Rare earth elements power everything from smartphones to wind turbines, yet most investors overlook this critical market. The rare earths market outlook hinges on three forces: China’s stranglehold on production, surging demand from electric vehicles, and a recycling revolution that could reshape supply chains.

We at Natural Resource Stocks believe understanding these dynamics is essential for spotting the next generation of resource opportunities.

Where Rare Earths Stand Today

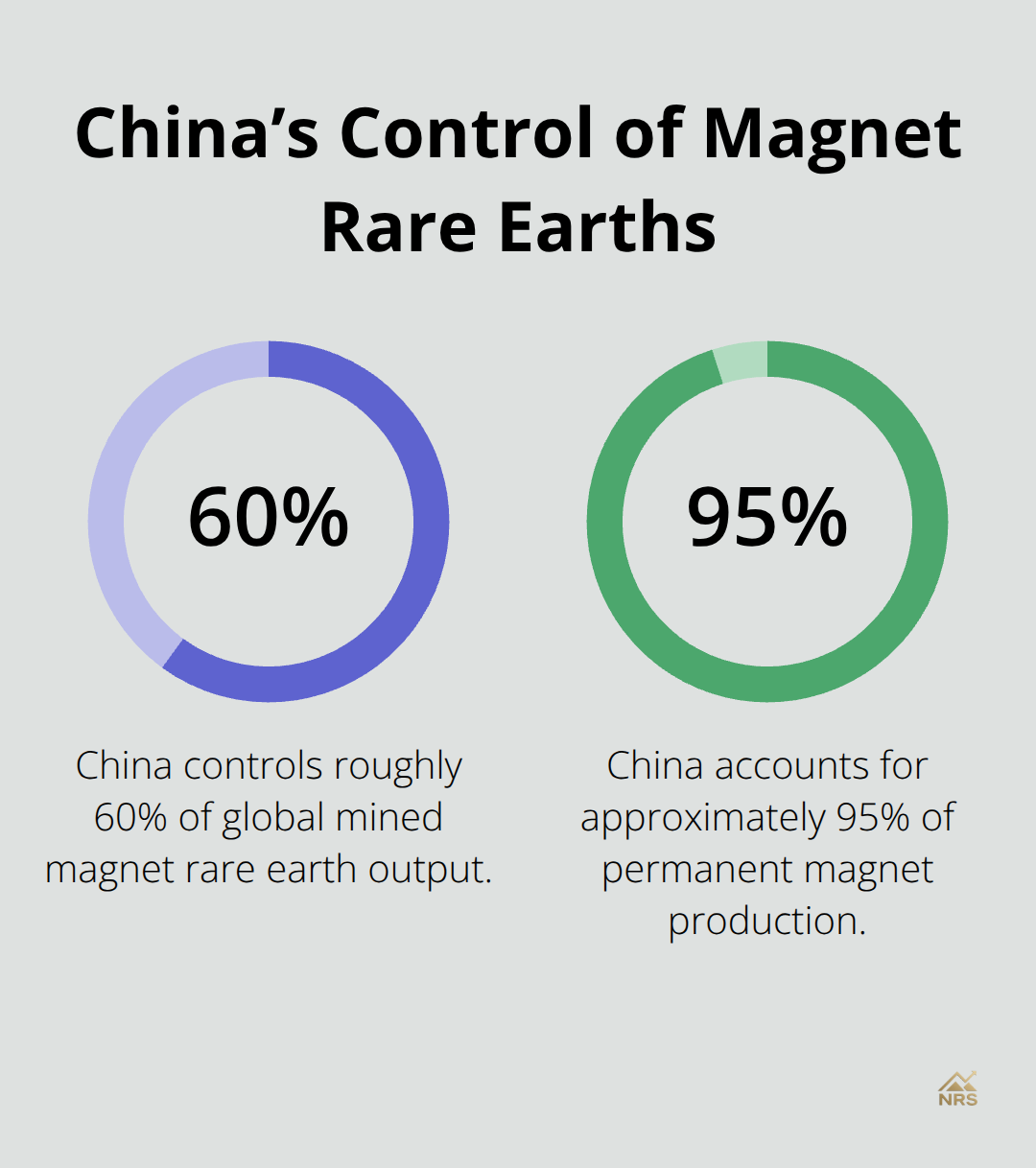

The rare earths market reached approximately 4 billion dollars in 2024, with projections pointing toward 6.3 billion by 2030 according to recent market analysis. That represents roughly 8 to 9 percent annual growth, which is substantial but masks a far more critical reality: production bottlenecks constrain the market severely, making supply the defining factor for investors. Global magnet rare earth demand has doubled since 2015 and will grow more than 30 percent by 2030. China controls roughly 60 percent of global mined magnet rare earth production, over 90 percent of refining capacity, and approximately 95 percent of permanent magnet production. When China implements export controls, as it did in 2025, consequences ripple instantly through downstream supply chains. Those 2025 export controls caused immediate input shortages and reduced production for manufacturers outside China, signaling that geopolitical risk translates directly into market volatility.

