Gold prices swing wildly based on forces most investors don’t fully understand. At Natural Resource Stocks, we’ve identified the main gold price drivers that move markets-from interest rates and geopolitical tensions to mining output and investor demand.

This guide breaks down exactly what moves gold prices and how these factors interact. You’ll learn which signals matter most when building your gold investment strategy.

What Moves Gold Prices in Macroeconomic Cycles

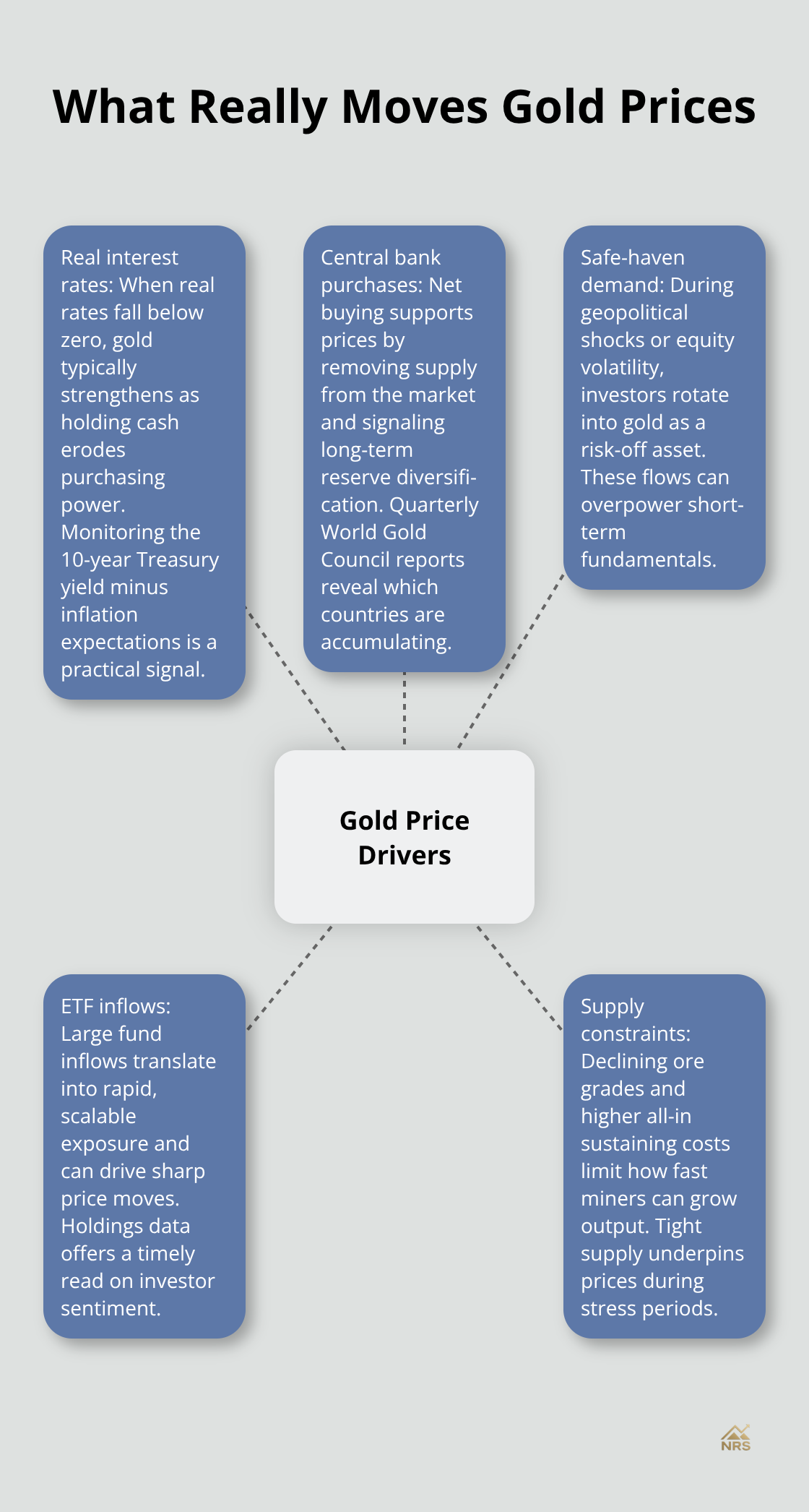

Real Interest Rates: The Primary Driver

Real interest rates sit at the core of gold pricing, and this relationship has hardened over the past two years. When real rates turn negative, gold becomes genuinely attractive because holding cash loses purchasing power. In 2022, inflation exceeded 9% while rates lagged behind, creating negative real returns on bonds and pushing gold higher. The World Gold Council data confirms central banks bought gold with net demand of 230 tonnes in Q4 2025, driven partly by this real-rate environment.

Watch real rates closely: when they fall below zero, gold typically strengthens. Conversely, if the Fed raises rates aggressively above inflation, gold weakens. Try monitoring the 10-year Treasury yield minus inflation expectations, not just the Fed’s headline rate.

Currency Strength: A Weakening Relationship

Currency strength matters far less than most investors assume. Gold and the U.S. dollar both rallied in 2023 and 2024, defying the traditional inverse relationship. Geopolitical tensions in Ukraine and the Middle East drove safe-haven demand for both assets simultaneously, while central banks diversified away from dollar-denominated reserves into gold as a strategic hedge. This structural shift signals that gold’s appeal now stems from systemic risk and inflation protection rather than simple currency weakness.

The dollar’s strength or weakness will influence gold prices, but it no longer acts as the dominant driver it once did. Instead, focus on whether central banks accumulate gold as a strategic reserve.

Economic Growth and Recession Cycles

Economic growth cycles matter only insofar as they affect inflation and real rates. Recession fears in late 2025 and early 2026 pushed gold above $5,500 intraday in January 2026 before pulling back, showing that investors flee to gold when equity returns look uncertain. Rising unemployment or falling manufacturing output typically signal economic weakness, which triggers safe-haven inflows into gold.

