Geopolitical tensions reshape how investors allocate capital across natural resource markets. Wars, sanctions, and regional conflicts create immediate ripple effects through supply chains, commodity prices, and currency values.

At Natural Resource Stocks, we’ve observed that understanding geopolitical risk implications is essential for positioning portfolios effectively. This guide walks through the specific ways conflicts and trade restrictions influence resource availability and investor behavior.

How Geopolitical Shocks Disrupt Resource Supply Chains

When conflicts freeze critical supply lines

Military conflicts and regional instability create immediate supply shocks in natural resource markets. Russia’s 2022 invasion of Ukraine demonstrated this vividly. Russian stock markets dropped 33 percent following the invasion, but the real damage extended far beyond equities. Russia supplies roughly 10 percent of global oil and accounts for a substantial share of palladium, nickel, and aluminum exports. The disruption forced buyers to scramble for alternative sources, pushing commodity prices sharply higher.

Energy stocks spiked globally as investors priced in scarcity, while firms with direct revenue exposure in Russia or Ukraine faced declines averaging around 2.5 percentage points according to IMF analysis. Direct conflict in a major producer region triggers immediate repricing and sourcing challenges for resource investors. Supply chain fragility means that even localized conflicts can affect your portfolio if you hold positions in companies dependent on affected regions.

Sanctions reshape resource flows and create winners

Trade restrictions and sanctions alter commodity flows in ways that create both disruption and opportunity. When Western nations imposed sanctions on Russian energy and metals after 2022, European buyers faced acute shortages and price spikes. However, sanctioned commodities found new buyers in Asia, particularly China and India, redirecting global trade patterns. The China-US tariff episodes from 2018 through 2024 hit Chinese firms with roughly 4 percent average declines after US tariff announcements, according to IMF data, while retaliatory measures depressed Chinese firms by an additional 0.3 to 0.7 percent depending on their cross-border exposure. Sanctions and tariffs function as structural portfolio risks because they alter the competitive landscape permanently. Companies that diversify sourcing across multiple jurisdictions or that operate in sanctioned-resistant regions gain competitive advantages. Currency instability amplifies these pressures. When geopolitical risk spikes, capital flows shift rapidly toward safe-haven currencies like the US dollar, Swiss franc, and yen, leaving emerging-market currencies vulnerable to sharp depreciation. A firm that earns revenue in a depreciating currency faces margin compression and reduced returns even if its underlying operations perform well. Resource companies with significant debt denominated in foreign currencies face additional pressure when their home currency weakens.

