Silver is at an inflection point. Industrial demand from solar panels and electronics keeps climbing, while geopolitical tensions threaten supply chains and push investors toward hard assets.

At Natural Resource Stocks, we’ve analyzed the data behind a long-term silver forecast to help you understand where prices are headed and which stocks deserve your attention. This guide breaks down the opportunities ahead.

What’s Really Happening to Silver Supply and Demand Right Now

The Supply Crisis That Won’t Quit

In 2024, global silver mine production rose by 0.9 percent to 819.7 Moz, while demand exceeded 1.2 billion ounces. That creates a structural deficit, and this shortfall has now persisted for five consecutive years. The Silver Institute projects a 2025 deficit of 115 to 120 million ounces alone. Over the last four years, roughly 700 million ounces more has been consumed than mined-equivalent to about ten months of total mine output. This isn’t a temporary imbalance; it reflects a fundamental mismatch between what the world needs and what miners can produce.

The problem compounds because roughly 70 percent of silver comes as a byproduct of copper and gold mining, meaning miners cannot simply ramp up silver output in response to higher prices. Mining capacity additions remain delayed until 2027 and 2028 due to permitting and capital constraints, locking in supply tightness for at least another two years.

Industrial Demand Accelerates Faster Than Supply

Solar energy consumes more than 200 million ounces annually, representing about 20% of total silver demand, and this consumption rose again in 2025. The Silver Institute forecasts solar demand could nearly double between 2020 and 2030, with new TOPCon solar technologies requiring up to 50 percent more silver than traditional panels. Electric vehicle production adds another major demand vector, with EV silver demand jumping approximately 20 percent in 2025 as vehicles incorporate more sensors, high-voltage wiring, and power-management systems.

Global EV production is projected to exceed 15 million units in 2026, with each vehicle using roughly 1 to 2 ounces of silver.

AI data centers and semiconductors represent an emerging demand source, requiring silver for high-efficiency electrical components, precision contacts, and thermal management systems. Industrial demand now accounts for more than half of total silver consumption for the second consecutive year.

Physical Inventories Collapse Under Pressure

Available silver at the London Bullion Market Association has fallen by over 40 percent since 2020, with COMEX and LBMA good delivery bars tightening through 2024 and 2025. This inventory stress directly contributed to price spikes throughout 2025. Silver climbed from roughly $29 per ounce at the start of 2025 to above $72 by late December, a gain of 147 percent, marking a dramatic breakout beyond prior cycles.

The rally reflected both renewed investor participation and the reality of a market where demand structurally exceeds supply with no relief in sight. This price action sets the stage for understanding where silver heads next and which investment opportunities emerge as the market tightens further.

Where Silver Prices Head Over the Next Decade

Industrial Demand Drives the Long-Term Price Floor

Solar and electronics manufacturing will consume an estimated 300 million ounces of silver annually by 2030, up from roughly 230 million ounces in 2024. This 30 percent increase compounds because new TOPCon solar technologies require up to 50 percent more silver per panel than conventional designs. The Silver Institute projects cumulative solar demand through 2050 could consume 85 to 98 percent of known silver reserves, meaning the structural deficit we face today will intensify dramatically over the next five to ten years.

Electric vehicles add another 15 to 30 million ounces of annual demand by 2030 as production climbs toward 15 million units globally. Each vehicle incorporates roughly 1 to 2 ounces of silver across sensors, high-voltage wiring, and power-management systems. Semiconductors, 5G infrastructure, and AI data centers require silver for conductivity and thermal management, with no substitutes available at scale. These industrial applications are inelastic-manufacturers cannot reduce silver usage even if prices spike.