The connection is indirect: recessions don’t move gold directly, but the policy responses they trigger-rate cuts and stimulus-do. This means geopolitical events and central bank actions deserve your attention far more than GDP forecasts alone.

Geopolitical Events and Market Sentiment

Central Banks Drive Gold Prices More Than Markets

Central banks hold roughly one-fifth of all gold ever mined, and their purchasing decisions now matter more than traditional supply-demand mechanics. Poland bought 102 tonnes in 2025, Kazakhstan acquired 57 tonnes, and Brazil added 43 tonnes according to the World Gold Council. These transactions reflect a systematic effort to reduce dollar exposure and build gold reserves as a hedge against currency instability and geopolitical risk. China officially reported only 27 tonnes purchased in 2025, yet estimates suggest actual purchases may be substantially higher due to opaque reporting practices. This structural shift toward gold reserves means central bank policy moves gold prices far more reliably than mining output or jewelry demand. When central banks accumulate gold, prices remain supported regardless of short-term market noise. Monitor which countries are buying and at what pace through World Gold Council reports released quarterly.

Safe-Haven Demand Overwhelms Fundamental Analysis

Geopolitical tensions and investor fear drive explosive gold rallies in ways that macroeconomic data alone cannot explain. January 2026 saw gold spike intraday above $5,500 before retreating within days-a 14% swing that reflected shifting risk sentiment rather than fundamental supply changes. The Russia-Ukraine conflict, Middle East instability, and trade uncertainties push investors to rotate into gold as insurance against systemic breakdown. This safe-haven demand operates independently from dollar strength or interest rates.

When equity markets swing sharply downward or political tensions escalate unexpectedly, gold flows accelerate because institutional investors and central banks treat it as the ultimate risk-off asset. Investment demand through ETFs reached 801.2 tonnes in 2025 according to the World Gold Council, demonstrating how quickly capital floods into gold during uncertainty.