How capital reallocation accelerates during crises

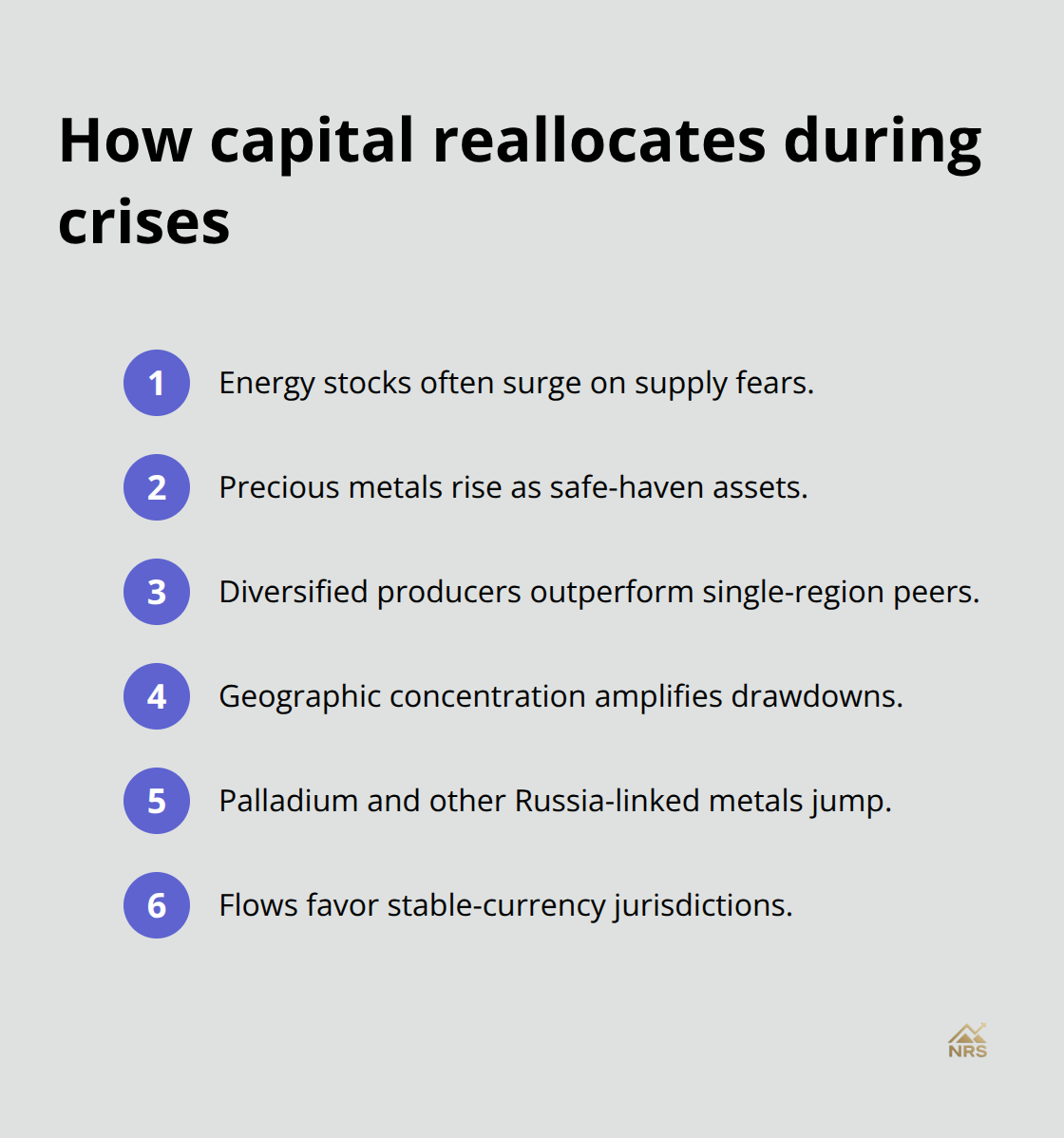

Geopolitical shocks trigger rapid capital reallocation across resource sectors. Investors reassess exposure to affected regions and redirect funds toward producers in geopolitically stable jurisdictions. This reallocation happens faster than supply chains can adjust, creating temporary price dislocations. Energy stocks benefit immediately from supply concerns, while metals producers face mixed signals depending on their geographic exposure. Firms with operations spanning multiple continents weather these storms better than single-region producers. The competitive advantage shifts toward companies with operational flexibility and diversified sourcing networks. Understanding these dynamics helps you anticipate which resource stocks will outperform during the next geopolitical episode.

How Geopolitical Shocks Reshape Portfolio Positioning

Geopolitical tensions spike, and investors move capital immediately toward assets perceived as safer or more resilient. This reallocation happens within days, not weeks, and it fundamentally changes which resource stocks outperform. The IMF’s Global Financial Stability Report from April 2025 documented that major geopolitical events trigger sovereign credit default swap spreads to widen in advanced economies and emerging markets within the first month. That widening reflects real capital flight. Investors rotate out of equities exposed to unstable regions and into precious metals, stable-currency government bonds, and energy stocks positioned to benefit from supply constraints. Gold prices typically climb during these episodes because the metal holds value regardless of which currency depreciates or which government defaults.

Capital flows reveal predictable patterns

The Russia-Ukraine invasion in February 2022 exemplifies how capital moves during crises. Stock markets fell 2.1 percent on the day of the invasion, with a total drawdown reaching 6.8 percent before recovery in 23 days according to LPL Financial data. However, energy stocks surged because Russia supplies roughly 10 percent of global oil.

Palladium, which Russia produces in significant quantities, jumped sharply higher. Investors who held diversified resource exposure benefited from the energy rally while those concentrated in single regions suffered losses. Geographic concentration amplifies geopolitical risk, while diversification across producing regions acts as a natural hedge.

