The nuclear sector is experiencing a fundamental shift. Global governments are committing billions to new reactor construction, and uranium demand is outpacing supply at an accelerating rate.

At Natural Resource Stocks, we’re tracking how this supply-demand imbalance creates real opportunities for investors. This uranium mining stocks outlook examines the catalysts driving the sector, the stocks positioned to benefit, and the risks you need to understand before investing.

The Uranium Supply Crisis Reshaping Global Energy

The numbers tell a stark story. Global uranium demand sits around 185 million pounds annually, yet mine production covers only about 150 million pounds, leaving a structural deficit that widens each year. This gap exists despite decades of warnings, and it will worsen before supply catches up. The World Nuclear Association projects uranium demand growth as nuclear expansion accelerates, but mines operating today cannot close this gap alone. According to Bloomberg analysis from October 2025, U.S. utilities face an estimated 184-million-pound uranium supply shortage over the next decade. That’s not theoretical scarcity-that’s a concrete shortfall utilities must solve through long-term contracts, strategic stockpiling, or accepting higher spot prices.

Where New Supply Actually Comes From

New uranium mines take 10 to 15 years from discovery to first production, and capital spending on exploration has remained depressed for years. Canada’s Wheeler River project represents one of the few near-term additions to global supply, with first production targeted around mid-2028 from Saskatchewan’s Phoenix deposit. Paladin Energy’s Langer Heinrich restart in Namibia offers another incremental source, but neither project moves the needle significantly on the 35-million-pound annual deficit. The U.S. remains heavily dependent on foreign uranium, importing roughly 49 million pounds annually while domestic production hovers near 1 million pounds. This dependency created urgency in Washington-the Department of Energy is funding approximately 900 million dollars to expand HALEU enrichment capacity, signaling long-term commitment to domestic supply resilience. Several uranium mines will obtain environmental permits in the first quarter of 2026, which could accelerate production timelines, but permitting alone doesn’t guarantee shovels in the ground.