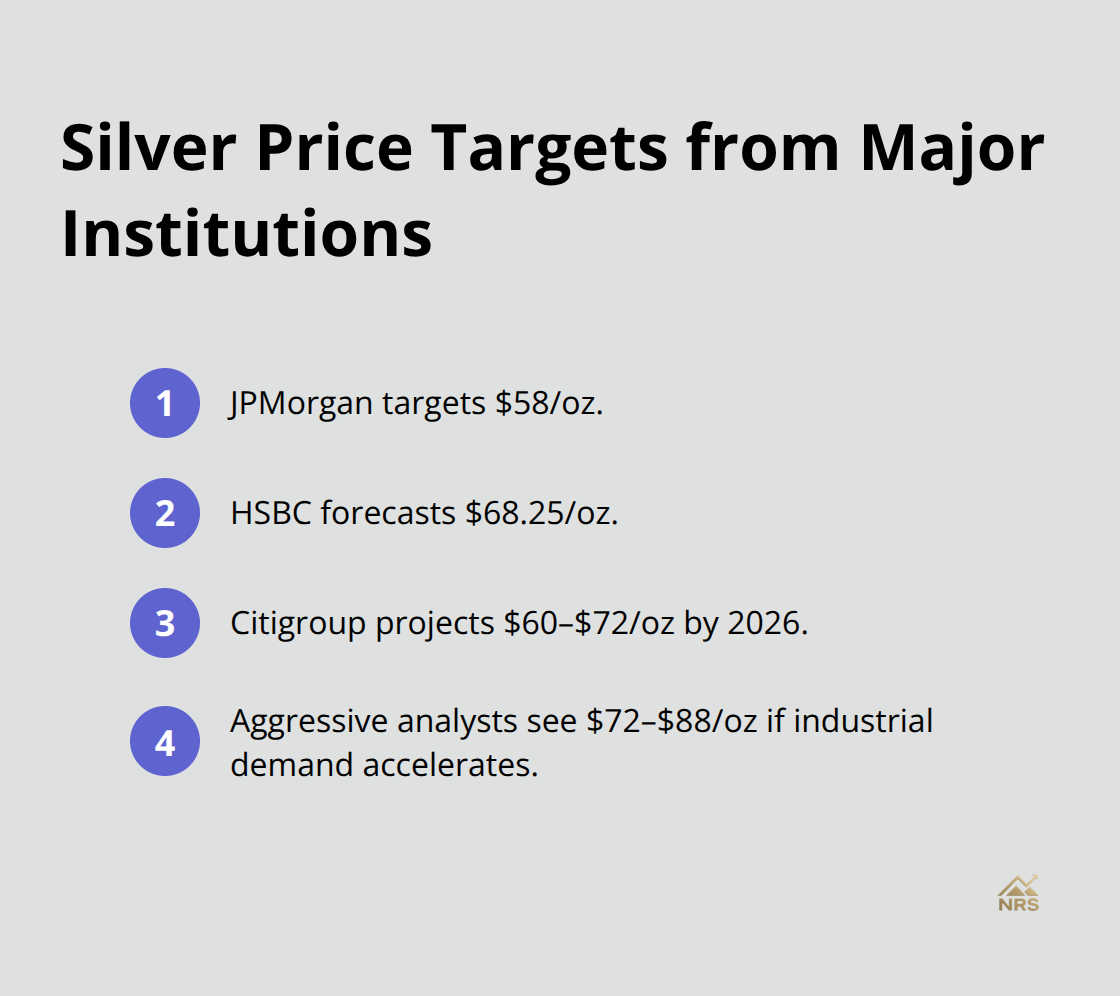

What Major Banks Expect Silver to Reach

Price projections from major institutions reflect this industrial reality. JPMorgan targets $58 per ounce, while HSBC forecasts $68.25 and Citigroup projects $60 to $72 by 2026. More aggressive analysts expect silver to trade in the $72 to $88 range if industrial demand accelerates as expected.

Industrial demand alone justifies higher prices without relying on investment speculation.

Investment Demand and Inflation Hedging Amplify Moves

Investment demand and inflation hedging will amplify price moves beyond what industrial consumption alone would drive. Federal Reserve rate cuts expected through 2026 weaken real yields and make non-yielding assets like silver more attractive relative to bonds. ETF inflows turned positive in 2025 after years of outflows, with Russia accumulating roughly $535 million in silver reserves and Saudi Arabia purchasing its first silver ETF, signaling sovereign demand shifting toward precious metals.

If inflation remains above the Federal Reserve’s 2 percent target through 2026, as most economists expect, silver functions as genuine portfolio insurance against currency debasement. This combination of industrial strength and monetary tailwinds creates a powerful backdrop for sustained price appreciation.

Geopolitical Risks Create Supply Shocks

Geopolitical risks in major mining regions amplify this dynamic considerably. Mexico and Russia produce significant silver volumes, and U.S.–China tariff tensions, Latin American nationalization trends, and mining-region instability create supply shocks that push prices higher. When geopolitical stress spikes, investors rotate into hard assets, and silver’s lower price point relative to gold makes it an accessible hedge for retail portfolios.

