Most investors overlook a simple fact: gold and silver move differently than stocks and bonds. This difference is exactly what makes gold and silver diversification powerful for protecting your wealth.

At Natural Resource Stocks, we’ve seen how adding these metals to a portfolio reduces overall risk while maintaining growth potential. The right mix of gold and silver can stabilize your returns when markets turn volatile.

Why Precious Metals Protect Wealth When Markets Crack

Gold and silver during market crashes have historically shown mixed performance during downturns. The 2008 financial crisis illustrates this clearly: while the S&P 500 fell roughly 57% from peak to trough, gold rose approximately 5% that same year. Silver proved more volatile, dropping initially before recovering sharply. This inverse relationship isn’t random-it reflects how investors flee to safety when equities collapse. Central bank purchases of gold reached record levels in recent years, reinforcing gold’s appeal as a monetary asset during periods of currency devaluation concern and geopolitical tension. Silver’s performance diverges from gold because industrial demand drives roughly half of silver’s consumption through electronics, solar panels, and automotive applications. When economies contract, industrial demand falls, pressuring silver harder than gold. Conversely, when economies expand, silver’s gains often outpace gold’s percentage returns due to its smaller market size and lower liquidity. This dual nature makes silver a tactical tool: it hedges inflation during growth phases while gold provides stability during downturns.

Metals Move Independently from Your Stock Portfolio

Gold and silver correlations to stocks and bonds hover near zero or turn negative during crises, meaning they genuinely diversify your holdings rather than moving in lockstep with equities. This matters practically: when your stock portfolio loses 20%, metals frequently gain or hold steady, offsetting losses. The gold-to-silver ratio currently sits around 50:1, having tightened from the long-run average of roughly 60:1, suggesting silver has outperformed significantly in this metals rally. Real interest rates and gold prices show a strong inverse relationship. According to research, the correlation between real interest rates and gold prices is -0.82, meaning when real yields fall, gold rises. High real rates punish gold; low real rates reward it. Silver responds similarly but with greater amplitude due to its industrial component.

Current Price Levels and Accessibility

At current price levels, with gold above $5,000 per ounce and silver breaking through $100 per ounce in late January, both metals remain accessible for diversification, though silver’s lower per-ounce price makes dollar-cost averaging into positions more straightforward for retail investors. You can build positions gradually without committing large sums upfront. This accessibility matters for investors who want to test their conviction in metals without overcommitting capital immediately.

Inflation Protection That Actually Works

Precious metals preserve purchasing power when currencies weaken. Historical price charts spanning back to 1915 show gold and silver rising alongside inflation spikes, though timing remains imperfect. The practical takeaway: metals hedge inflation better than cash sitting in low-yield accounts, but they require patience and proper positioning. Financial advisors typically recommend allocating 5% to 10% of a diversified portfolio to precious metals. This allocation level balances inflation protection against the reality that metals generate no yield and carry storage costs. If your portfolio currently holds no metals, this 5-10% allocation provides meaningful downside protection without dominating your overall strategy.

How to Position Metals Within Your Broader Strategy

The choice between gold and silver depends on your risk tolerance and market outlook. Gold serves as your portfolio’s anchor-the stable, non-correlated asset that protects wealth during crises. Silver amplifies returns when economies expand and industrial demand accelerates. A core-satellite approach works well here: maintain gold as a stable core holding while adding silver for potential higher gains and diversification. You can adjust this mix based on your macro outlook and whether you expect economic expansion or contraction ahead. The metals you select now will shape how your portfolio responds to the market conditions we explore in the next section.

Gold or Silver? Choose Based on Your Goals

Gold and silver serve fundamentally different purposes in a portfolio, and treating them identically is a mistake. Gold’s primary function is wealth preservation. It holds value during currency crises, geopolitical shocks, and banking instability. Silver, by contrast, derives more than half its demand from industrial applications-solar panels, smartphones, electric vehicles, medical devices, and electronics manufacturing. This industrial demand creates a key distinction: gold performs well during economic downturns and periods of financial stress, while silver tends to underperform when economies contract because factories slow production and industrial consumption drops. Gold and silver don’t play the same role in a portfolio, and understanding these differences is essential before committing capital. When you buy gold, you’re betting on stability and crisis protection. When you buy silver, you’re betting on economic expansion and industrial growth. This difference shapes everything about how you should allocate between them.

