Platinum prices are climbing, and the reasons are clear. Industrial demand from automotive and hydrogen fuel cell sectors is accelerating, while supply constraints in South Africa and Russian sanctions are tightening the market.

At Natural Resource Stocks, we’re tracking these platinum market trends closely because they’re creating real opportunities for investors. Understanding what’s driving the white metal now will help you position yourself ahead of the next wave.

Where Platinum Demand Is Really Coming From

Automotive Catalytic Converters: The Structural Foundation

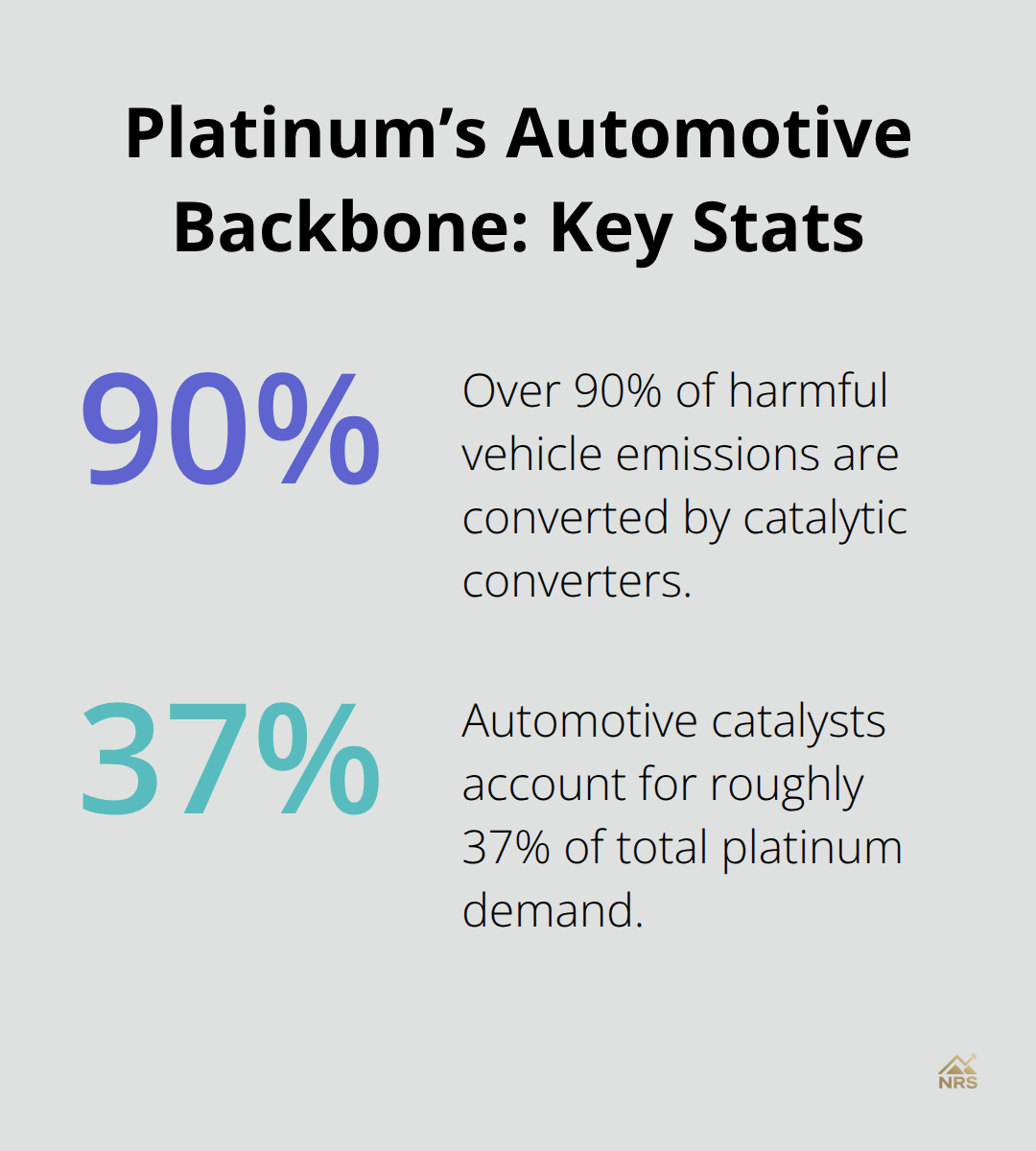

Automotive catalytic converters remain platinum’s backbone, converting over 90% of harmful vehicle emissions according to research from Mordor Intelligence. This demand won’t disappear. Stricter emissions standards in the US, Europe, and China tighten requirements rather than loosen them. The EU’s 2035 combustion-engine ban decision in 2025 accelerated demand for platinum-based catalytic converters in vehicles manufacturers must sell before that deadline.

