Nuclear energy is experiencing a genuine resurgence. Governments worldwide are committing billions to reactor construction, and the uranium demand outlook for 2027 shows supply struggling to keep pace with growth.

At Natural Resource Stocks, we’ve identified this mismatch as a defining opportunity for investors. The coming years will separate winners from laggards in the uranium sector.

How Fast Is Nuclear Really Expanding

Asia-Pacific Leads Global Reactor Growth

China operates over 20 reactors and has 29 more under construction, with plans to reach 30 percent of electricity generation from nuclear by 2050. The country produced 242.2 terawatt-hours of nuclear electricity in its fiscal year, demonstrating industrial-scale deployment that Western competitors struggle to match. Japan restarted reactors after Fukushima, with 14 reactors producing 93.48 terawatt-hours in fiscal 2024, and targets 20 percent nuclear electricity by 2040. South Korea operates above 80 percent capacity utilization across its fleet. These numbers matter because Asia-Pacific held 33.7 percent of global uranium enrichment market share in 2024 and maintains a projected 9.9 percent annual growth rate through 2030. This regional concentration reveals where uranium demand actually concentrates, not in theoretical projections but in operating reactors and active construction pipelines.

The U.S. Supply Gap and Government Response

The United States faces a uranium supply gap of approximately 184 million pounds through 2030, per Bloomberg reporting from November 2025. This gap exists because utilities under-contract for uranium despite known demand. The U.S. Department of Energy awarded 3.4 billion dollars in long-term contracts to domestic enrichment producers, signaling government recognition that current market forces alone cannot close the supply gap. Western enrichment capacity sits at roughly 25,300 tSWU annually, insufficient for regional reactor fleets, and expansions typically require five to seven years.

Europe’s Fuel Diversification Challenge

Europe phases out Russian nuclear fuel entirely through the REPowerEU Roadmap. The EU imported over 13,000 metric tons of natural uranium in 2024, with Russia supplying 15 percent of that volume. This geopolitical shift forces European utilities to secure alternative suppliers and invest in domestic enrichment capacity-a transition that takes years to complete.