Building Your Silver Position for the Long Term

A 5 to 10 percent allocation to silver through physical metal or ETFs like SLV provides meaningful diversification without concentration risk. Try dollar-cost averaging into positions during pullbacks toward $50 to $54 per ounce to capture entry points while avoiding the trap of trying to time perfect bottoms. Expect volatility of 30 to 50 percent in some periods, but the underlying supply deficit and industrial demand trajectory support a base case around $65 per ounce or higher through 2026 and beyond.

With industrial demand locked in and geopolitical risks mounting, the question shifts from whether silver prices will rise to which mining stocks will capture the most value from this structural tightness. The next section examines the companies positioned to profit as silver markets tighten further.

Which Silver Stocks Deliver Real Returns

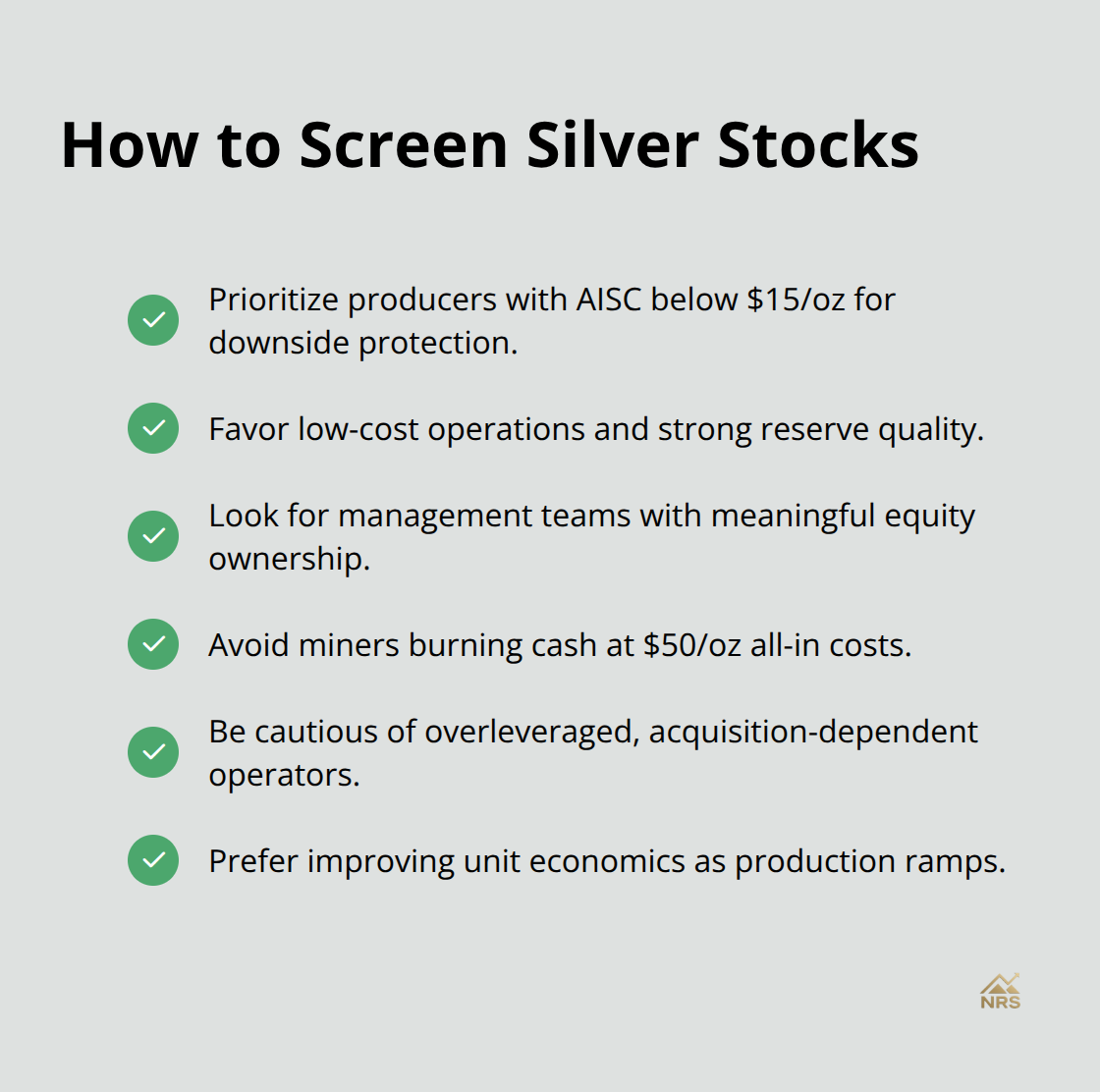

Screen for Production Costs First

The structural deficit and industrial demand outlined earlier translate directly into profit opportunities for mining companies positioned to capitalize on tightening markets. However, not all silver stocks move in lockstep with prices. Established producers with low-cost operations and exploration-stage companies with near-term production potential offer fundamentally different risk-return profiles. Evaluating silver stocks through the lens of production costs, reserve quality, and management execution separates smart allocators from those who chase momentum. A silver miner burning cash at $50 per ounce provides no margin of safety, while a producer with all-in costs below $12 per ounce generates substantial cash flow across a wide price range.

Start by screening for companies reporting all-in sustaining costs (AISC) in annual reports or investor presentations. Producers with AISC below $15 per ounce offer genuine downside protection and upside leverage as prices move toward $65 to $88.

Major Producers and Their Operational Advantages

Barrick Gold and Pan American Silver generate meaningful silver as a byproduct alongside their primary metals, giving them operational flexibility that pure-play silver miners lack. Endeavour Silver and First Majestic Silver operate primarily as silver producers and benefit directly from spot price appreciation, though their cost structures deserve scrutiny. The gold-silver ratio trading near 70-82 in 2026 suggests silver will outperform gold, meaning silver-focused operators capture disproportionate gains if that ratio compresses further toward historical bull-market levels of 40-60.

Exploration-Stage Companies and Resource Quality

Exploration-stage companies trading at modest market caps relative to their silver-equivalent resource bases present higher-risk, higher-reward opportunities for investors comfortable with volatility. Companies with high-grade deposits in jurisdictions with established mining infrastructure and favorable permitting records warrant closer examination than those in politically unstable regions. Reserve replacement matters critically over the next decade given the supply deficit, so companies actively expanding their resource bases through exploration success deserve preference over those managing existing reserves without meaningful additions.