China’s 6 emission standards for heavy-duty diesel vehicles similarly locked in platinum demand for commercial fleets. Automotive catalysts account for roughly 37% of total platinum demand, and this segment operates structurally rather than cyclically. When vehicles roll off assembly lines, they require catalytic converters. The real opportunity lies in recognizing that stricter regulations guarantee baseline demand regardless of economic conditions.

Chemical Catalysts and Industrial Processing

Chemical catalysts represent the second major industrial pillar, accounting for roughly 40% of total industrial platinum usage across petroleum refining and chemical production. Refineries depend on platinum catalysts to process crude oil efficiently, and the chemical industry applies platinum in everything from fertilizer production to fine chemical synthesis. Unlike automotive demand, chemical catalyst demand remains price-inelastic-refineries and chemical plants won’t switch to inferior catalysts simply because platinum prices rise. These industrial processes operate continuously, and manufacturers cannot compromise on catalyst quality without sacrificing output or efficiency.

Emerging Growth Segments

Glass production emerges as the fastest-growing non-jewelry segment, projected to expand about 5.72% annually through 2031 according to Mordor Intelligence. Platinum enables high-temperature, erosion-resistant components for LCD and plasma displays, plus solar glass manufacturing. Electronics applications including magnetic coatings for computer hard drives continue to consume material quantities of platinum. These sectors expand as technology adoption accelerates globally, particularly in Asia-Pacific markets where display and electronics manufacturing concentrates.

Hydrogen Fuel Cells: The Structural Growth Story

The hydrogen fuel cell sector remains smaller today but represents genuine structural growth. Platinum catalysts convert hydrogen into electricity efficiently, making them essential to fuel cell technology. While hydrogen adoption faces infrastructure challenges, major automakers and governments continue investing in fuel cell development. This demand trajectory differs from cyclical industrial sectors-it reflects long-term policy commitments and technological transitions that will unfold over the next decade.

Supply constraints amplify the power of this embedded demand across all applications. Platinum demand isn’t speculative; it’s woven into production processes that operate regardless of market sentiment. These structural demand drivers set the stage for understanding why supply-side pressures matter so intensely for platinum prices.

