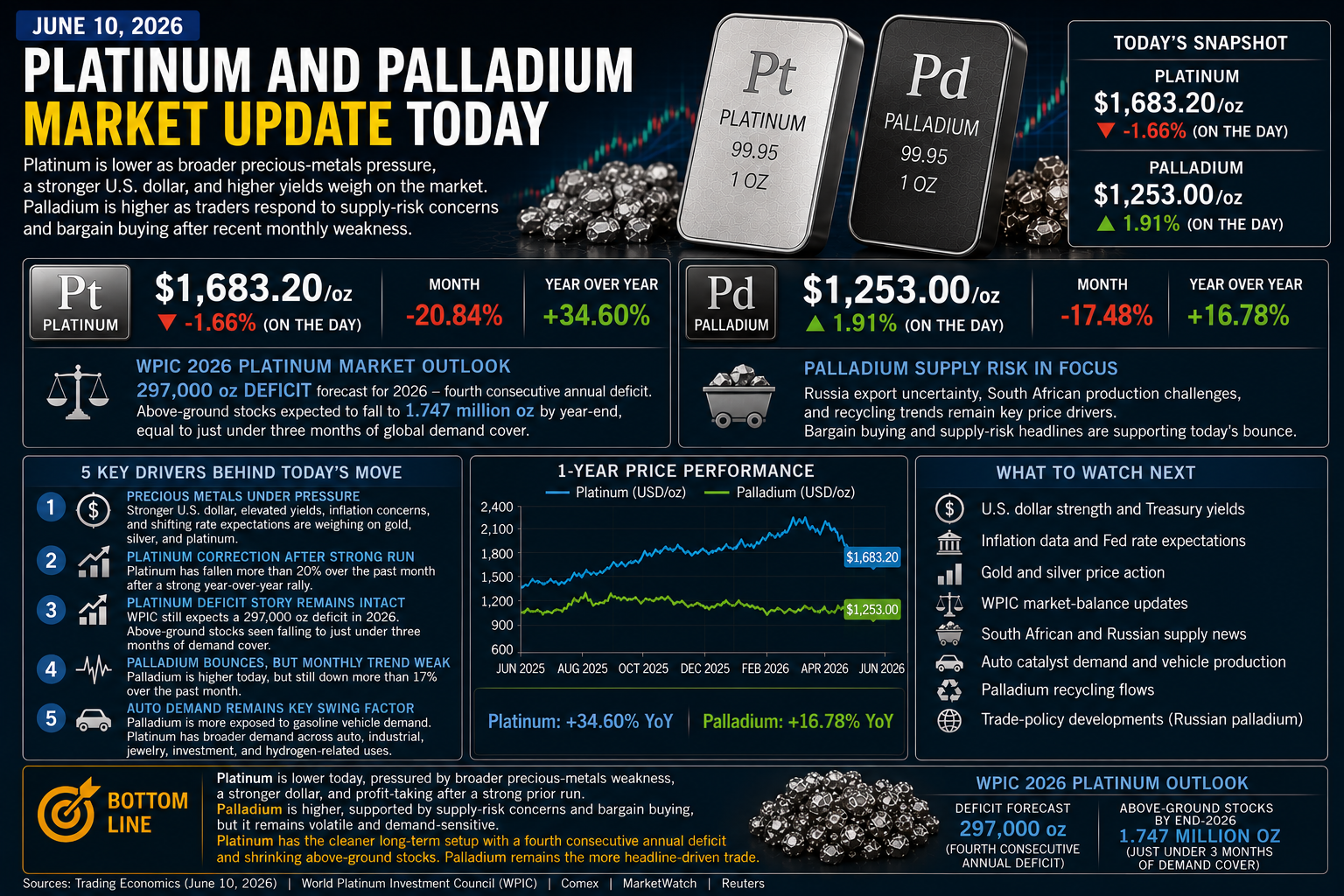

Platinum and palladium are nearly flat today, but the broader setup is still important. Platinum is easing slightly after a strong year-over-year run, while palladium is holding modestly higher despite recent monthly weakness. The main difference remains the same: platinum has the cleaner structural deficit story, while palladium is more tied to Russia supply risk, auto demand, recycling flows, and trade-policy headlines.

