Nuclear power is experiencing a genuine renaissance. Governments worldwide are committing to new reactor builds and life extensions, driving uranium demand to levels not seen in over a decade.

At Natural Resource Stocks, we believe uranium mining stocks offer real value for investors who understand the sector’s fundamentals. This guide walks you through the market dynamics, evaluation criteria, and investment opportunities shaping this space.

Why Uranium Prices Must Rise to Meet Nuclear Demand

The uranium market faces a structural supply deficit that will shape uranium mining stocks for the next decade. According to the International Energy Association’s World Energy Outlook 2025, annual nuclear investment will climb from over 70 billion dollars today to approximately 210 billion dollars by 2035. This capital surge reflects genuine policy momentum, not speculation. The US committed 80 billion dollars to Westinghouse for new reactor construction, while Canada allocated 3 billion Canadian dollars specifically for small modular reactor development. These commitments translate directly into uranium demand.

The IEA forecasts a supply deficit by 2030, meaning mine production will fall short of reactor requirements. This gap exists because new mines require 8 to 12 years to develop and demand enormous upfront capital. Utilities understand this constraint. Long-term uranium contracting volumes reached 82 million pounds year-to-date by December 2025 according to Sprott Asset Management data, yet this remains well below the approximate replacement rate of 150 million pounds annually. The market is tightening, and prices must rise to incentivize producers to build new capacity. Triple-digit long-term uranium pricing represents the minimum threshold needed to unlock sustained upstream growth.