Why South Africa’s Platinum Mines Can’t Keep Up

The Dominance Problem

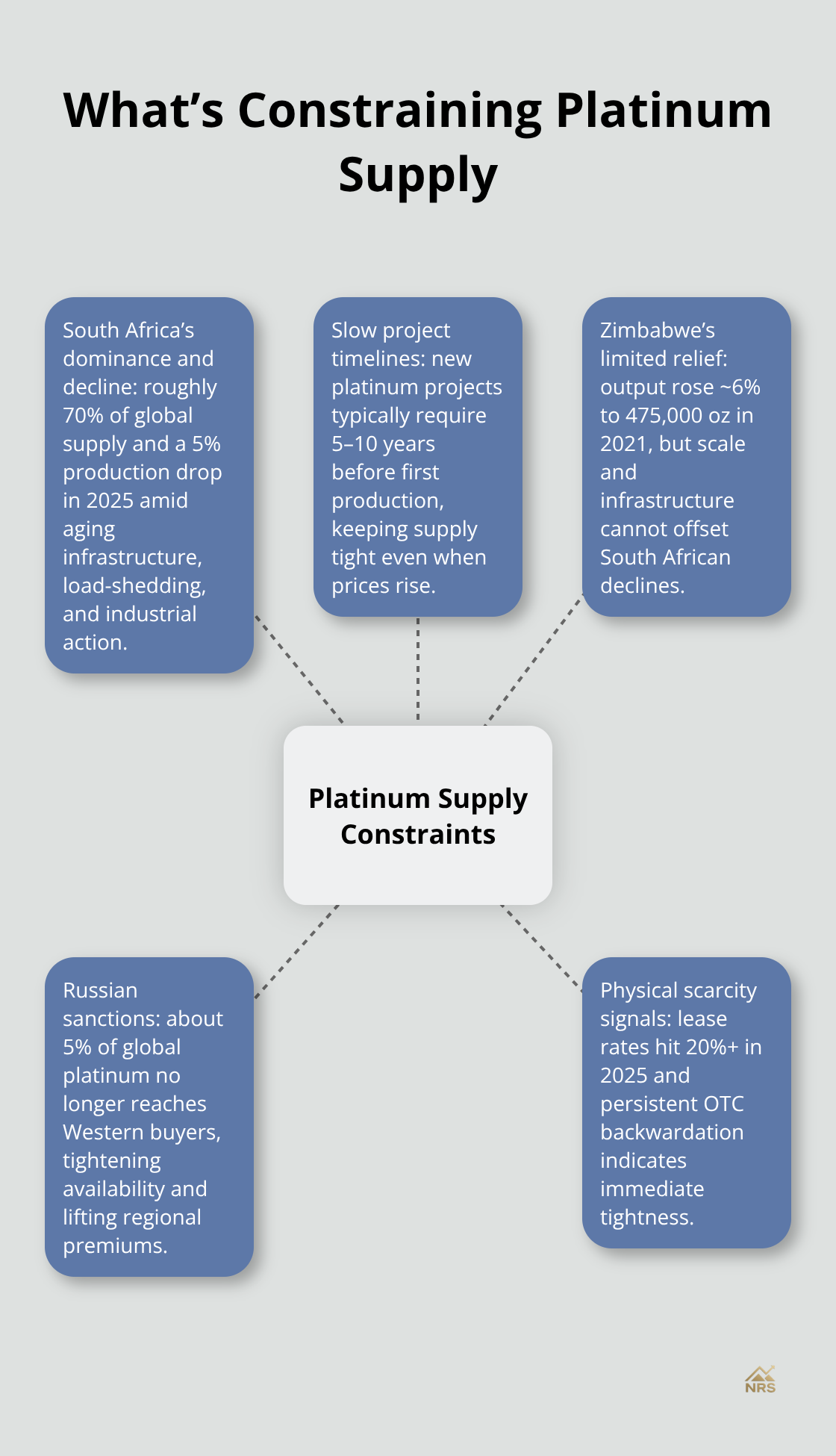

South Africa controls roughly 70% of global platinum supply, making the region’s mining challenges a direct threat to worldwide market balance. The World Platinum Investment Council reports that South African mine production declined 5% in 2025, with deeper cuts ahead due to aging infrastructure, load-shedding, and industrial action. The country’s largest mines-Anglo American Platinum, Impala Platinum, and Sibanye-Stillwater-face crushing electricity costs as South Africa’s state utility Eskom struggles to meet demand.

Why Supply Can’t Respond Quickly

A single mine shutdown cascades through global markets because no other region can absorb the lost production quickly. Zimbabwe offers modest relief, with output rising roughly 6% to 475,000 ounces in 2021, but Zimbabwe’s mining sector lacks the scale and infrastructure to replace South African declines. New platinum projects require five to ten years of development before production begins, meaning today’s supply tightness will persist regardless of investment decisions made now.

The World Platinum Investment Council projects total platinum supply will rise only 4% year-over-year in 2026, while deficits persist at roughly 692,000 ounces annually through 2025. Above-ground stocks have collapsed 42% since 2020 to approximately 2,341,000 ounces, leaving less than five months of demand cover-a critically low buffer that amplifies price volatility.

Russian Sanctions Remove Another Major Source

Russian sanctions eliminate another major supply source from Western markets. Russia produced roughly 5% of global platinum before export restrictions took effect, and that metal no longer flows to North American or European buyers. This supply loss tightens physical availability in Western markets specifically, creating regional price premiums and forcing industrial users to compete harder for limited stocks.

Physical Scarcity Signals Extreme Tightness

Platinum lease rates hit 20%+ in 2025, signaling extreme scarcity of physical metal available to borrow. Leasing volumes decline as metal holders refuse to lend, withdrawing platinum from lending markets entirely. The London over-the-counter market shows persistent backwardation-a pricing structure indicating immediate scarcity outweighs future supply expectations.