Distinguishing Real Threats From Market Noise

Geopolitical headlines matter enormously, but only if they genuinely threaten financial stability. Routine political noise produces minimal gold movement. Focus instead on developments that could disrupt global trade, banking systems, or reserve currency stability. These events trigger the strongest and most sustained gold rallies. The next section examines how physical supply constraints and investor demand patterns interact to shape prices over longer timeframes.

Supply and Demand Imbalances Reshaping Gold Markets

Mining Production Fails to Match Rising Demand

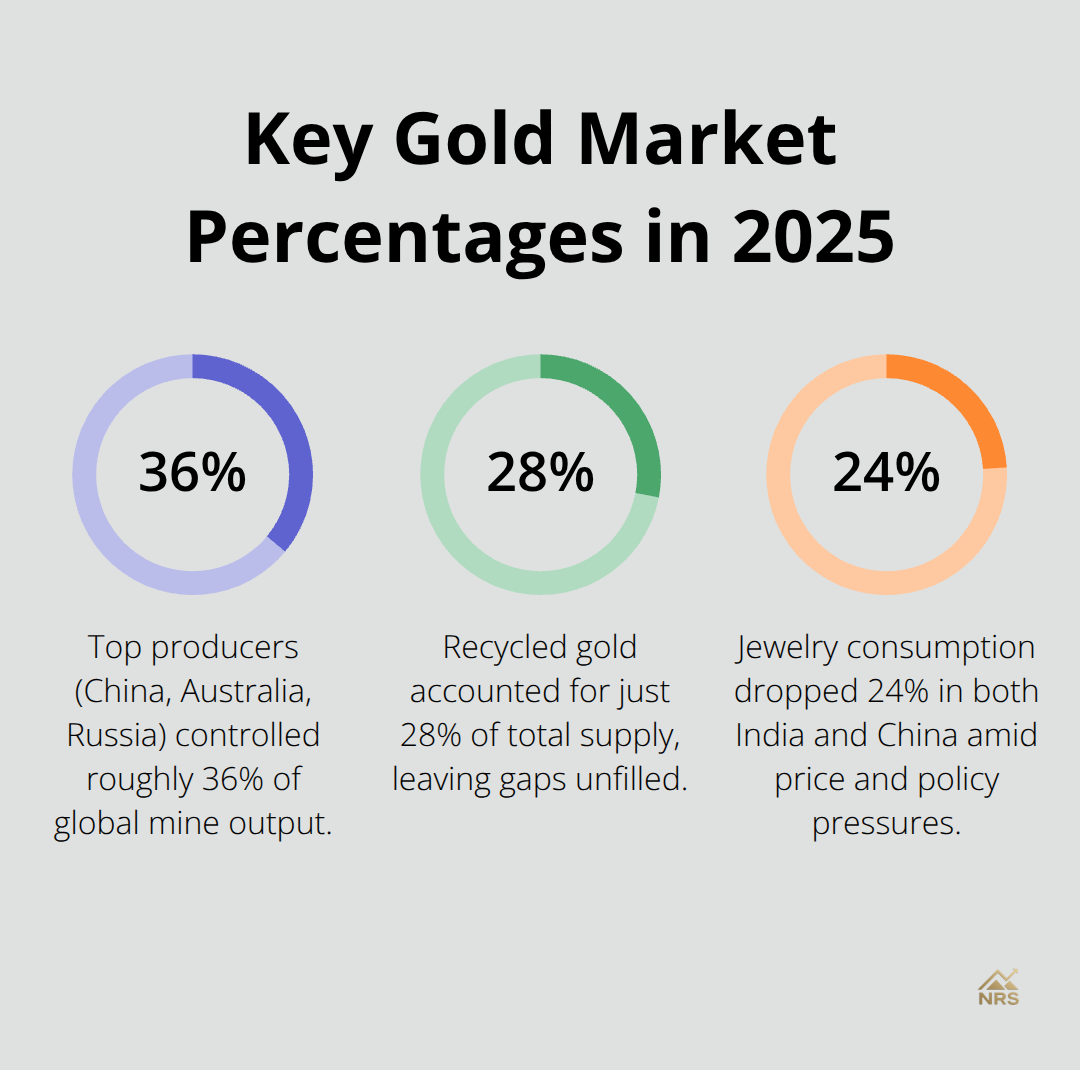

Mining production struggles to keep pace with rising demand, and this matters far more than most investors realize. Global gold output reached 5,002 tonnes in 2025 according to the World Gold Council, yet investment demand alone consumed 2,175 tonnes that year. The problem intensifies because ore grades continue declining across the industry-average grades fell 16% over 15 years from 1.01 grams per tonne to 0.85 grams per tonne, forcing miners to process vastly more rock for the same ounce. All-in sustaining costs surged from roughly $1,000 per ounce in 2020 to $1,600 per ounce by Q3 2025, compressing margins even as gold prices climbed.

This cost inflation means miners cannot simply expand production to meet demand without sacrificing profitability. Top producers like China, Australia, and Russia control roughly 36% of global output, creating concentration risk that leaves markets vulnerable to supply disruptions. Recycled gold provided only 1,404 tonnes in 2025-just 28% of total supply-so secondary sources cannot fill widening gaps.

The structural reality is stark: supply growth has stalled while investment and central bank demand accelerate upward, a mismatch that supports prices over the medium term.

Jewelry Demand Collapses While Investment Flows Accelerate

Jewelry demand collapsed in 2025 while investment flows accelerated, revealing where real gold appetite lies. Jewelry consumption dropped 24% in both India and China despite record gold prices, totaling only 1,374 tonnes globally according to the World Gold Council. India’s decline stemmed partly from rupee weakness and a 74% local price gain that priced out middle-income buyers, while China’s VAT reform on gold fabrication pushed consumers toward ultra-lightweight or ultra-luxury pieces.