Safe-haven flows create patterns that resource investors can exploit. US Treasury yields typically fall during global crises as capital seeks the safest destination, while emerging market yields spike as foreign capital exits. This dynamic benefits companies with US dollar revenues or those operating in geopolitically insulated jurisdictions. Precious metals rally because they serve as insurance against currency collapse and inflation uncertainty. The China-US tariff episodes from 2018 through 2024 showed that retaliatory measures depressed Chinese firms by 0.3 to 0.7 percent depending on their cross-border revenue exposure, yet mining companies with diversified customer bases weathered the shocks better.

Energy producers capture temporary advantages

Energy producers gain when geopolitical events threaten supply, as happened immediately after the Ukraine invasion when oil prices climbed above $100 per barrel. However, this benefit is temporary. Once supply chains adjust or new producers come online, energy stocks often retreat. The window for capturing geopolitical-driven energy gains narrows quickly, typically closing within weeks as markets reprice expectations. Resource investors who act decisively during the initial shock capture outsized returns, while those who hesitate miss the opportunity. The critical advantage lies in holding positions in companies with operational flexibility and geographic diversification before tensions escalate, not in trying to time entry points during the chaos.

Commodity-specific volatility demands differentiated positioning

Different commodities respond distinctly to geopolitical shocks based on their supply concentration and strategic importance. Oil and natural gas spike immediately when major producing regions face conflict because supply is inelastic in the short term. Palladium, which Russia dominates with roughly 70 percent of global supply, experiences extreme volatility when Russia faces sanctions. Nickel and aluminum, also Russian staples, face similar supply pressures. Rare earth elements present a different dynamic because China controls rare earth elements processing, making these elements vulnerable to US-China tensions rather than direct regional conflicts. Gold and silver climb during uncertainty regardless of the specific geopolitical event because they function as universal hedges.

Investors should weight portfolio allocations toward commodities with concentrated supply in stable regions and away from those dependent on geopolitically fragile producers. Companies that own assets in multiple jurisdictions or that can shift production between regions command premium valuations during crises because they offer optionality. A copper miner operating in both Chile and Peru has more flexibility than one operating only in Peru, and that flexibility translates into resilience when political instability threatens one region.

Identifying resilient resource companies

The practical approach involves identifying which resource companies operate across geographically diverse assets and which face single-region concentration risk. Overweight the former and underweight the latter before tensions spike. Companies with operational flexibility across multiple continents weather geopolitical storms better than single-region producers. The competitive advantage shifts toward those with diversified sourcing networks and the ability to redirect production or procurement when one region becomes unstable. This positioning matters most before crises hit, not after markets have already repriced the risk. Resource investors who understand these dynamics can position portfolios to capture opportunities that emerge when capital reallocates during the next geopolitical episode. The next section examines which specific regions currently pose the greatest supply risks and how resource availability in those areas shapes investment decisions.