For investors, this tightness means platinum supply cannot respond to price signals in any meaningful timeframe. Higher prices won’t unlock new South African production quickly, and sanctioned Russian metal remains unavailable to most Western markets. This structural mismatch between inelastic supply and ongoing industrial demand creates conditions where investors must evaluate how supply constraints will shape platinum’s investment profile across different market scenarios and time horizons.

How to Position Yourself in Platinum’s Supply Crisis

The supply constraints we outlined create a direct investment thesis: platinum will remain scarce, and investors who position now will benefit from sustained price pressure. The question isn’t whether platinum prices stay elevated, but how to gain exposure most efficiently. Mining stocks and ETFs offer distinct paths into this market, each with different risk profiles and entry points worth evaluating carefully.

Mining Companies: Direct Exposure With Operational Risk

Platinum mining companies operating at scale represent the most direct exposure to supply tightness. Anglo American Platinum, Impala Platinum, and Sibanye-Stillwater control the majority of global production and face rising costs from electricity shortages and labor pressures in South Africa. These companies benefit structurally from platinum scarcity because they cannot increase output meaningfully despite higher prices, meaning margin expansion flows directly to shareholders.

The challenge is execution risk: South African operational disruptions remain a real threat, and electricity costs could worsen. Sibanye-Stillwater’s 2025 output faced pressure from load-shedding, yet the company maintained profitability because platinum prices offset rising costs. This dynamic persists into 2026 if supply remains constrained.