Small Modular Reactors Drive New Fuel Demand

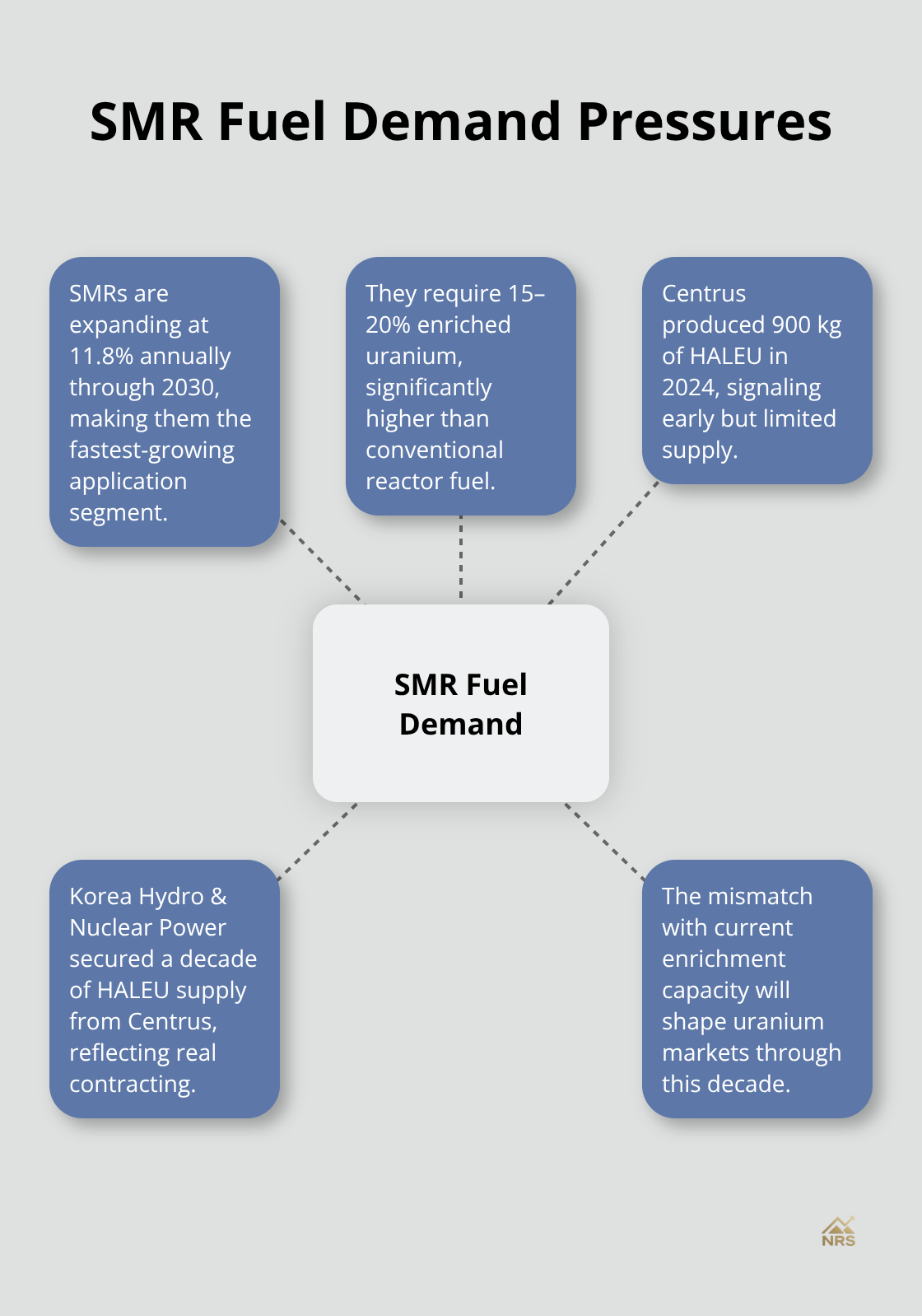

Small modular reactors represent the fastest-growing application segment, expanding at 11.8 percent annually through 2030, yet they demand 15 to 20 percent enriched uranium. This creates a separate supply crunch beyond conventional reactor fuel needs. Centrus produced 900 kilograms of this high-assay low-enriched uranium in 2024, while Korea Hydro & Nuclear Power secured a decade of supply from Centrus. These are not aspirational targets; they reflect current contracting realities showing where actual fuel demand pressure exists.

The mismatch between SMR fuel requirements and current enrichment capacity will shape uranium markets through the remainder of this decade and beyond.

Where Uranium Actually Gets Produced

Kazakhstan dominates global uranium production with roughly 38 percent of world output, followed by Canada at 24 percent. Australia, Namibia, and Russia round out the top five producers. This geographic concentration matters because Kazakhstan’s political orientation toward strategic autonomy from Russia and China creates potential openings for Western supply diversification.

The United States mines virtually no uranium domestically, a vulnerability that the Department of Energy now treats as a national security issue. Global uranium production growth barely matches rising reactor demand, with projections showing U.S. uranium production could increase to more than 4 million lb U3O8 annually by 2030.

The Conversion Bottleneck

The conversion stage represents the actual constraint on supply expansion. Western conversion capacity sits at approximately 31,100 tonnes of uranium annually, yet the region faces a shortfall exceeding 10,000 tonnes per year. Only about five large-scale conversion facilities operate globally, and stockpiles are shrinking. Buyers hesitate to sign long-term conversion contracts at current high prices, which means conversion capacity will not expand without government intervention or sustained price premiums that make new projects economically viable.

Geopolitical Pressure Reshapes Supply Routes

Russia supplied 23 percent of European enrichment needs in 2024, down from 38 percent in 2023, while the United States increased its share by 18 percent. The European Commission’s REPowerEU Roadmap targets complete phaseout of Russian nuclear fuel, including enriched uranium imports and future fuel contracts. This transition creates a five-to-seven-year implementation lag because enrichment capacity expansions require years to complete. Planned capacity additions in France, Germany, the Netherlands, the UK, and the US target post-2027 completion dates.