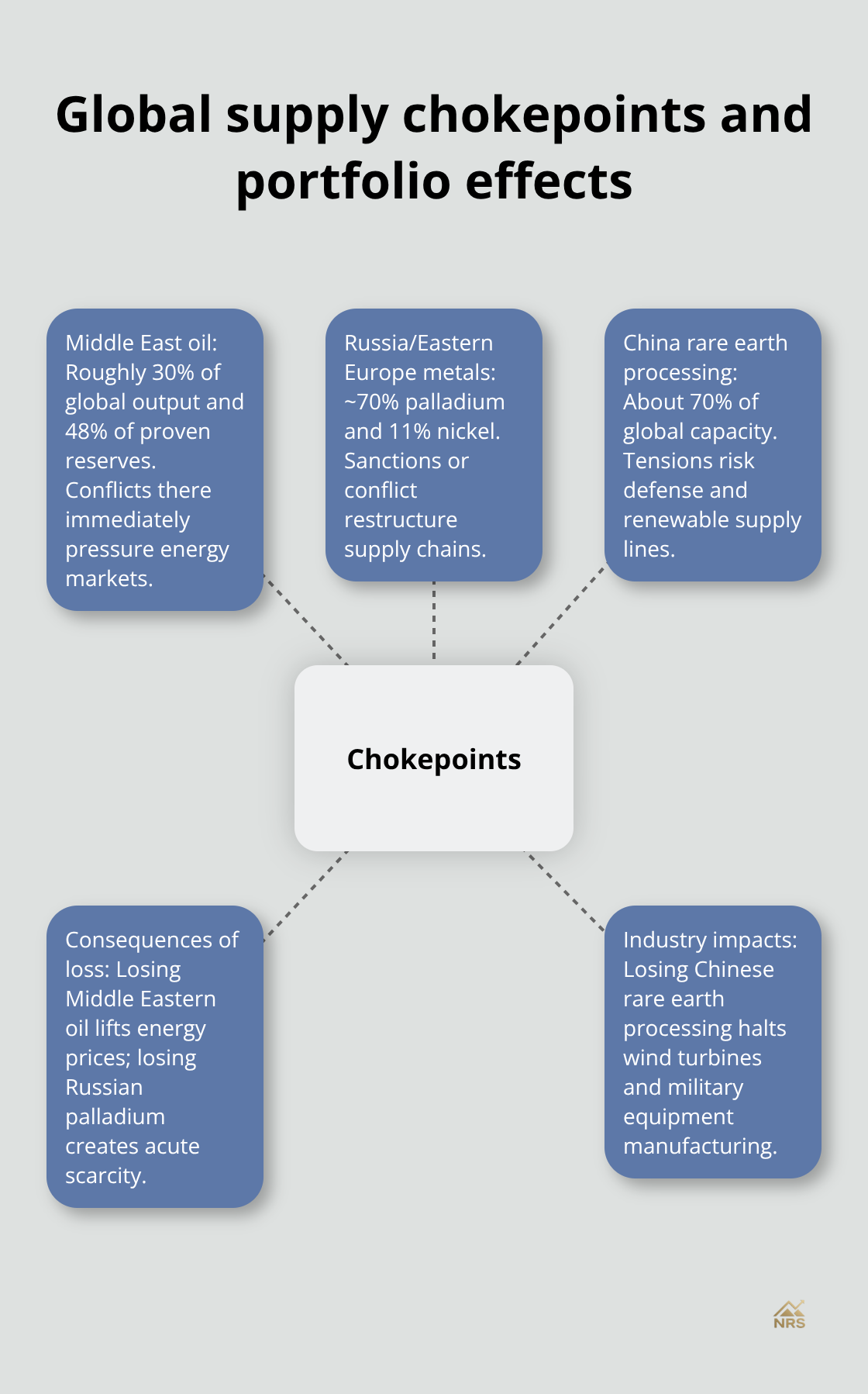

Where Global Supply Chokepoints Create Resource Scarcity

Three geographic regions control the vast majority of critical natural resource supply, and geopolitical instability in each creates distinct portfolio pressures. The Middle East produces roughly 30 percent of global oil and holds 48 percent of proven reserves, making regional conflict an immediate threat to energy markets worldwide. Russia and Eastern Europe supply approximately 10 percent of global oil, 70 percent of palladium, 11 percent of nickel, and substantial aluminum exports, meaning sanctions or military action there restructures entire commodity supply chains. China dominates rare earth element processing with roughly 70 percent of global capacity, making US-China tensions a direct threat to defense, renewable energy, and technology supply chains. These three regions are not interchangeable. Losing Middle Eastern oil pushes energy prices upward but leaves metals markets largely unaffected. Losing Russian palladium creates acute scarcity in automotive catalytic converters and electronics manufacturing. Losing Chinese rare earth processing halts wind turbine production and military equipment manufacturing.

Understanding which resources each region controls determines which portfolio positions survive geopolitical shocks and which collapse.

