Silver as an inflation hedge sounds good in theory, but the reality is messier. We at Natural Resource Stocks have watched silver fail to deliver consistent protection during inflationary periods, despite what conventional wisdom suggests.

The metal’s price movements tell a different story than inflation rates do. This blog post breaks down what actually drives silver prices and how to think about it in your portfolio.

Does Silver Actually Rise When Inflation Accelerates?

The 1970s: A Misleading Success Story

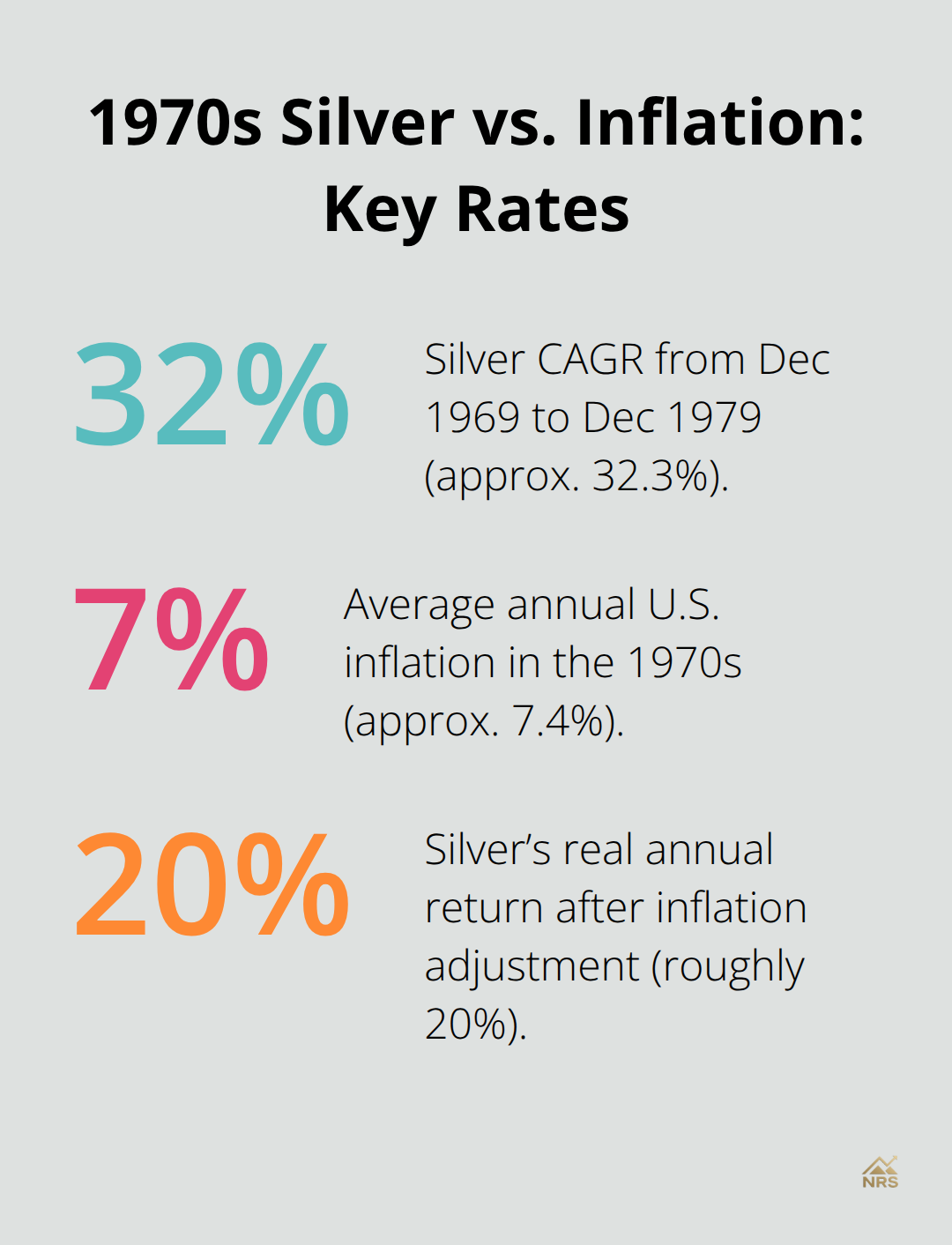

The 1970s offer the clearest evidence that silver responds to inflation spikes. From December 1969 to December 1979, silver climbed from $1.83 per ounce to $30.13 per ounce-a compound annual growth rate of 32.3%-while inflation averaged 7.4% annually. That same decade, silver delivered a 1,546% total return, far outpacing cash and bonds. The numbers look compelling at first glance. But here’s where the narrative breaks down: silver’s performance during that period was driven as much by the Hunt Brothers’ speculative buying in 1980 (when silver briefly spiked to $50.35 per ounce) as it was from inflation itself.