AI and Data Centers Drive Immediate Demand

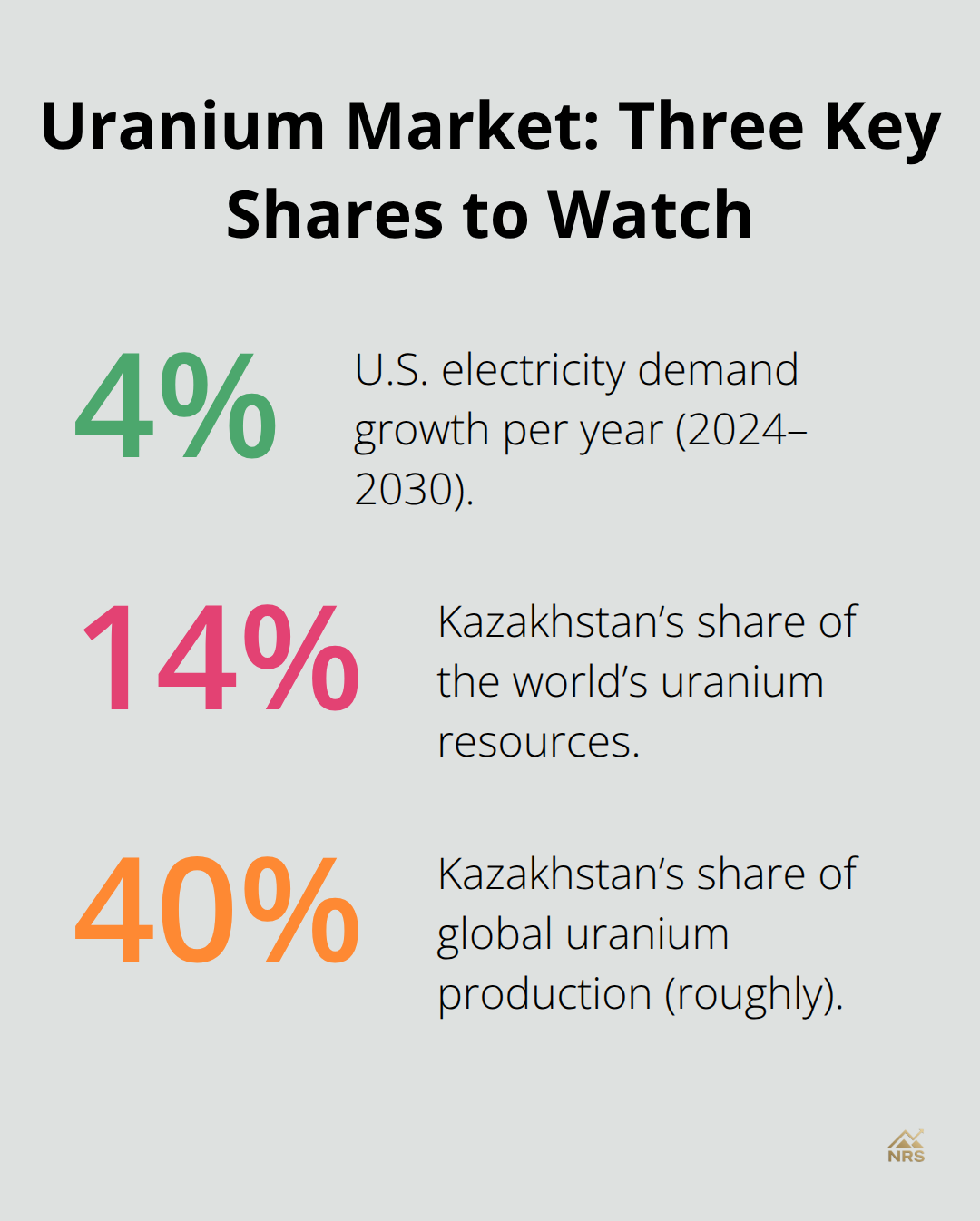

US electricity demand will grow 4 percent annually from 2024 to 2030, but the AI sector’s energy consumption is rising far faster-from 4.3 percent to 11.7 percent of total demand. This shift is not theoretical.

NextEra Energy and Google signed a 25-year power purchase agreement to restart the 615-megawatt Duane Arnold Energy Center around 2029 specifically to serve AI data center loads. Microsoft and Amazon pursue small modular reactors to power their data center infrastructure. These are binding commercial commitments, not sustainability marketing.

Global nuclear capacity would expand to 1446 GWe by 2050 under continued operation and new nuclear build scenarios. This acceleration means uranium miners must expand production capacity immediately, not in five years. Long-term uranium prices reached approximately 86 dollars per pound in 2025 according to Sprott data, up 8.86 percent year-to-date, yet producers like Kazatomprom signaled that even higher prices are required to justify production growth. Uranium mining equities gained 37.98 percent through November 2025, outpacing spot price gains of 3.62 percent, which reveals that investors are pricing in sustained demand and production constraints.

Geopolitical Risk Concentrates Supply Exposure