Silver Moves Faster Than Gold, for Better and Worse

Silver’s price volatility runs two to three times higher than gold’s daily swings, according to volatility analysis across major precious metals markets. A 5% move in gold might translate to a 10-15% move in silver on the same day. This amplification cuts both ways: silver gains accelerate during bull markets, but losses deepen during downturns. Silver’s higher beta means it outpaced gold significantly in recent rallies, with the gold-to-silver ratio tightening from historical averages. This outperformance tempts investors to overweight silver, but history warns against it. During economic slowdowns, silver’s industrial demand collapses faster than gold’s safe-haven demand rises, creating sharp drawdowns.

Risk Tolerance Determines Your Split

Your risk tolerance determines the split between these two metals. Conservative investors should anchor their position in gold-perhaps 70-80% of their metals allocation-and use silver as a smaller tactical position for growth. Aggressive investors comfortable with volatility can reverse this weighting, holding 60-70% in silver while keeping gold as a stabilizer. The allocation you choose today reflects how much portfolio turbulence you can tolerate without abandoning your strategy.

Match Your Allocation to Economic Expectations

The practical allocation decision hinges on what you expect economically over the next 12-24 months. If you anticipate recession, slowing industrial demand, or financial instability, shift toward gold. A 70% gold, 30% silver split provides meaningful upside from silver while keeping your portfolio anchored in the asset that historically gains during crises. If you expect continued economic expansion, renewable energy acceleration, and strong industrial demand, you can justify 50-60% silver and 40-50% gold. Electric vehicles use approximately three times more silver per vehicle than combustion-engine cars, creating a structural tailwind for industrial silver demand as EV adoption accelerates globally.

Operationalizing Your Gold-Silver Decision

Some investors use a 60-40 gold-to-silver split as a neutral starting point, then adjust based on their macro outlook. Financial advisors typically recommend keeping precious metals between 5-10% of total portfolio value, so your gold-silver decision operates within that constraint. If you allocate 7% to metals, that might mean 4.2% in gold and 2.8% in silver under a 60-40 approach. The key is intentionality: decide whether you’re positioning for economic resilience or economic growth, then weight your metals accordingly rather than splitting them equally. Once you’ve settled on your gold-silver ratio, the next critical question becomes how to actually own these metals-a choice between physical bullion, mining stocks, and ETFs that fundamentally changes your risk profile and tax treatment.