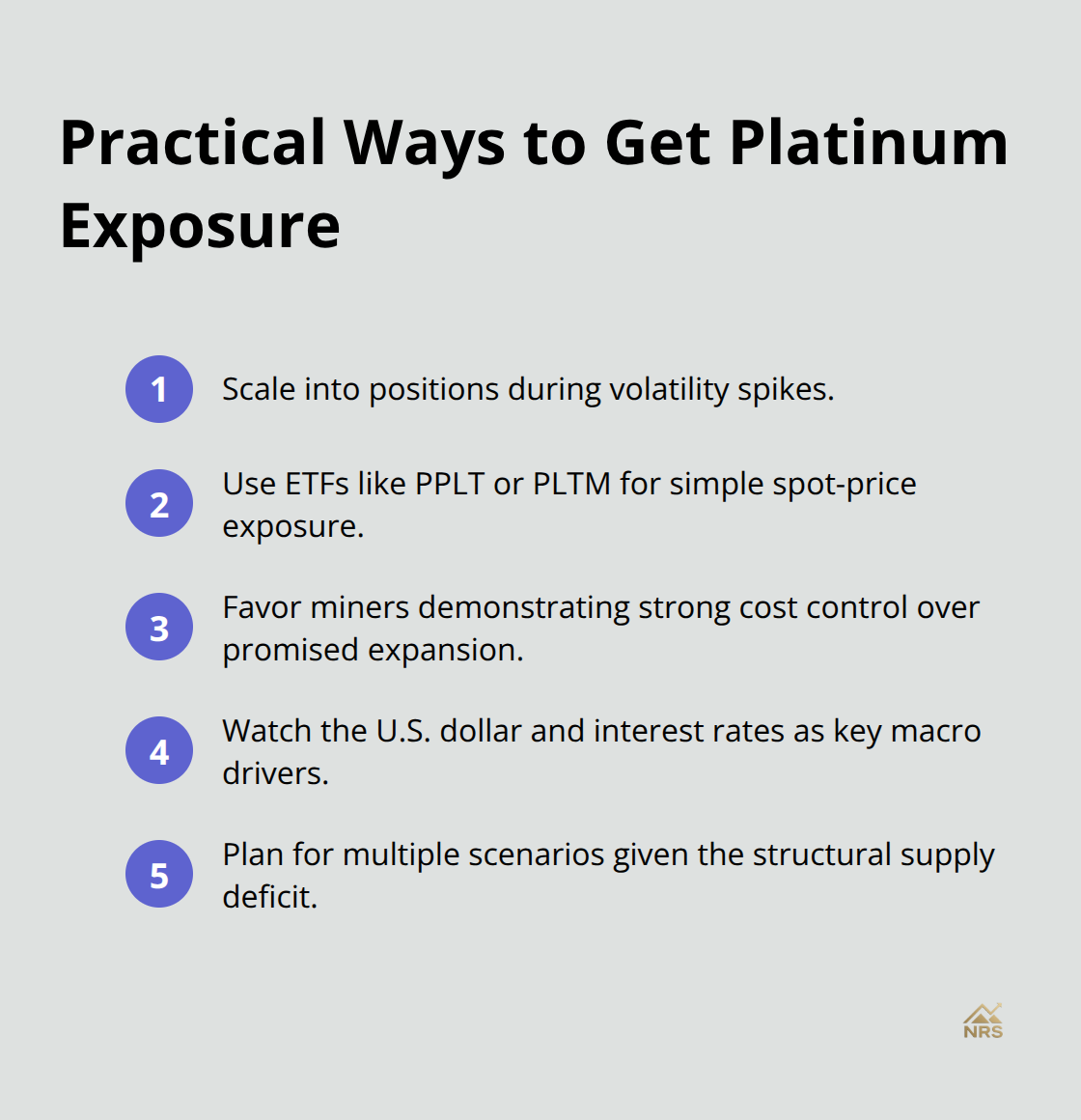

For investors seeking direct mining exposure, focus on companies demonstrating cost control in challenging environments rather than betting on production growth that won’t materialize. Production trends matter more than expansion promises when evaluating mining stocks in this environment.

ETFs: Simplicity and Spot-Price Exposure

ETFs offer a different approach entirely, and they work well for most investors seeking platinum exposure. PPLT and PLTM track platinum spot prices directly, providing efficient exposure without mining company operational risk. These funds hold physical platinum or futures contracts, eliminating counterparty risk and complexity.

PPLT specifically holds physical platinum bars in vaults, making it the purest spot-price play available. Expense ratios remain low, typically under 0.60% annually.

The advantage is simplicity: you gain platinum exposure without analyzing mining company balance sheets or geopolitical risks in South Africa. ETF investors benefit from supply tightness regardless of which mining company faces disruption.

Strategic Entry Points in a Volatile Market

Entry points matter significantly right now. Platinum prices began 2026 with strength, continuing the 2025 breakout where the metal delivered returns exceeding 125%. Above-ground stocks stand at their lowest levels in years. Price volatility will persist as investors rotate between risk assets and safe havens based on geopolitical developments.

Dollar weakness and easing interest rates supported platinum in 2025, and these factors remain fluid. Try scaling into platinum positions during volatility spikes when fear drives selling, rather than attempting to time a single entry point. The structural supply deficit averaging roughly 692,000 ounces annually means scarcity compounds over time, supporting a multi-year platinum investment thesis regardless of short-term price movements.

The World Platinum Investment Council projects a small market surplus of roughly 20,000 ounces in 2026, contingent on easing US-China trade tensions. If tensions persist, deficits extend further, supporting sustained platinum prices. This conditional outlook reinforces why investors should position for multiple scenarios rather than betting on a single outcome.

Final Thoughts

Platinum market trends point toward sustained scarcity and structural demand that will shape investment returns over the next several years. The white metal’s price surge in 2025 reflected real supply constraints meeting genuine industrial demand across automotive, chemical, and emerging hydrogen sectors. Automotive catalytic converters alone guarantee baseline platinum consumption regardless of economic cycles, while chemical catalysts and glass production add layers of inelastic demand that won’t disappear when prices rise.

Supply remains the binding constraint that will persist through 2026 and beyond. South Africa’s production decline, Russian sanctions, and the impossibility of rapid mining expansion mean platinum deficits continue across the forecast horizon. Above-ground stocks have collapsed to critically low levels, leaving minimal buffer against supply disruptions, and this structural undersupply creates a multi-year tailwind for platinum prices that transcends short-term market sentiment. Risk factors including South African operational disruptions, electricity cost pressures, and geopolitical tensions could shift outcomes unexpectedly, though the price-inelastic nature of most platinum applications limits downside risk significantly.

For investors, platinum will likely trade higher over the next three to five years as supply tightness persists and industrial demand continues. Mining stocks offer direct exposure with operational risk, while ETFs provide simplicity and spot-price tracking-try scaling into positions during volatility rather than chasing strength. We at Natural Resource Stocks track platinum market trends and broader natural resource opportunities through expert analysis and macroeconomic insights, so visit our platform to access in-depth market commentary and position yourself strategically across resource sectors.