Geopolitical Pressure Points and Price Dynamics

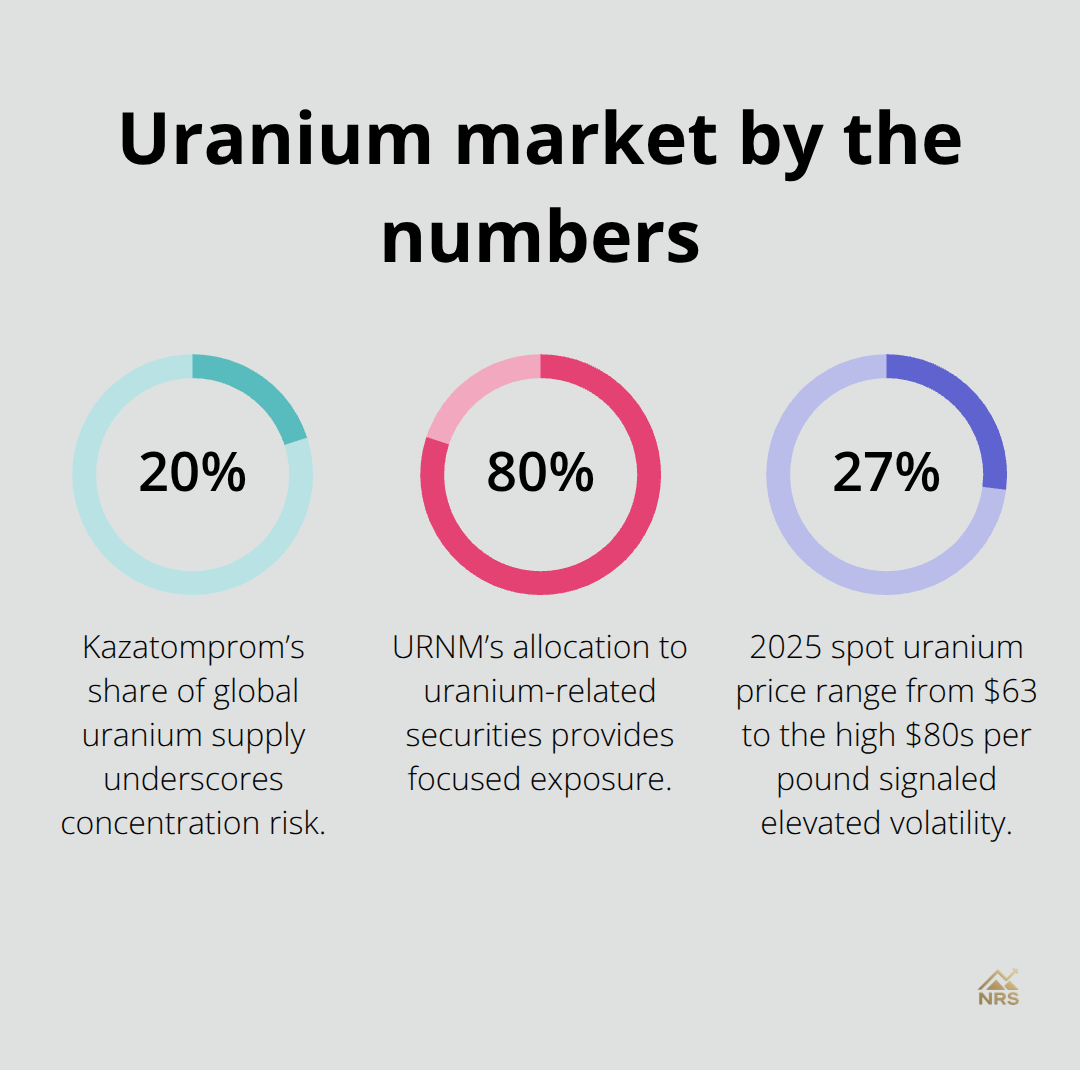

Kazakhstan’s Kazatomprom, the world’s largest uranium producer, supplies roughly 20 percent of global uranium. Any disruption there reverberates across markets immediately.

Geopolitical events reshape metal markets faster than most investors realize, and uranium is no exception-China’s aggressive stockpiling and domestic production expansion through in-situ leaching operations add another variable. China is securing long-term supply for its reactor buildout while simultaneously tightening global availability. Spot uranium prices moved between roughly 63 dollars and the high 80s per pound throughout 2025, but the real signal comes from term prices (longer-term contracts that utilities lock in for future delivery). Term prices have climbed after years of stagnation, indicating utilities recognize they must secure supply at higher levels or face availability risks. Uranium equities like Cameco, up approximately 70 percent over the past year, have already priced in much of this supply tightness, suggesting the market recognizes the structural nature of this deficit.