Today’s pricing snapshot

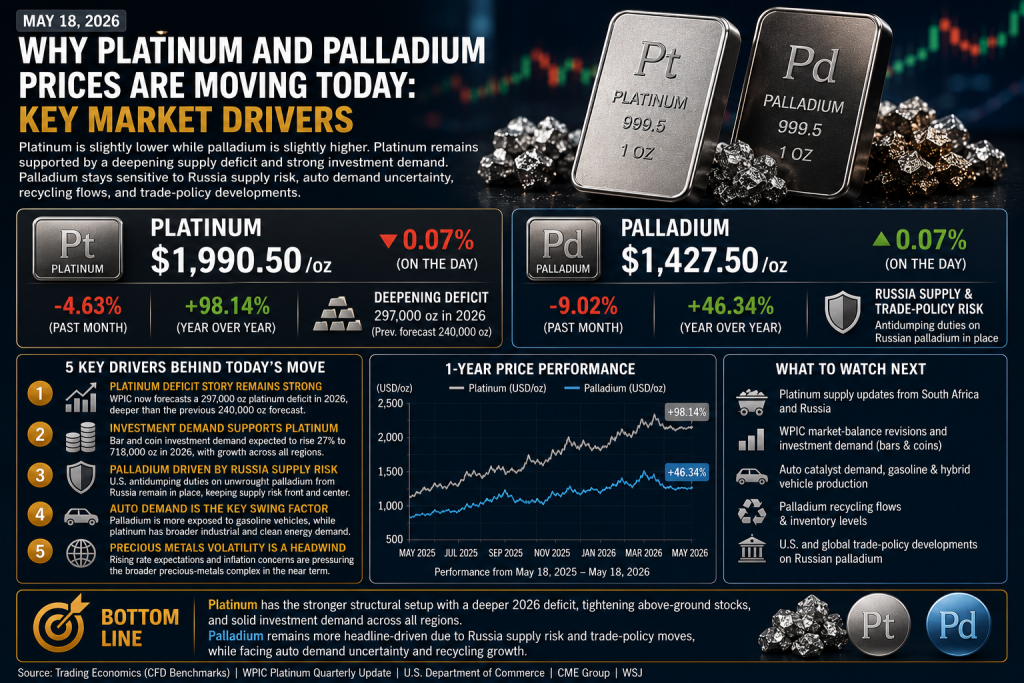

According to Trading Economics CFD benchmarks, platinum fell to about $1,990.50/oz on May 18, 2026, down roughly 0.07% on the day. Platinum is down about 4.63% over the past month, but it remains up roughly 98.14% year over year, showing that the metal is still holding major gains despite today’s softness.

Palladium rose to about $1,427.50/oz on May 18, 2026, up roughly 0.07% on the day. Palladium is down about 9.02% over the past month, but it remains up roughly 46.34% year over year, keeping supply-risk concerns in focus even after a recent pullback.

5 key drivers behind today’s move

1) Platinum is pausing, but the deficit story remains strong

Platinum’s small decline today looks more like consolidation than a breakdown. The latest World Platinum Investment Council update says the forecast for a fourth straight platinum market deficit in 2026 has deepened to 297,000 ounces, compared with the previous forecast of 240,000 ounces. WPIC also expects above-ground stocks to fall to just under three months of demand cover by the end of 2026.

That tight physical backdrop continues to support platinum even when prices cool in the short term.

2) Investment demand remains a major platinum support

Investor demand is still one of platinum’s biggest supports. WPIC now expects total bar and coin investment demand to rise 27% to 718,000 ounces in 2026, helped by a strong first quarter and growth across all regions.

That matters because investment demand can tighten available supply faster when the market is already running in deficit.

3) Palladium is holding up on Russia supply and trade-policy risk

Palladium remains sensitive to Russian supply headlines. The U.S. Department of Commerce announced a final affirmative determination in the antidumping duty investigation of unwrought palladium from Russia on April 28, 2026, and the Federal Register notice said Commerce determined that Russian palladium was being, or was likely to be, sold in the U.S. at less than fair value.

That keeps palladium headline-driven, especially because any shift in duties, import flows, sanctions, or Russian export availability can quickly affect sentiment.

4) Auto demand remains the key swing factor

Both platinum and palladium are used in catalytic converters, but palladium remains more exposed to gasoline vehicle demand. Platinum has a broader demand base across auto catalysts, jewelry, industrial applications, investment products, and fuel-cell-related clean-energy uses. CME notes that platinum demand extends beyond jewelry and industrial applications into catalytic converters and fuel cells, while palladium is widely used in automotive catalytic converters, electronics, dental, and chemical applications.

If gasoline and hybrid vehicle production remains strong, palladium can find support. If battery-electric vehicles gain share faster than expected, palladium’s longer-term demand outlook becomes more challenging.

5) Precious-metals volatility is still a headwind

The broader precious-metals complex is under some pressure today. WSJ reported that Comex gold settled slightly lower on May 18, marking a third straight session of declines, as rising interest-rate expectations and inflation concerns weighed on non-yielding assets.

That macro backdrop can limit upside for platinum and palladium in the short term, even when the underlying supply story remains supportive.

What to watch next

Traders will be watching platinum supply updates from South Africa and Russia, WPIC market-balance revisions, bar-and-coin investment demand, auto catalyst demand, palladium recycling flows, gasoline and hybrid vehicle production, and any new U.S. or global trade-policy developments involving Russian palladium.

For platinum, the key question is whether the market keeps pricing in a deeper 2026 deficit and falling above-ground stocks. For palladium, the key question is whether Russia supply risk can offset weaker monthly momentum and uncertainty around auto demand.

Bottom line

On May 18, 2026, platinum is slightly lower while palladium is slightly higher. Platinum still has the stronger structural story because the 2026 deficit forecast has deepened, above-ground stocks are expected to tighten further, and investment demand remains strong. Palladium still has upside potential from Russia supply risk and trade-policy headlines, but it remains more vulnerable to auto-demand shifts, EV adoption, recycling growth, and broader precious-metals volatility.

Platinum looks like the cleaner long-term setup today, while palladium remains the more headline-driven and supply-risk-sensitive trade.