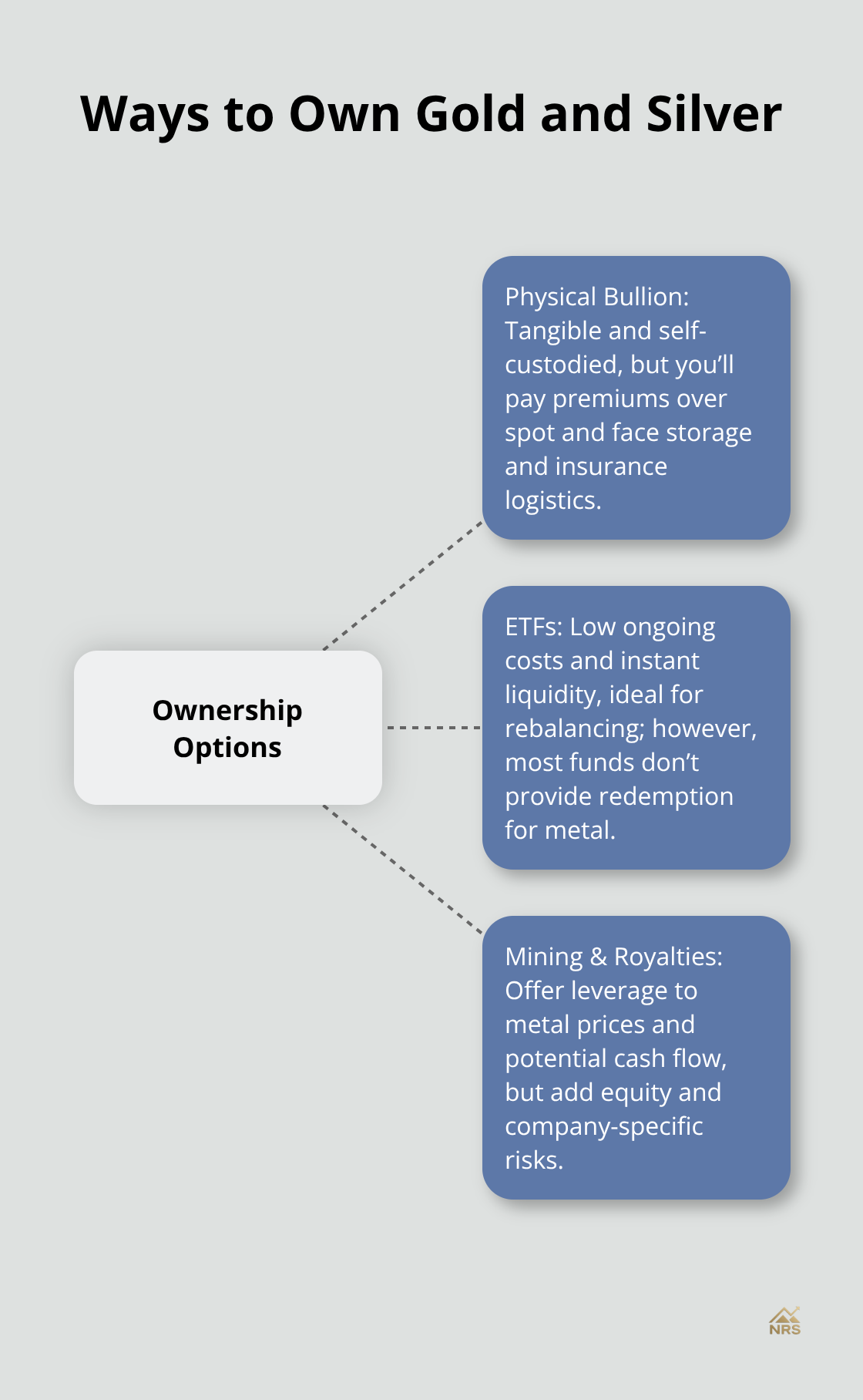

How to Own Gold and Silver

You’ve decided on your gold-to-silver ratio. Now comes the harder part: actually owning these metals. Three distinct pathways exist, and each carries different costs, tax consequences, and practical considerations that dramatically affect your real returns. Physical bullion feels tangible and secure but demands storage solutions and upfront premiums above spot prices.

ETFs offer liquidity and simplicity while eliminating storage headaches, yet you never touch actual metal. Mining stocks and royalty companies provide leveraged exposure to metal prices alongside operational cash flow, but introduce equity risk and company-specific volatility unrelated to metal prices themselves. The path you choose matters more than the metals themselves because fees, taxes, and accessibility will either compound your gains or erode them over years.

Physical Metals Demand Honesty About Real Costs

Buying physical gold and silver means paying spot price plus a dealer premium that typically ranges from 2% to 8% depending on the form and seller. A one-ounce gold coin might cost $5,200 when spot gold trades at $5,000, meaning you start underwater immediately. Silver premiums often run higher on a percentage basis, sometimes reaching 10-15% for smaller quantities. These premiums aren’t negotiable myths-they’re real money that must be recovered through price appreciation before you see any profit. Storage and insurance compound these costs further. Home storage eliminates third-party fees but introduces theft and security risks; most serious investors use bank safe deposit boxes or professional vault services costing $100-300 annually depending on quantity. Insurance typically runs 0.5-1% of your holdings’ value annually. A $50,000 physical metals position could cost $300-500 yearly in storage and insurance alone. The Federal Trade Commission warns that these costs accumulate faster than many investors anticipate, and comparing premiums across multiple dealers before purchasing is non-negotiable. Physical metals make sense if you believe in worst-case scenarios like banking system collapse or hyperinflation-situations where digital assets become inaccessible. For most diversification purposes, however, the friction costs and illiquidity create headwinds that favor alternative approaches.