Why Utilities Drive the Investment Thesis

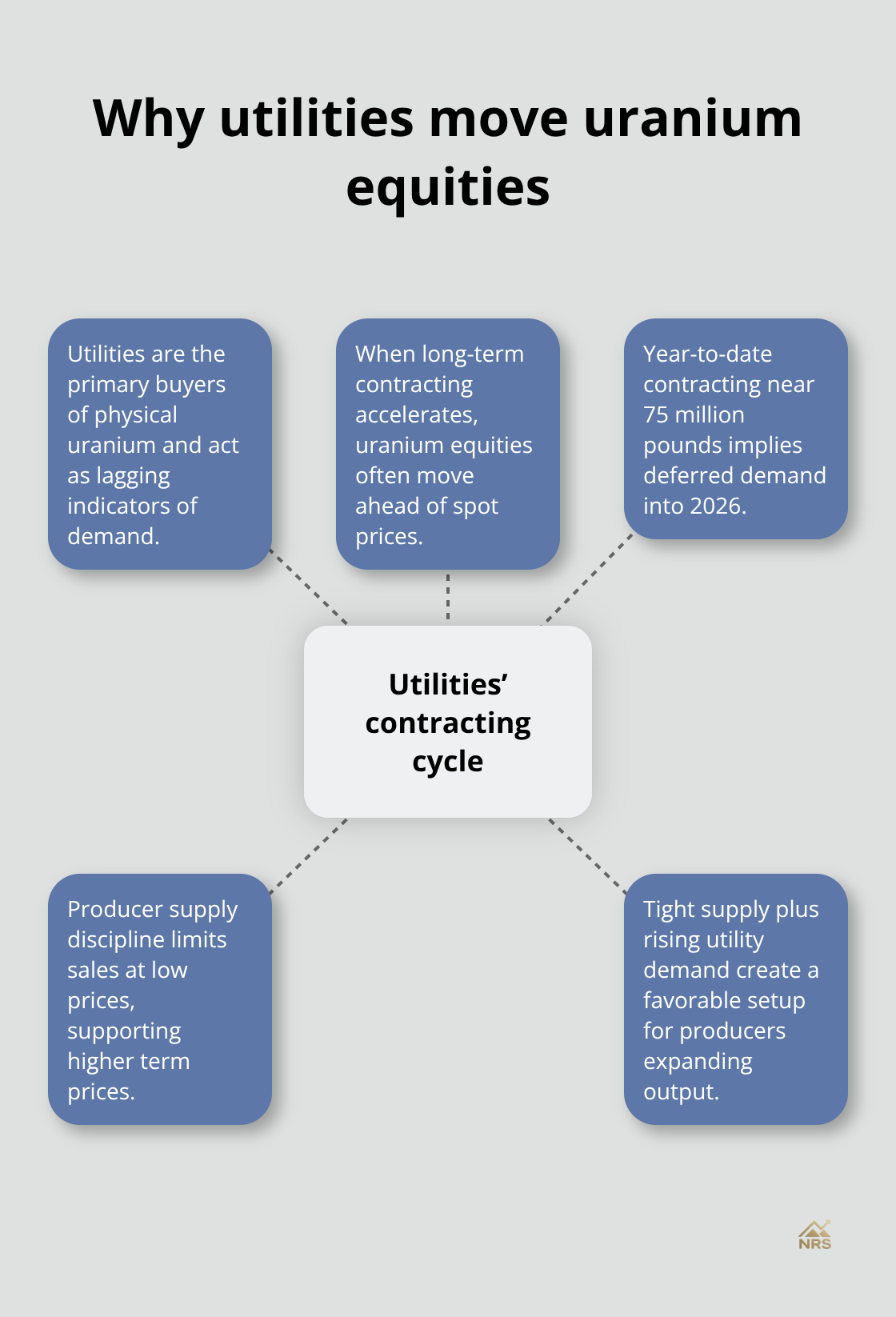

Utilities represent the primary buyers of physical uranium and act as lagging indicators of underlying demand. When utilities accelerate their long-term contracting, uranium equities respond as leading indicators, often moving ahead of spot prices.

Year-to-date contracted volumes show roughly 75 million pounds for the first 11 months of 2025, implying substantial deferred demand into 2026. This procurement pattern matters because utilities cannot simply switch to alternative fuels overnight-nuclear plants require uranium, and securing it at reasonable prices becomes a strategic imperative. Producers have maintained supply discipline, resisting sales at low prices, which helps cap supply growth and supports higher prices over time. The combination of tight supply, rising utility demand, and producer discipline creates a favorable backdrop for uranium mining stocks positioned to expand production.

Which Uranium Stocks Deserve Your Capital

Cameco and Uranium Energy Corp Lead the Pack

Cameco and Uranium Energy Corp stand out as the two producers worth serious consideration, though for different reasons. Cameco represents roughly 19.9 percent of the URNM uranium mining ETF and has demonstrated production discipline by holding inventory rather than flooding markets with supply at depressed prices. The company controls the Cigar Lake operation in Saskatchewan and possesses the scale to expand production as prices justify capital investment. Uranium Energy accounts for approximately 11.6 percent of URNM, operates lower-cost assets, and has positioned itself aggressively for the supply deficit ahead. Both companies have benefited from the structural supply tightness discussed earlier, with Cameco up roughly 70 percent over the past year according to Sprott analysis. Year-to-date contracted volumes of roughly 75 million pounds for the first 11 months of 2025 signal utilities are serious about locking in supply, and equity markets have responded accordingly.

The URNM ETF as a Focused Alternative

If you want focused uranium exposure without picking individual stocks, the URNM ETF tracks the VettaFi Global Uranium Mining Index and maintains an 80 percent allocation to uranium-related securities with a 0.75 percent expense ratio. The fund’s quarterly rebalancing targets companies that derive at least 50 percent of assets from uranium activities, filtering out diversified miners that treat uranium as a secondary business. This screening matters because uranium-focused operators have stronger incentives to expand production when prices rise, directly benefiting from the supply deficit. Sprott’s uranium-focused funds provide an alternative vehicle for physical uranium exposure, offering a hedge against equity volatility while maintaining direct participation in price appreciation.

Valuation and Price Curve Signals

The valuation argument for uranium miners remains straightforward. These companies trade on forward earnings multiples tied to future uranium prices, and the term price curve suggests utilities will accept higher long-term contract prices as supply tightens. Uranium rose to 84.95 USD/Lbs on May 26, 2026, and this level reflects ongoing tightness in the market. The structural supply deficit creates a multi-year tailwind for producers positioned to expand, but near-term price volatility remains certain.

Portfolio Diversification Within Natural Resources

Portfolio diversification within natural resources becomes more relevant when uranium represents a volatile allocation. Uranium mining stocks exhibit higher beta than broader commodity indices, meaning they amplify both upside and downside moves. Pairing uranium exposure with other resource sectors like gold or copper can dampen drawdowns during commodity market corrections while preserving upside when nuclear demand accelerates. This balanced approach protects your capital during sector rotations while maintaining exposure to the uranium supply deficit.