Kazakhstan, Canada, and Australia control the majority of global uranium production, but geopolitical instability concentrates supply risk in ways uranium investors must monitor actively. Niger’s SOMAÏR mine recorded no production in 2025 due to junta control, eliminating a secondary source of supply. Russia’s nuclear fuel exports face sanctions that reduce non-Western supply alternatives. Kazakhstan’s ownership reforms could grant Kazatomprom up to 90 percent control at joint venture extensions, signaling tighter state control over supply.

A bilateral Canada-India uranium supply arrangement valued at approximately 2.8 billion dollars over ten years will support longer-term demand resilience, but this also means supply commitments lock in at current and rising price levels. Production headwinds appeared in 2025, with Canada’s McArthur River lowering output and in-situ recovery restarts in the US progressing slower than planned. The market shifted from inventory-driven dynamics to production-driven fundamentals, meaning utilities prioritize coverage as strategic stockpiles run low. This transition favors uranium miners with established operations and low all-in sustaining costs, not speculative explorers betting on future discoveries.

Price Momentum Reflects Supply Tightness

Uranium futures hovered around 85 dollars per pound on April 14, 2026, with Trading Economics forecasts suggesting 91.68 dollars per pound within 12 months if demand strengthens as expected. The 30-day price decline of 0.81 percent masks a year-over-year uplift of 32.69 percent, illustrating how structural supply constraints support prices despite near-term volatility. Traders are pricing in a longer-term demand thesis: widespread adoption of nuclear power supports elevated uranium prices beyond near-term noise.