Real returns matter more than nominal prices. During the 1970s, silver’s real return after inflation adjustment reached roughly 20% annually, which is genuinely strong. However, this performance was an outlier, not a reliable pattern. The decade’s extreme conditions-oil shocks, currency instability, and rampant speculation-created an environment that won’t repeat itself.

Recent Inflation Cycles Tell a Different Story

The COVID-19 era provides a more recent test case. Silver surged approximately 70% from March 2020 lows near $12 per ounce to May 2021, when inflation concerns had risen to 7%. That sounds like textbook inflation hedging. Yet when you examine the 2008 financial crisis recovery, silver climbed roughly 387% from crisis lows below $10 to around $48.70 by 2011-a period when inflation remained subdued. This reveals the uncomfortable truth: silver rises during periods of economic uncertainty and when investors fear currency debasement, not necessarily from inflation actually accelerating.

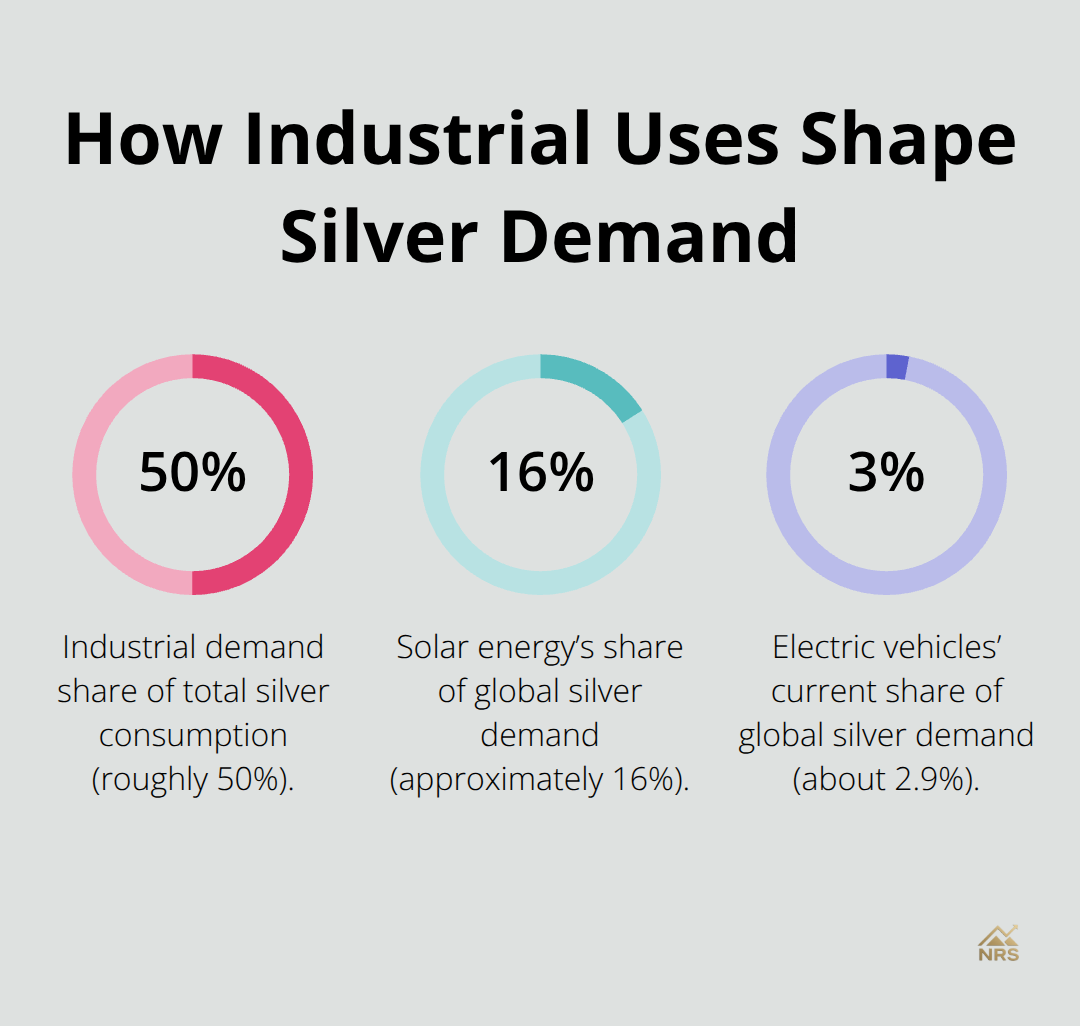

Total silver demand fell by 3 percent to 1.16 billion ounces in 2024, with solar energy driving approximately 16% of global demand and growing around 14% annually. This means silver’s price depends heavily on manufacturing output and renewable energy investment cycles, factors disconnected from inflation rates. Compare silver to gold during the same periods: gold’s correlation with CPI in high-inflation regimes reaches 0.7 to 0.9, making it the more reliable inflation hedge. Accelerating inflation without rate increases does favor metals as currency protection, yet silver’s correlation weakens significantly in moderate inflation environments.

What Academic Research Reveals

The data from academic research covering monthly returns from January 1975 to October 2023 shows gold responds sharply to inflation spikes while silver’s response remains subdued, especially when inflation accelerates rapidly. Silver excels as a complement to gold during transitions between economic cycles, not as a standalone inflation protection tool. The research demonstrates that silver’s price movements stem from multiple sources-industrial demand, investor sentiment, and currency fluctuations-rather than inflation alone. If inflation averages 2.5 percent annually through 2050 and silver prices rise 4 percent per year in nominal terms, the real price barely moves, illustrating how nominal gains can mask weak real returns.

Current Market Conditions and Positioning

Silver trades around $30 to $35 per ounce as of mid-2025, with UBS forecasting average prices of $36 to $38 for the year. The gold-to-silver ratio sits around 91:1, well above the long-run average of 65:1, suggesting potential upside if the ratio reverts toward historical norms. However, this potential gain has nothing to do with inflation hedging and everything to do with mean reversion and industrial demand recovery. Dollar-cost averaging through regular monthly investments reduces timing risk and smooths volatility.