HALEU Supply Risk and Western Response

High-assay low-enriched uranium for small modular reactors presents another supply risk. EU HALEU imports currently split roughly 50-50 between the US and Russia, with higher enrichment prices potentially constraining faster reactor deployment. Western governments recognize these constraints and act accordingly. The DOE awarded 2.7 billion dollars in enrichment contracts to three domestic companies, explicitly targeting both conventional and next-generation reactor fuel. These are not theoretical policy gestures but concrete capital commitments to build capacity that will operate for decades. The investment decisions made today will determine whether Western nations can meet their nuclear expansion targets or face fuel shortages that slow reactor deployment through the 2030s.

Where Uranium Investment Opportunity Concentrates

The supply deficits outlined above create genuine investment opportunities, but not all uranium plays offer equal risk-adjusted returns. Uranium spot prices traded near $86 per pound in May 2026, signaling renewed contracting interest that translates directly into producer cash flows. The fundamental driver remains unchanged: Western nations cannot meet their nuclear targets without securing reliable uranium supply, and current production capacity cannot support that demand through 2030 and beyond.

Production Capability Trumps Exploration Potential

This reality favors producers with near-term production capability and long-term contracts already in place over explorers betting on future discoveries. Established producers controlling operating mines or advanced development projects benefit immediately from price strength and multi-year offtake agreements. NexGen Energy’s Rook I project carries a capital expenditure estimate of CAD 2.2 billion and targets production within the decade, positioning the company to capture demand growth as Western enrichment constraints force utilities to secure supply now rather than later. Smaller producers with existing production or advanced projects closer to development outperform junior explorers still in early-stage work because they convert current market strength into revenue and cash generation while the supply gap persists through 2027 and 2028.

Geographic Diversification Reduces Geopolitical Risk

Kazakhstan supplies 39 percent of global uranium output, yet Western governments actively reduce reliance on that concentration. Producers operating in Canada, Australia, and Namibia benefit from increased procurement attention as utilities and governments diversify supply sources away from geopolitical risk. Orano’s partnership with Uzbekistan’s Navoiyuran joint venture targets approximately 700 tonnes of uranium annually through the Nurlikum Mining project, exemplifying how Western producers expand capacity outside traditional supply centers. For investors, this means favoring producers with assets in jurisdictions where Western governments actively support supply chain security.

Contract Revenue Outweighs Spot Market Exposure

Natural resource portfolios gain meaningful diversification through uranium producers because uranium demand tracks nuclear policy and energy security rather than traditional economic cycles. Utilities sign multi-year contracts regardless of broader economic conditions, creating revenue stability that differs sharply from cyclical commodity exposure. Investors should prioritize producers with executed or near-term contracts over those relying on spot market sales, since contracted revenue provides certainty that persists even if uranium prices moderate from current levels (a scenario that remains unlikely given Western supply constraints through 2030).

Final Thoughts

The uranium demand outlook through 2027 reflects a fundamental mismatch between Western nuclear ambitions and current fuel supply capacity. Asia-Pacific reactor growth, U.S. supply gaps exceeding 184 million pounds, and Europe’s geopolitical pivot away from Russian fuel create a supply environment where demand will outpace production for years. This is not speculation-utility contracting patterns, government capital commitments, and the five-to-seven-year timelines required to expand conversion and enrichment facilities confirm it.

Established producers with near-term production capability and executed contracts will capture disproportionate value as utilities secure supply now rather than risk shortages later. Geographic diversification away from Kazakhstan concentration benefits producers in Canada, Australia, and Namibia as Western governments actively support supply chain security. Contract revenue provides stability that spot market exposure cannot match, making multi-year offtake agreements the defining metric for producer quality.

Investors positioning for the nuclear energy transition should focus on producers converting current market strength into cash generation rather than explorers betting on future discoveries. The supply constraints are real, the government support is concrete, and the timeline is compressed. We at Natural Resource Stocks provide the market analysis and expert insights needed to identify which uranium producers will thrive as Western nations execute their nuclear expansion plans-explore our uranium investment research to discover how uranium exposure fits your natural resource portfolio strategy.