This price environment creates a critical inflection point for uranium mining stocks. Producers with low all-in sustaining costs will capture outsized margins as prices rise toward triple-digit levels. Explorers with high-quality assets in stable jurisdictions will attract capital to fund development. The next phase of this market will separate operators with genuine production capacity from those dependent on speculative price rallies. Understanding which uranium mining companies possess the operational discipline and cost structure to thrive in this environment will determine investment returns over the next five years.

How to Separate Quality Uranium Miners from Speculative Plays

All-in Sustaining Costs Reveal True Profitability

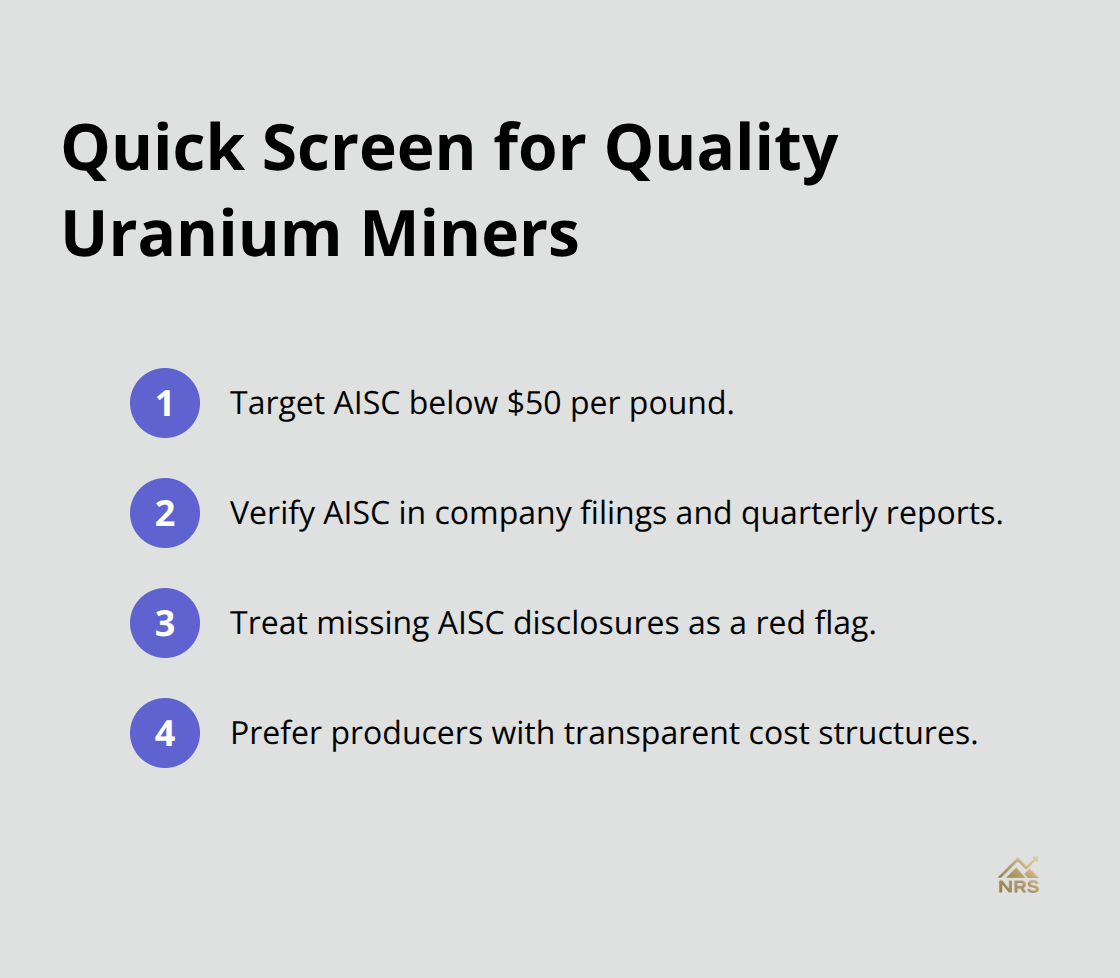

All-in sustaining costs determine whether a uranium miner thrives or struggles when prices fluctuate. This metric directly predicts profitability across commodity cycles. If a producer’s AISC sits at 40 dollars per pound and the long-term contract price reaches 86 dollars per pound, the margin expands to 46 dollars per pound. That same producer faces margin compression to just 5 dollars per pound if prices fall to 45 dollars. Kazatomprom and other major producers already signaled that prices above 86 dollars per pound are necessary to justify production growth, meaning the market expects sustained elevated pricing.

This creates an immediate screening rule: focus on uranium miners reporting AISC below 50 dollars per pound, as these operators generate meaningful cash flow even if prices moderate. Check company filings and quarterly earnings reports for AISC disclosures. If a uranium miner avoids publishing this metric, treat that as a red flag. Producers with transparent cost structures attract institutional capital and maintain operational discipline.

Ore Grade Drives Economics and Competitive Advantage

Ore grade represents the single biggest profitability driver because high-grade deposits dramatically reduce processing and waste costs. The Athabasca Basin deposits in Canada contain grades between 5 and 20 percent U3O8, which is why Canadian producers command premium valuations. Lower-grade deposits succeed only through massive scale or efficient extraction methods like in-situ recovery in stable jurisdictions.

Compare ore grades across your uranium mining stock candidates using company technical reports and prefeasibility studies. A deposit grading 3 percent U3O8 requires fundamentally different economics than one grading 10 percent. This comparison reveals which producers can maintain profitability at lower price points and which ones depend on sustained elevated pricing to survive.