Middle East oil production faces escalating risks

Oil supply from the Middle East remains vulnerable to multiple geopolitical triggers. The Strait of Hormuz, through which roughly 20 percent of global oil passes, sits in one of the world’s most unstable regions. Iran’s nuclear program, Israeli-Palestinian tensions, and US-Iran hostilities create recurring supply concerns that spike oil prices within days. Middle East oil production vulnerability creates supply disruptions that ripple through global markets. Saudi Arabia, the region’s largest producer, faced drone and missile attacks on its refineries, most notably in September 2019 when attacks temporarily knocked offline 5 percent of global supply and sent oil prices spiking 20 percent intraday. These attacks proved temporary, but they revealed the fragility of the region’s infrastructure. Energy investors should position for higher baseline oil prices rather than betting on price stability. Companies with production outside the Middle East command premium valuations because they offer geographic hedges. A US-based oil producer or a Canadian tar sands operator gains competitive advantage during Middle Eastern crises because buyers pay premiums to source from stable regions.

Russian metal supply remains geopolitically weaponized

Russia’s metal exports face structural supply risk that extends beyond the initial Ukraine invasion. Palladium prices spiked 30 percent in the weeks following Russia’s 2022 invasion because automotive manufacturers and electronics producers depend almost entirely on Russian supply. Nickel and aluminum face similar concentration risk. These metals cannot be quickly substituted, meaning supply disruptions force buyers to accept higher prices or reduce production. Sanctions on Russian banks and the SWIFT payment system make purchasing Russian metals legally complicated and financially risky for Western companies, effectively reducing demand even when supply technically remains available. This dynamic benefits non-Russian metal producers significantly. Companies mining palladium in Zimbabwe or nickel in Indonesia gain market share and pricing power because buyers actively reduce Russian exposure. The competitive advantage extends to companies that can secure their supply chains from non-Russian inputs. An automotive manufacturer that sources palladium from non-Russian producers gains customer loyalty and operational certainty. A battery manufacturer that sources nickel from Indonesia rather than Russia reduces geopolitical risk and regulatory exposure. Resource investors should overweight metal producers in geopolitically stable regions and underweight those dependent on Russian sourcing relationships.

China’s rare earth stranglehold demands urgent attention

China controls rare earth element processing so completely that US-China tensions create immediate supply bottlenecks for defense contractors, renewable energy manufacturers, and technology companies. Rare earth elements appear in wind turbine generators, military radar systems, semiconductor manufacturing equipment, and electric vehicle motors. The US produces some rare earth ore but relies almost entirely on Chinese processing facilities to extract and refine usable materials. Chinese rare earth export restrictions would cripple US defense production and renewable energy deployment within months. Resource investors should recognize that rare earth element companies face unique geopolitical dynamics. Companies with processing capacity outside China, even if they operate at higher cost, command strategic value that pure mining operations cannot match. A rare earth refiner operating in the US or Japan gains pricing power and customer loyalty because buyers prioritize supply security over marginal cost differences. Direct exposure to rare earth mining companies operating in politically stable regions, particularly Australia and Canada, provides portfolio diversification away from Chinese processing concentration risk.

Final Thoughts

Geopolitical risk implications reshape which resource companies thrive and which struggle, alter commodity price trajectories, and determine which portfolios weather crises intact. The Russia-Ukraine invasion demonstrated that energy stocks rallied while firms with direct exposure suffered losses averaging 2.5 percentage points, and the China-US tariff episodes showed that retaliatory measures depressed Chinese firms by 0.3 to 0.7 percent depending on cross-border revenue exposure. These patterns repeat because capital flows follow predictable paths during geopolitical stress, with investors rotating toward safe-haven assets while energy producers benefit from supply concerns and companies with geographic diversification outperform concentrated competitors.

Resource investors who position portfolios strategically capture measurable advantages when tensions escalate. Overweight resource companies operating across multiple continents and underweight those dependent on single regions, since geographic diversification acts as natural insurance against localized shocks. Recognize that different commodities face distinct supply risks-Middle Eastern oil, Russian palladium and nickel, and Chinese rare earth processing each present unique vulnerabilities that demand differentiated allocation strategies based on your risk tolerance and time horizon.

Capital reallocation happens within days, not weeks, so monitor geopolitical developments continuously to identify opportunities before markets reprice expectations. We at Natural Resource Stocks track macroeconomic factors and geopolitical impacts that shape resource prices and investor behavior, providing expert analysis that helps you understand how regional conflicts, sanctions, and trade restrictions translate into portfolio opportunities. Visit Natural Resource Stocks to access market insights that inform your resource investment decisions during periods of heightened geopolitical tension.