraints directly impact the industrial applications that drive demand for rare earth elements across multiple sectors.

What Industries Drive Rare Earth Demand

Electronics manufacturers consume 65% of global rare earth production, with smartphones alone requiring 16 different rare earth elements per device. A single iPhone contains approximately 8 grams of rare earths, including neodymium for speakers, europium for touchscreens, and terbium for color displays. Apple produced 231 million iPhones in 2022, which created demand for 1,848 tons of rare earth elements just from this product line. Tesla Model S vehicles contain 22 pounds of rare earth materials per car, primarily neodymium and dysprosium for drive motors. Electric vehicle sales reached 10.5 million units globally in 2022 according to the International Energy Agency, which translates to roughly 52,500 tons of rare earth consumption from EVs alone.

Defense Applications Command Premium Prices

Military applications command the highest prices for rare earth elements because defense contractors prioritize performance over cost. F-35 fighter jets contain 920 pounds of rare earth materials, including samarium for precision-guided munitions and erbium for fiber-optic communications. The Pentagon awarded $35 million in contracts to MP Materials in 2022 specifically for domestic rare earth supply chains. Defense spending creates stable demand that manufacturers can rely on regardless of economic cycles (unlike consumer electronics that fluctuate with market conditions).

Wind Energy Drives Massive Consumption Growth

Wind turbines represent the fastest-growing application segment, with each 3-megawatt turbine requiring 600 kilograms of neodymium for permanent magnet generators. By the end of 2022, companies had contracted a combined 77.4 GW of renewable energy, including 28.8 GW of wind power, which created significant demand for neodymium annually. China’s export restrictions in 2010 proved that countries controlling rare earth supplies hold significant leverage over high-tech manufacturing worldwide.

Green Technology Multiplies Future Demand

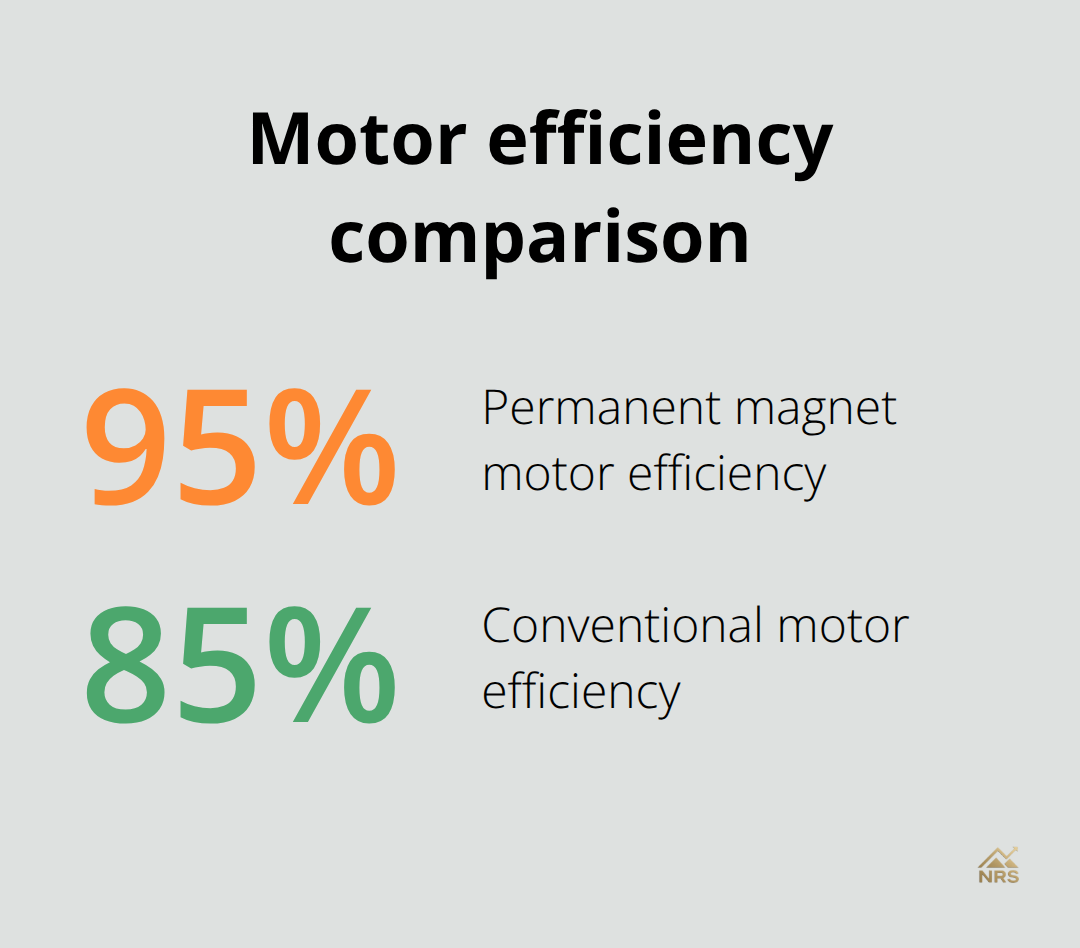

Renewable energy infrastructure creates exponential demand growth that traditional mining operations cannot match. Solar panels use indium and gallium, while battery storage systems require lithium and cobalt alongside rare earths for power electronics. The European Union allocated €6.2 billion through 2030 for critical materials including rare earths (recognizing supply chain vulnerabilities that threaten climate goals). Permanent magnet motors achieve 95% efficiency compared to 85% for conventional motors, which explains why manufacturers pay premium prices for neodymium despite supply constraints. Market analysts project rare earth demand will triple by 2030 as governments mandate electric vehicle adoption and renewable energy targets.

Final Thoughts

Rare earth minerals definition extends beyond technical specifications to encompass strategic investment opportunities that reshape global markets. We at Natural Resource Stocks track companies positioned to benefit from supply chain diversification as governments reduce dependence on Chinese production. MP Materials trades at $12 per share while Lynas Rare Earths commands $6.50, which reflects investor confidence in non-Chinese producers.

Market fundamentals support long-term growth with demand projected to reach 315,000 tons by 2030 compared to current production of 280,000 tons annually. The Pentagon invested $2.4 billion in domestic rare earth processing and created opportunities for established miners and exploration companies. Electric vehicle mandates across Europe and North America guarantee sustained demand growth that current supply chains cannot meet.

Supply chain vulnerabilities create national security concerns that drive government investment. The CHIPS Act allocated $52 billion for semiconductor manufacturing (which requires stable rare earth supplies for production equipment). Natural Resource Stocks provides expert analysis and market insights to help investors navigate this complex sector through video content, podcasts, and research that covers geopolitical factors impacting rare earth prices.