ETFs Offer Simplicity at the Cost of Ownership

Gold ETFs like GLD, IAU, and GLDM track spot prices with expense ratios between 0.18% and 0.40% annually-a fraction of physical storage costs. Silver ETFs including SLV and SIVR operate similarly. These funds provide instant liquidity, meaning you can sell your position in seconds during market hours without hunting for buyers or dealing with shipping complications. Tax treatment differs from physical metals; ETFs typically generate capital gains rather than collectibles taxation, though you should verify specific fund prospectuses since rules vary. The critical limitation: most ETFs don’t allow redemption for physical metal, meaning you own a claim on metal held by a custodian rather than metal itself. Only specialized funds like Sprott Physical Gold Trust or the Perth Mint’s offerings provide redemption rights for actual bullion. This distinction matters less during normal market conditions but becomes relevant during extreme scenarios where counterparty risk surfaces. ETFs work brilliantly for portfolio diversification and tactical adjustments. You can rebalance between gold and silver in minutes without premium friction. Some sophisticated investors employ option-weaving strategies with ETFs, selling cash-secured puts on depressed metals to collect premiums while waiting for assignments, then using covered calls to harvest additional income. This income-generation approach converts static precious metals holdings into yield-producing positions, though it requires active management and options experience.

Mining Stocks and Royalties Offer Leverage With Complications

Mining stocks amplify metal price movements but introduce operational risk that metal ownership avoids entirely. A 10% gold price increase might drive a 20-30% surge in a gold miner’s stock due to operational leverage-fixed costs stay constant while revenues rise sharply, boosting profits disproportionately. Conversely, a 10% price decline can slash mining profits by 30-50%, creating downside amplification that pure metals don’t experience. All-in Sustaining Costs for major gold miners measure the total cost per ounce of producing gold, with top performers achieving competitive margins. When gold prices approach these cost floors, miners face margin compression and potential production cuts, which can create price support during downturns. Royalty and streaming companies like Franco-Nevada, Royal Gold, and Wheaton Precious Metals occupy middle ground between metals and miners. These firms own long-term contracts granting them rights to a percentage of mine production in exchange for upfront capital. They generate steady cash flow without operational headaches, and historically have outperformed gold itself during bull markets while providing downside protection during declines. Newer entrants including Osisko Gold Royalties, Sandstorm Gold, Metalla, and Maverix Metals offer similar structures with potentially higher growth profiles but less operational history. The practical allocation we recommend emphasizes starting with physical metals or ETFs for core diversification, then layering in selective mining or royalty exposure only if you understand the additional risks and can commit to research. Mining stocks suit aggressive investors with conviction about metals and tolerance for 30-40% drawdowns. Conservative investors should stick with metals and royalties rather than pure mining plays.

Final Thoughts

Gold and silver diversification works because these metals operate independently from stocks and bonds while serving distinct portfolio functions. Gold anchors your position with stability during crises, while silver amplifies gains when economies expand. The allocation strategy you choose depends entirely on your risk tolerance and economic outlook over the next 12-24 months, with conservative investors weighting toward gold and aggressive investors justifying higher silver exposure given its industrial demand tailwinds from electric vehicle adoption and renewable energy acceleration.

Your ownership method matters as much as the metals themselves. Physical bullion provides tangible security but demands patience with premiums, storage costs, and illiquidity, while ETFs offer simplicity and tax efficiency without ownership friction. Mining stocks and royalty companies introduce leverage and cash flow but require deeper research and higher risk tolerance, so most investors benefit from starting with ETFs or physical metals as their core position before selectively adding royalty exposure.

Long-term wealth building with precious metals succeeds when you treat them as portfolio insurance rather than speculation. The 5-10% allocation range balances meaningful downside protection against the reality that metals generate no yield, and real returns depend on recovering premiums and fees through price appreciation. Start implementing your metals strategy by defining your gold-to-silver ratio based on your macro outlook, then selecting your ownership method based on your lifestyle and tax situation-compare premiums across dealers if buying physical metals, and verify ETF expense ratios before committing capital to Natural Resource Stocks for expert analysis and market insights on precious metals allocation within your broader resource investment strategy.