Jurisdictional Stability Separates Value from Volatility

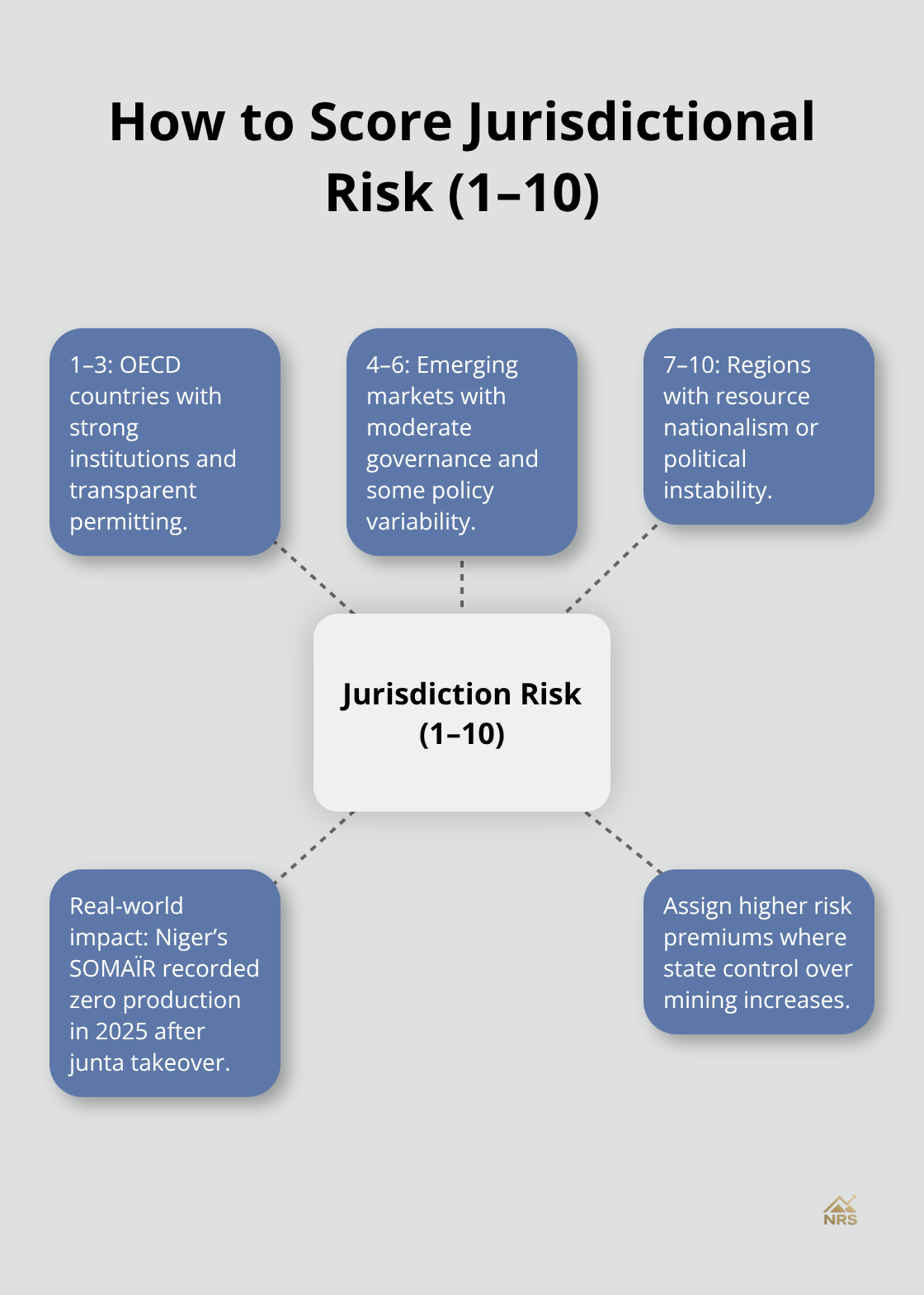

OECD member countries like Canada, Australia, and the United States offer rule of law, transparent permitting processes, and political continuity that reduce sovereign risk. Kazakhstan produces roughly 40 percent of global uranium supply, yet ownership reforms granting Kazatomprom up to 90 percent control at joint venture extensions signal increasing state intervention in pricing and production decisions. This does not eliminate Kazakhstan as an investment source, but it requires assigning higher geopolitical risk premiums to producers operating there.

Niger’s SOMAÏR mine recorded zero production in 2025 after junta takeover, illustrating how abruptly supply can vanish in unstable jurisdictions. Use a 1 to 10 risk scoring system for each jurisdiction where your uranium stocks operate: assign 1 to 3 for OECD countries with strong institutions, 4 to 6 for emerging markets with moderate governance, and 7 to 10 for regions facing resource nationalism or political instability. This framework helps you weight geopolitical exposure against potential upside.

Management Track Records Predict Project Execution

Uranium mine development requires executing multi-year, capital-intensive projects without cost overruns. Examine whether executives have successfully brought uranium or other mining projects into production on schedule and within budget. NuScale Power’s general and administrative expenses surged over 3000 percent to 519 million dollars in Q3 2025 following a 495 million dollar payment to ENTRA1 Energy, a three-year-old firm with only three employees, raising serious credibility questions about project execution.

This scenario demonstrates why investor skepticism toward unproven management teams is justified. Verify management credentials through LinkedIn profiles, prior employment at established mining companies, and documented project completions. Avoid uranium mining stocks where senior leadership lacks direct experience bringing mineral deposits into commercial production. Strong execution records separate operators who deliver value from those who destroy shareholder capital through delays and cost overruns.

The quality metrics you apply to uranium miners-AISC transparency, ore grade, jurisdictional stability, and management track records-directly determine which stocks capture upside as nuclear demand accelerates and which ones underperform. Your next step involves identifying specific uranium mining companies that meet these criteria and assessing their reserve bases and production timelines.

Uranium Mining Stocks Worth Your Capital

Major Producers Control Supply and Pricing Power

Kazakhstan has 14% of the world’s uranium resources and is the world’s leading uranium producer. The company signaled in 2025 that prices above 86 dollars per pound are necessary to justify production growth, which tells you producers view current pricing as insufficient for expansion. For investors, this means exposure to major uranium producers through publicly traded vehicles provides direct leverage to uranium price movements, but you must accept the geopolitical risk embedded in Kazakhstan operations.