Mining and Refining Reality

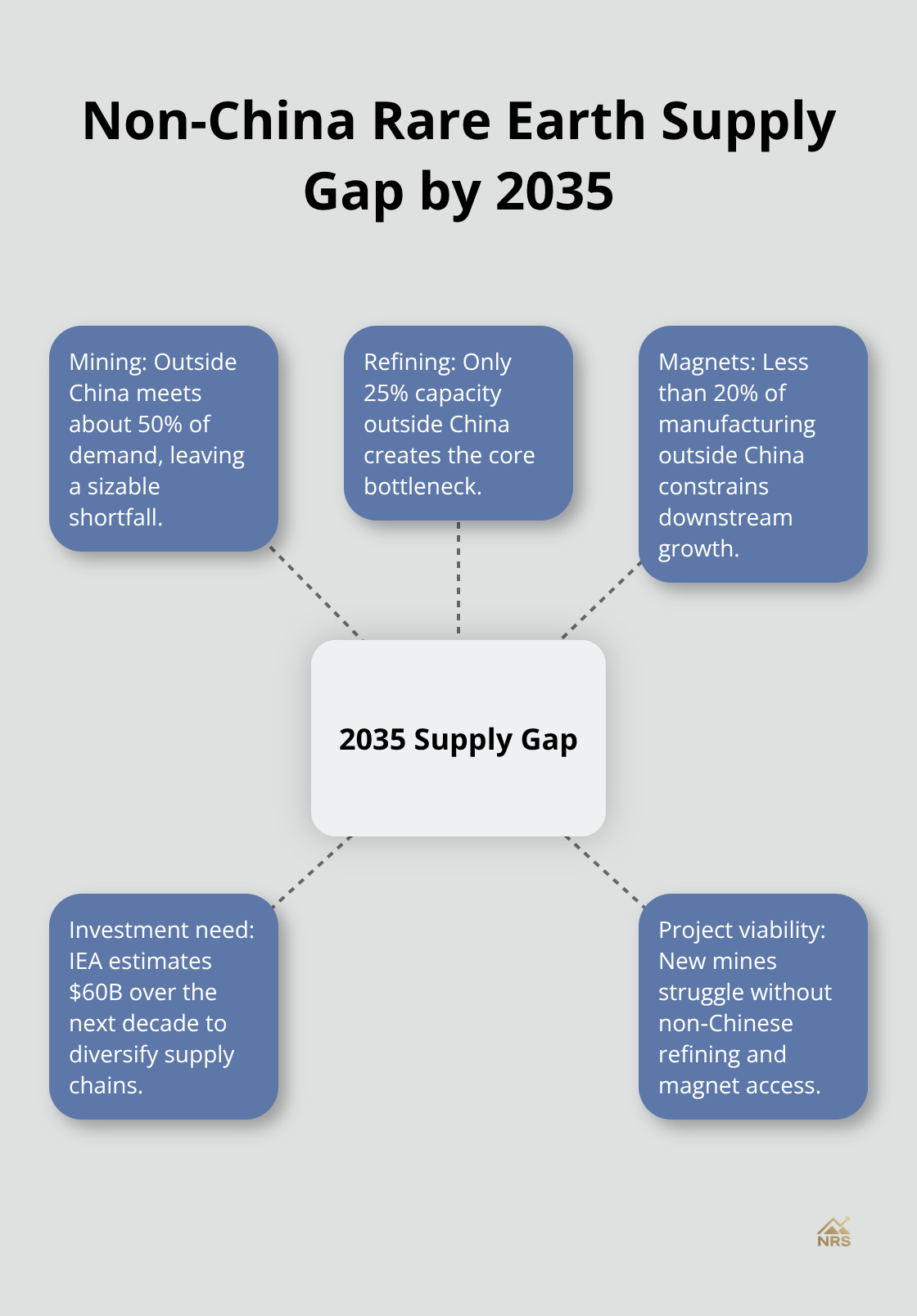

The production numbers reveal why supply remains the binding constraint. Outside China, mining capacity will cover only about 50 percent of demand by 2035, while refining capacity will cover just 25 percent, and magnet manufacturing less than 20 percent. This widening gap explains why projects like Apex Critical Metals’ Rift deposit in Nebraska matter significantly to investors. Recent drilling at Rift returned 81.6 meters at 2.02 percent rare earth oxide with a highly enriched neodymium-praseodymium zone that averages 49 percent NdPr over 10 meters. That concentration is exceptional because typical carbonatite deposits show neodymium-praseodymium distributions of 14 to 20 percent, making Rift’s mineralization substantially more valuable per ton of ore. The 2026 drill program at Rift comprises eight holes totaling approximately 5,868 meters, with assays pending and 3D geological modeling underway.

Magnet Manufacturing Acceleration

Domestic magnet production finally materializes. USA Rare Earth commissioned its commercial sintered neodymium-iron-boron magnet production line in Stillwater, Oklahoma, with commercial output expected in the second quarter of 2026. More significantly, MP Materials is building a 120-acre magnet manufacturing campus in Northlake, Texas, with over 1.25 billion dollars in investment and over 1,500 jobs, targeting approximately 10,000 metric tons annually of neodymium-iron-boron magnets by 2028. These projects represent the first genuine steps toward a fully integrated U.S. supply chain from mining through magnet production. Investors should monitor commissioning timelines and production ramp rates for these facilities because they directly determine whether U.S. and allied nations can reduce dependence on Chinese magnet supply.

Price volatility will remain elevated until downstream magnet manufacturers gain confidence in alternative supply sources outside China.

What Comes Next

The supply constraints we see today set the stage for the next critical challenge: whether technological innovation and recycling can ease pressure on the most constrained rare earth elements. Understanding these emerging solutions requires examining how the industry approaches secondary sources and new applications in green technology.

Why China Controls the Rare Earths Game

China’s grip on rare earth production extends far beyond mining percentages. The International Energy Agency reports that China controls approximately 60 percent of global mined magnet rare earth production, over 90 percent of refining capacity, and roughly 95 percent of permanent magnet production. This concentration matters because refining and magnet manufacturing represent the true bottlenecks, not raw ore extraction. A nation can mine rare earth ore elsewhere, but without access to Chinese refining infrastructure or magnet production facilities, that ore becomes economically worthless. China weaponized this reality in 2025 when export controls on rare earth materials caused immediate input shortages and reduced production for manufacturers outside China. Fully implemented export controls could jeopardize up to 6.5 trillion dollars of annual economic activity globally, particularly in automotive, electronics, and transport sectors, according to the IEA. This threat materialized last year and manufacturers scrambled to secure alternative supply sources that simply don’t exist at scale.