Monitoring Production Guidance and Utility Demand

The practical approach involves sizing uranium positions appropriately within your natural resource allocation and monitoring quarterly earnings from top producers for production guidance changes. Utilities’ long-term contracting pace serves as the leading indicator for sustained demand, so track whether utilities accelerate or decelerate their procurement activity. As new mines approach production timelines and utilities finalize their supply strategies, the investment landscape will shift-understanding these dynamics positions you to capitalize on the next phase of the uranium cycle.

Key Risks and Market Headwinds

Uranium price volatility will test your conviction in this sector. Spot prices swung from $63 to the high $80s per pound throughout 2025, a 27 percent range that translates into significant equity drawdowns for leveraged uranium miners. This volatility stems from long lead times required to bring new mines online, reduced capital expenditure on exploration over the past decade, and geopolitical tensions that reshape supply expectations overnight. When Kazakhstan’s Kazatomprom signals production changes or China announces stockpiling intentions, uranium equities react sharply before fundamentals justify the move. The term price curve offers some stability since utilities lock in longer-term contracts at higher levels, but spot price weakness still pressures mining companies’ near-term cash flows and stock valuations.

Volatility Demands Disciplined Position Sizing

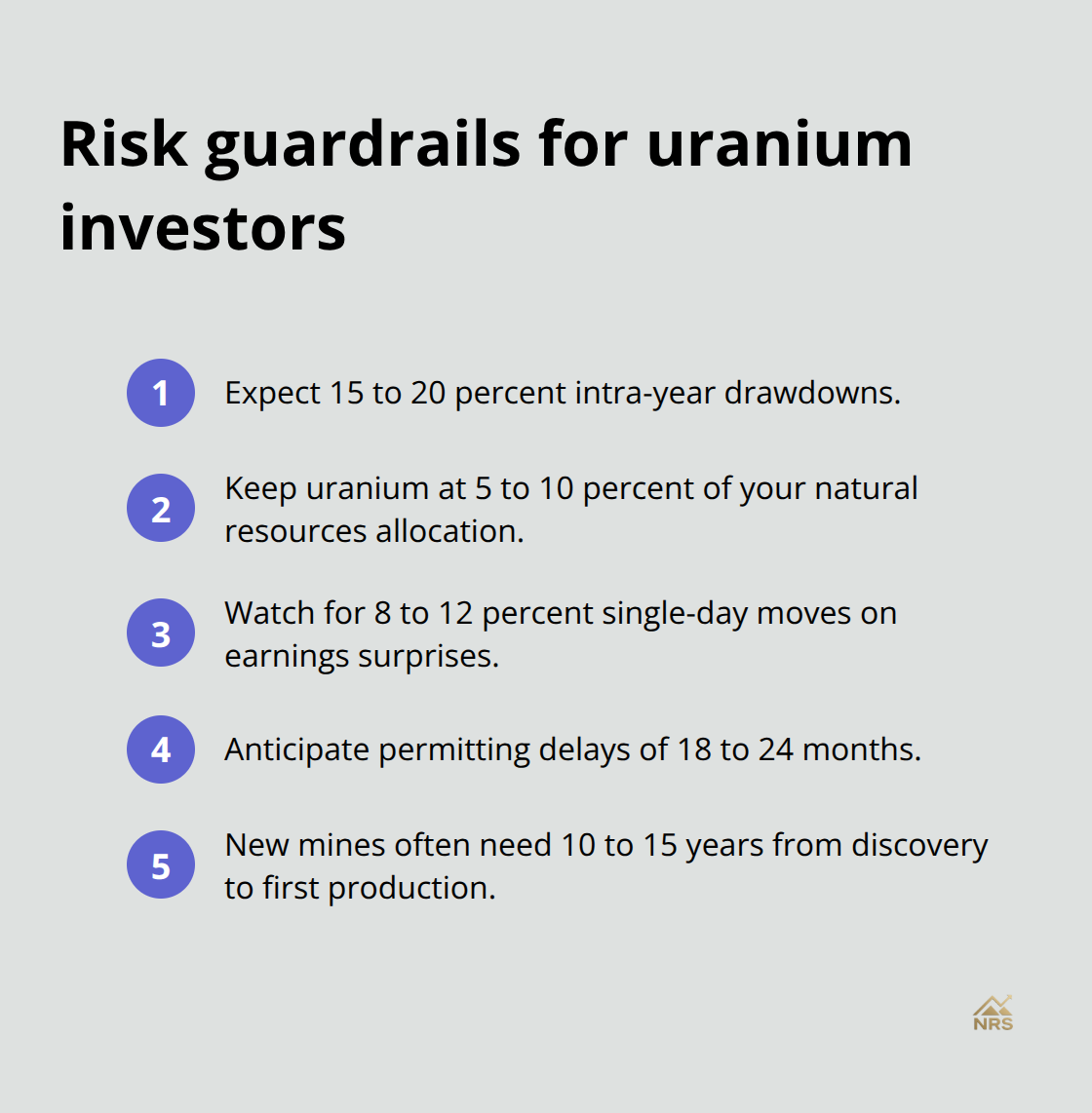

If you own URNM or individual positions like Cameco, expect 15 to 20 percent intra-year drawdowns as a normal feature of uranium cycles, not an anomaly. Position sizing becomes critical here-allocating more than 5 to 10 percent of your natural resources allocation to uranium means absorbing volatility that can derail your broader portfolio strategy.

Monitor quarterly production reports and guidance updates from top holdings, since earnings surprises from Cameco or Uranium Energy typically trigger 8 to 12 percent single-day moves that catch unprepared investors off guard.

Permitting Delays and Environmental Scrutiny Slow Supply Growth

New uranium mines face environmental review processes that routinely extend timelines by 18 to 24 months beyond initial projections. Canada’s Wheeler River project received regulatory approval for mid-2028 first production, but actual production could slip if environmental conditions or Indigenous consultation requirements trigger additional assessments. The U.S. Department of Energy’s $900 million commitment to HALEU enrichment capacity signals policy support, yet actual construction and operational ramp-up face real execution risk that markets underestimate.

Several uranium mines were expected to obtain environmental permits in Q1 2026, but permitting approval does not equal immediate production-capital allocation, labor availability, and commodity price movements all influence when operators actually begin extraction. Environmental standards continue tightening globally, particularly in Europe where uranium mining faces opposition despite nuclear energy’s role in decarbonization. Mine development timelines slip 12 to 18 months from announced targets, meaning the supply gap persists longer than current projections suggest, which actually supports higher uranium prices but delays the production growth that justifies current equity valuations.