Understanding silver’s actual price drivers matters far more than chasing the inflation hedge narrative. The metal responds to forces that extend well beyond consumer price indices, which means your portfolio strategy should account for these multiple influences rather than treating silver as a simple inflation solution.

Why Silver Fails as a Reliable Inflation Hedge

Industrial Demand Drives Price, Not Inflation

Industrial demand accounts for roughly 50% of total silver consumption, and this demand fluctuates based on manufacturing cycles, not inflation rates. Solar energy drives approximately 16% of global silver demand and grows around 14% annually, meaning silver prices rise and fall with renewable energy investment trends rather than consumer price indices. When solar installations slow due to policy changes or financing constraints, silver demand drops regardless of inflation levels. The electric vehicle sector currently accounts for about 2.9% of global silver demand, with projections suggesting this could intensify significantly toward 2050.

This industrial dependency creates a fundamental problem: silver prices respond to business cycles and capital expenditure patterns, not to the purchasing power of currency.

Historical Crises Reveal the Real Driver

During the 2008 financial crisis, silver climbed 387% from lows below $10 to $48.70 by 2011 while inflation remained subdued. This wasn’t inflation hedging-investors fled equities and sought alternative assets. The 2020-2021 period showed similar dynamics. Silver surged 70% from $12 per ounce to May 2021 peaks as investors feared currency debasement, but real inflation-adjusted returns tell a different story. Real returns reached about 15% annually during 2020-2021, which looks strong until you compare it to the 1970s real returns of 20% annually. The 1970s had extreme geopolitical conditions that won’t repeat, making that decade an outlier rather than a reliable benchmark.

Volatility Disconnects from Inflation Rates

Silver’s volatility exposes the inflation hedge weakness. The metal swings wildly in response to shifts in investor risk appetite and central bank policy, movements completely disconnected from inflation acceleration. When the Federal Reserve signals rate cuts, precious metals rally regardless of inflation data. Conversely, when the Fed tightens policy to fight inflation, silver often declines because higher rates increase the opportunity cost of holding non-yielding assets. Gold has shown strong performance across eight market scenarios over 50 years, proving itself a cycle-tested portfolio protector, while silver’s response remains subdued during inflation spikes.