Refining and Magnet Manufacturing Form the Real Chokepoint

The supply picture outside China deteriorates dramatically as production scales downward. Mining capacity outside China will cover approximately 50 percent of demand by 2035, refining capacity only 25 percent, and magnet manufacturing less than 20 percent. This cascading deficit means that even if new mines open in North America, Africa, or Southeast Asia, those projects cannot reach commercial viability without access to Chinese refining services or magnet makers. The IEA estimates that 60 billion dollars of investment over the next decade is necessary to develop diversified rare earth supply chains that reduce this dependency.

Progress toward diversification remains limited; existing and planned projects fall far short of meeting projected demand growth of more than 30 percent by 2030.

Strategic Stockpiling Addresses Symptoms, Not Root Causes

Governments stockpile rare earth materials to address immediate supply crises, yet this approach cannot substitute for permanent supply chain transformation. Strategic reserves provide temporary relief during export restrictions or market disruptions, but they deplete over time and require constant replenishment. The real opportunity for investors lies in backing projects that solve downstream bottlenecks-refining capacity and magnet manufacturing facilities-rather than mining operations that feed into Chinese refineries. Projects that establish processing infrastructure outside China create lasting competitive advantages and reduce geopolitical exposure for downstream manufacturers. These downstream investments command premium valuations because they address the actual constraint limiting market growth.

Where Investment Opportunities Concentrate

The investment thesis shifts when you recognize that mining alone cannot solve the supply problem. Investors should focus on companies developing refining technology, magnet manufacturing capacity, and recycling infrastructure that operates independently from Chinese supply chains. These projects face higher capital requirements and longer development timelines than mining operations, but they offer substantially greater strategic value. Companies that can process rare earth ore into refined materials or manufacture magnets domestically position themselves as essential infrastructure for the energy transition and defense applications. The next phase of rare earths market development depends entirely on whether these downstream projects can scale fast enough to meet accelerating demand from electric vehicles and renewable energy installations.