Cameco represents a major producer with established Canadian operations offering OECD jurisdiction stability. Cameco approved development of Westinghouse reactors, signaling deeper industry collaboration that could accelerate reactor deployments and uranium demand. This partnership demonstrates how established producers position themselves within the broader nuclear supply chain.

Diversified Energy Companies Maintain Uranium Exposure

EOG Resources reported 1.232 million barrels of oil equivalent daily production in 2025 with approximately 69 percent from oil and natural gas liquids, demonstrating how diversified energy companies maintain uranium exposure without pure-play sector risk. Diamondback Energy added roughly 470,000 net acres after its 2024 merger with Endeavor and operates among the lowest unit cost producers in the Permian, illustrating how cost discipline separates winners from losers across energy sectors including uranium. These companies offer investors exposure to uranium demand without concentrating capital in single-commodity plays.

Junior Explorers Require Rigorous Due Diligence

Junior uranium explorers with high-quality assets in stable jurisdictions attract institutional capital when long-term contracting accelerates, but these stocks carry execution risk that demands rigorous evaluation. IsoEnergy acquired Toro Energy for 49 million dollars in October 2025, signaling management confidence in project development timelines and deposit quality. NexGen and Global Atomic completed equity raises to fund exploration and development drilling, positioning themselves to advance projects toward production decisions. Energy Fuels issued convertible notes to finance inventory build-outs and restart activities, indicating management expects sustained elevated uranium pricing to support payback periods.

Your screening process should eliminate explorers lacking transparent ore-grade disclosures or management teams without prior mining project completions. A 197 million pound supply deficit is forecast for 2040, creating genuine demand for new production capacity, but only explorers with deposits grading above 3 percent U3O8 in jurisdictions rated 1 to 3 on geopolitical risk deserve portfolio allocation.

Alternative Vehicles Reduce Execution Risk

Physical uranium trusts like Sprott Physical Uranium Trust offer 1x price exposure without mining company execution risk, making these vehicles suitable for investors seeking commodity leverage without stock-specific risk. Uranium royalty corporations diversify across multiple producers and development projects while capturing upside from rising prices without incurring mining costs, providing a middle-ground approach between direct equity exposure and pure commodity plays.

The capital markets activity in October 2025 featuring notable financings and M&A demonstrates that institutional investors continue deploying capital into upstream uranium, validating the supply deficit thesis while separating operators with genuine production timelines from speculative plays dependent on price rallies.

Final Thoughts

The uranium market has shifted from speculative positioning to production-driven fundamentals, and uranium mining stocks now reflect genuine supply constraints rather than price momentum alone. Structural deficits, rising nuclear investment, and AI-driven electricity demand create real tailwinds for the next decade, with the IEA projecting annual nuclear investment climbing to 210 billion dollars by 2035 while utilities lock in long-term contracts at elevated price levels. This environment rewards investors who identify producers with transparent cost structures, high-grade assets, and operations in politically stable jurisdictions.

Major producers like Cameco offer established operations and OECD jurisdiction stability, providing direct leverage to uranium prices without concentrated geopolitical risk, while junior explorers with deposits grading above 3 percent U3O8 and proven management teams deserve capital allocation after rigorous due diligence. Physical uranium trusts and royalty corporations provide alternative exposure for investors seeking commodity leverage without mining company execution risk, and Kazatomprom’s signal that prices above 86 dollars per pound justify production growth validates the investment thesis. The 197 million pound supply deficit forecast for 2040 confirms that disciplined capital allocation toward quality uranium mining stocks will capture substantial upside over the next five years.

At Natural Resource Stocks, we help you navigate resource sector opportunities through expert analysis and market insights. Monitor long-term contracting volumes, policy momentum, and geopolitical risk as indicators of future supply dynamics to position your portfolio ahead of the nuclear renaissance.