Currency Movements Override Inflation Protection

Currency movements amplify this problem significantly. Silver prices denominated in US dollars mean that a strong dollar reduces silver’s purchasing power for international buyers, even if inflation accelerates. A weak dollar can push silver prices higher without any inflation acceleration occurring. During periods of dollar strength, silver prices have fallen despite rising inflation expectations. This currency overlay fundamentally undermines silver’s ability to protect purchasing power consistently.

Multiple Forces Create Conflicting Pressures

If you hold silver to hedge inflation, you face three competing forces: inflation itself, industrial demand cycles, and currency movements. Gold remains the more reliable choice because its correlation with inflation holds across different economic regimes. Silver works better as a diversification play within a broader precious metals strategy rather than as a standalone inflation solution. Understanding what actually moves silver prices matters far more than chasing the inflation hedge narrative. The metal responds to forces that extend well beyond consumer price indices, which means your portfolio strategy must account for these multiple influences. The real question becomes: what factors actually drive silver prices when inflation alone cannot explain the movements?

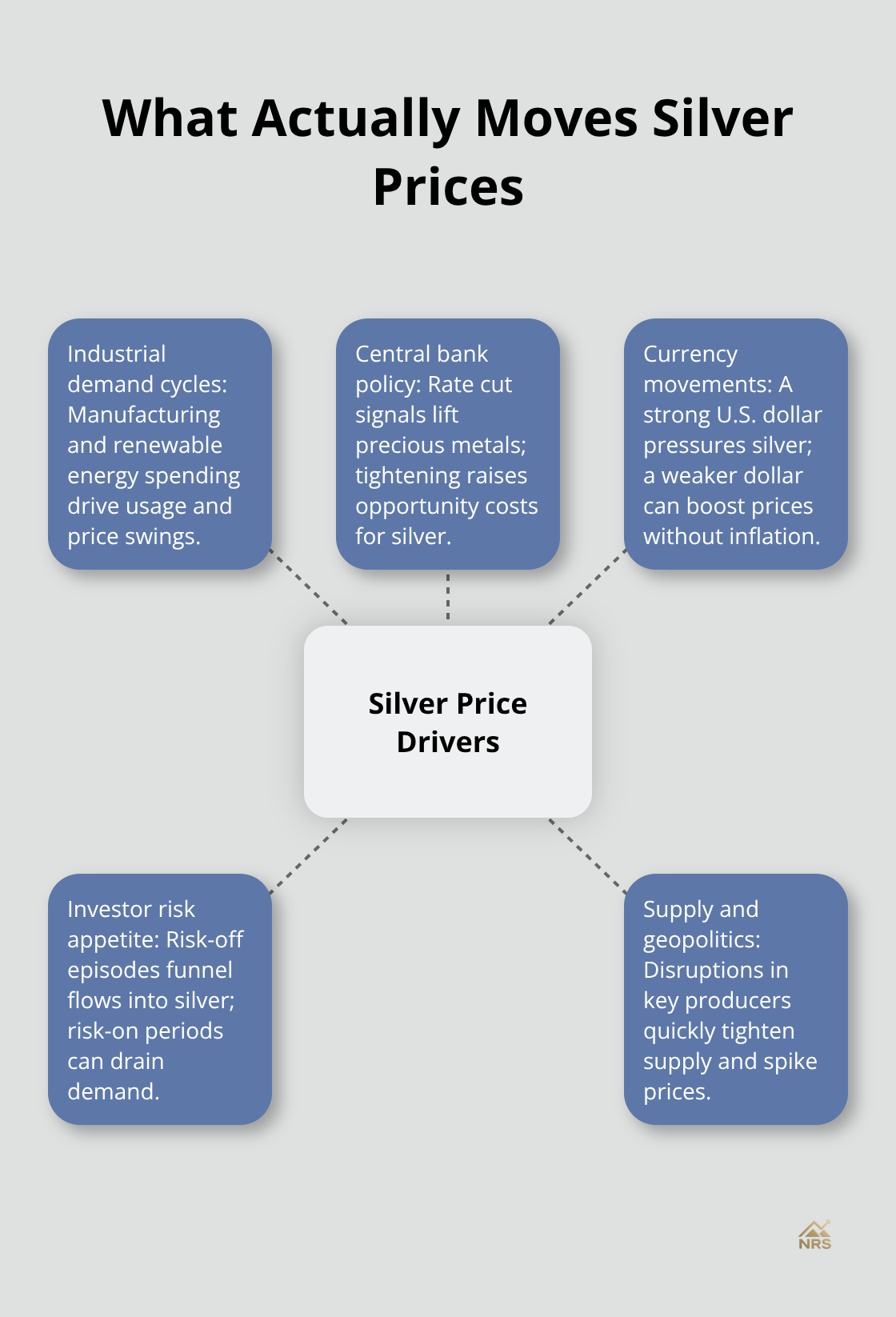

What Actually Moves Silver Prices

Supply Disruptions Create Immediate Price Pressure

Supply disruptions and geopolitical tensions create immediate price pressure that inflation rates cannot explain. Mexico’s mining reforms could affect roughly 5% of projected silver output, while Russia and Mexico together account for approximately 21% of global production, making geopolitical risk a constant factor in silver valuations. When tensions rise in major producing regions, silver prices spike within days, regardless of inflation data. The IMF downgraded 2025 global growth to 2.8% from 3.3% in January due to trade tensions, a backdrop historically favorable to precious metals as safe-haven assets. However, this safe-haven demand reflects investor fear about economic disruption and currency stability, not inflation protection. Supply constraints create a floor under prices, but they also create volatility that disconnects silver from inflation trends entirely. Track production announcements and geopolitical developments in Mexico, Russia, and Peru rather than waiting for inflation reports to predict movement.

Central Bank Policy Drives Silver More Than Consumer Prices

The Federal Reserve’s June 2025 projections showed core PCE inflation at about 3.1%, with only two rate cuts anticipated for the year, yet this information matters far less for silver than the Fed’s actual rate decisions. When central banks signal rate cuts, precious metals rally as investors flee low-yielding bonds and cash. When the Fed tightens policy to combat inflation, silver often declines because higher interest rates increase the opportunity cost of holding non-yielding assets. This inverse relationship to policy, not inflation itself, explains much of silver’s price movement. Monitor Fed commentary and rate expectations more closely than inflation data if you want to anticipate silver price direction. The gold-to-silver ratio at 91:1, compared to the long-run average of 65:1, reflects current monetary policy expectations and risk sentiment rather than inflation differentials between the metals.