Industrial demand rose modestly to 323 tonnes, driven primarily by semiconductor and AI-related electronics that require gold connectors and interconnections. This divergence tells you where institutional capital flows: not toward traditional consumption but toward investment vehicles that offer easy entry and exit.

ETF Inflows and Physical Demand Drive Markets Forward

ETF inflows reached 801.2 tonnes in 2025, channeling $89 billion into gold funds and bringing total ETF holdings to 4,025 tonnes. Physical bars and coins demand held at 1,374 tonnes, with India and China accounting for roughly 53% of this category. These investment vehicles now matter far more than jewelry consumption in price forecasts.

Treat jewelry demand as a declining variable in your analysis. Instead, monitor ETF inflows and central bank accumulation as the true demand drivers that will sustain higher prices regardless of whether wedding season in Delhi produces fewer gold necklaces.

Final Thoughts

Gold price drivers operate through interconnected channels that activate simultaneously during periods of stress. Real interest rates turn negative, central banks accelerate purchases, and equity volatility spikes at the same moment, which intensifies gold rallies because multiple demand sources activate together. The 2025 data confirms this pattern: central banks bought gold strategically while ETF inflows reached 801.2 tonnes and investment demand hit 2,175 tonnes, yet jewelry consumption collapsed. This tells you that traditional demand metrics no longer predict prices accurately.

Supply constraints now create a structural floor under gold prices that protects investors during downturns. Mining production cannot expand fast enough to meet rising demand, with ore grades declining and all-in sustaining costs exceeding $1,600 per ounce. Central bank diversification away from dollar reserves combines with investment-driven demand to support prices at higher levels regardless of short-term market noise.

Focus your strategy on the factors that actually move prices: monitor real interest rate trends, track central bank purchases through quarterly World Gold Council reports, and watch equity market volatility as a leading indicator of safe-haven flows. We at Natural Resource Stocks provide expert analysis on how macroeconomic factors and geopolitical developments shape gold prices and broader commodity markets.