Nuclear Faces Structural Headwinds from Cost and Perception

Small modular reactors require 7 to 10 years from approval to grid connection for newcomers, creating demand uncertainty that extends beyond typical commodity cycles. The International Energy Agency notes that replacing nuclear capacity with wind and solar would require roughly $1.6 trillion more investment for advanced economies, yet policy commitment to nuclear remains fragile and subject to election cycles. Germany’s nuclear exit, Belgium’s reactor closures, and ongoing waste disposal debates in multiple countries create perception challenges that restrict uranium demand growth.

If major developed economies accelerate coal-to-gas transitions instead of coal-to-nuclear, uranium demand growth assumptions embedded in current uranium stock valuations become obsolete. The competitive pressure from renewables backed by improving battery storage technology means nuclear faces real displacement risk in markets where capital costs become the primary decision driver. Oil price movements also influence energy capital allocation-if crude falls below $60 per barrel, capital flows shift toward cheaper fossil fuel infrastructure rather than nuclear buildout, reducing uranium demand acceleration. Track geopolitical developments affecting major uranium producers like Kazakhstan and monitor nuclear policy statements from governments representing 40 percent of global electricity demand to gauge whether structural demand assumptions hold.

Final Thoughts

The uranium mining stocks outlook hinges on a simple reality: global uranium demand will outpace supply for years, and this structural imbalance rewards producers positioned to expand. Utilities lock in long-term contracts at higher prices, governments commit capital to reactor construction, and the term price curve signals sustained demand ahead. Cameco and Uranium Energy represent the most direct plays on this supply deficit, while URNM offers focused exposure without single-stock risk.

Strategic positioning requires honest assessment of volatility-uranium equities will experience 15 to 20 percent intra-year drawdowns, and permitting delays routinely extend mine timelines by 18 to 24 months. Size uranium positions at 5 to 10 percent of your natural resources allocation to absorb these swings without derailing your broader strategy. Monitor quarterly production guidance from top producers and track utilities’ long-term contracting pace, as these metrics reveal whether the supply deficit persists or begins closing.

The long-term outlook remains favorable despite near-term risks, with nuclear capacity expanding globally and AI data centers demanding baseload power. Policy commitment to nuclear remains subject to election cycles, and cost competition from renewables poses real displacement risk. We at Natural Resource Stocks track these dynamics through expert analysis designed to help you navigate sector shifts and capitalize on this structural opportunity without overcommitting capital to a volatile sector.