Where Technology and Recycling Reshape Supply Economics

Electric vehicles and renewable energy installations push rare earth demand upward with relentless force, yet this surge masks a fundamental reality: demand growth alone cannot solve supply constraints without parallel advances in recycling and processing technology. The IEA projects that magnet rare earth demand will exceed 30 percent growth by 2030, with electric vehicles and wind turbines consuming the majority of neodymium and praseodymium globally. This demand acceleration creates immediate pressure on mining and refining capacity, but recycling offers a tangible path to reduce primary supply needs. The IEA estimates that recycling could diminish primary rare earth supply requirements up to 35 percent by 2050, a substantial reduction that fundamentally alters project economics for investors.

Processing Innovation Unlocks Hidden Value

Critical Metals Corp demonstrated this opportunity through metallurgical testing in 2025, replicating prior results and achieving approximately 40 percent improved refined concentrate yields plus better total rare earth element recovery through new processing technology. This improvement matters because enhanced recovery rates directly translate to lower per-unit production costs and faster payback periods for capital-intensive projects. Investors should monitor recycling initiatives and processing innovations closely because these technologies determine whether existing rare earth deposits can compete economically against Chinese production costs without permanent tariff protection. The cost advantage compounds when processing technology reduces waste and increases the percentage of ore that converts to saleable product.

Domestic Magnet Production Reaches Commercial Scale

Domestic magnet production capacity finally reaches commercial scale, fundamentally shifting where manufacturers source high-strength magnets for electric vehicles and defense applications. USA Rare Earth began commercial sintered neodymium-iron-boron magnet production in Stillwater, Oklahoma during the second quarter of 2026, marking the first sustained domestic magnet output in decades. MP Materials’ 10X campus in Northlake, Texas represents the next inflection point, targeting 10,000 metric tons annually by 2028 with over 1.25 billion dollars invested and more than 1,500 jobs created. These facilities eliminate reliance on Chinese magnet supply for critical applications, but they require consistent feedstock from upstream processing operations to maintain profitability.

Feedstock Certainty Justifies Upstream Investment

Magnet manufacturers now function as anchor customers for rare earth refiners, creating stable demand that justifies investment in new refining capacity outside China. This downstream demand certainty accelerates the development timeline for projects like Apex Critical Metals’ Rift deposit, where neodymium-praseodymium enrichment averaging 49 percent over 10 meters substantially improves project value (producing higher-grade concentrate that commands premium pricing from magnet makers). Investors should recognize that magnet production facilities anchor the entire supply chain, transforming what was previously a speculative mining sector into a utility-like business with contracted offtake agreements. The premium pricing that magnet makers pay for enriched concentrate directly funds exploration and development at upstream mining operations, creating a virtuous cycle that accelerates supply chain diversification outside China.

Final Thoughts

The rare earths market outlook hinges on whether supply chain diversification outside China accelerates fast enough to meet surging demand from electric vehicles and renewable energy. Magnet rare earth demand will grow over 30 percent by 2030, yet refining capacity outside China will cover only 25 percent of needs and magnet manufacturing less than 20 percent by 2035. This widening gap creates both risk and opportunity for investors willing to back projects that solve downstream bottlenecks rather than chase mining operations feeding into Chinese refineries.

Magnet manufacturers now function as anchor customers for rare earth refiners, which strengthens the investment case considerably. USA Rare Earth’s commercial production in Oklahoma and MP Materials’ 10X campus in Texas represent the first genuine steps toward supply chain independence, and these facilities require consistent feedstock that justifies upstream investment in projects like Apex Critical Metals’ Rift deposit (where neodymium-praseodymium enrichment substantially improves economics). Processing innovations demonstrated by Critical Metals Corp, which achieved 40 percent improved refined concentrate yields, prove that technology can reduce production costs and accelerate payback periods.

Recycling offers additional upside that most investors underestimate, as the IEA estimates recycling could reduce primary rare earth supply needs by 35 percent by 2050. Combined with domestic magnet production reaching commercial scale, this creates a structural shift away from Chinese dependency that will persist for decades. We at Natural Resource Stocks provide expert analysis and market insights to help you identify which projects will drive this supply chain revolution and capture the premium valuations that accompany genuine supply chain solutions.