Management Alignment and Execution Track Records

Evaluate management teams by checking whether executives hold meaningful personal stakes in their companies through equity ownership, signaling alignment with shareholder returns rather than executive compensation alone. Avoid overleveraged producers dependent on acquisition growth to offset declining ore grades, and instead prioritize companies with improving unit economics as production ramps. Companies with high-grade deposits in stable jurisdictions and proven management teams reduce execution risk substantially.

Building a Diversified Silver Stock Portfolio

A diversified approach across three to five quality producers with distinct geographic footprints, cost profiles, and development stages reduces single-company risk while maintaining meaningful exposure to the silver supply tightness ahead. Try dollar-cost averaging into positions during market pullbacks to capture entry points without timing pressure. This strategy captures the structural supply deficit and industrial demand acceleration while limiting exposure to any single company’s operational or geopolitical risks.

Final Thoughts

Silver’s structural supply deficit and accelerating industrial demand create a compelling investment case that extends well beyond 2026. The five-year supply shortfall shows no signs of reversing, while solar panel manufacturing, electric vehicle production, and semiconductor demand continue climbing. Major financial institutions project silver trading between $58 and $72 per ounce through 2026, with industrial consumption alone justifying sustained price appreciation regardless of investment sentiment or inflation hedging demand.

Your long-term silver forecast should account for two distinct but complementary strategies: physical silver or silver ETFs provide portfolio diversification and inflation protection without counterparty risk, making them suitable for conservative allocators seeking 5 to 10 percent precious metals exposure, while silver mining stocks offer leveraged exposure to price appreciation and generate cash flow from operations. Dollar-cost averaging into both physical metal and quality producers during pullbacks toward $50 to $54 per ounce captures entry points without timing pressure. Expect volatility of 30 to 50 percent in some periods as geopolitical risks spike and Federal Reserve policy shifts, but this volatility creates opportunities for disciplined investors willing to rebalance positions and add during weakness.

The supply tightness and industrial demand acceleration outlined throughout this analysis provide genuine downside protection at current price levels. We at Natural Resource Stocks provide expert analysis on precious metals markets, macroeconomic trends, and geopolitical impacts affecting resource prices. Visit Natural Resource Stocks to access detailed market analysis and build your investment strategy around the structural opportunities ahead in silver and other natural resource sectors.