Investor Risk Appetite Determines Silver Demand

When equity markets sell off and investors fear recession, silver rallies as part of broader precious metals demand. When equity markets surge and confidence returns, silver often declines despite stable or rising inflation. The 2008 financial crisis saw silver climb 387% from lows below $10 to $48.70 by 2011 during a period of subdued inflation, proving that investor sentiment drives price action far more than consumer price indices.

This means silver behaves like a risk-off asset first and an inflation hedge second. Dollar-cost averaging through regular monthly investments matters more than timing entry points based on inflation forecasts, because you cannot predict when investor sentiment will shift. Watch equity market volatility and credit spreads as leading indicators for silver price direction, not inflation expectations. The metal’s dual role as both monetary asset and industrial commodity means price action reflects multiple competing forces simultaneously, making inflation alone an unreliable predictor of silver movement.

Final Thoughts

Silver as an inflation hedge carries appeal, but the evidence shows it delivers inconsistent protection at best. We at Natural Resource Stocks have examined the data extensively, and the pattern is clear: silver responds to multiple forces simultaneously-industrial demand cycles, central bank policy, geopolitical tensions, and investor risk appetite-making inflation alone an unreliable predictor of price movement. The metal rises during financial crises when investors flee equities, climbs when central banks signal rate cuts, and swings wildly based on manufacturing output, none of which guarantees purchasing power protection when inflation accelerates.

This doesn’t mean silver has no place in your portfolio. It means treating silver as a partial hedge within a diversified strategy works better than relying on it as your primary inflation protection. Gold remains the stronger choice for consistent inflation correlation, particularly during high-inflation regimes where its correlation with CPI reaches 0.7 to 0.9, while silver complements gold by capturing industrial demand exposure and providing volatility that can enhance returns during specific economic transitions. A practical allocation of 5 to 10 percent of portfolio value to silver, combined with gold holdings, balances inflation protection with realistic expectations about what each metal actually delivers.

Dollar-cost averaging through regular monthly investments matters more than timing entries based on inflation forecasts, as this approach smooths volatility and removes the burden of predicting when silver will respond to inflation versus when it will move based on Fed policy or geopolitical tensions. Monitor the gold-to-silver ratio, track central bank commentary, and watch equity market volatility as leading indicators, since these factors predict silver movement far better than inflation data alone. Explore our analysis on macroeconomic factors affecting resource prices to refine your approach and understand what actually moves silver valuations.