Uranium is entering a new investment cycle, driven by nuclear energy’s role in meeting global decarbonization targets. Governments worldwide are committing billions to nuclear expansion, creating genuine supply-demand imbalances that benefit mining companies.

At Natural Resource Stocks, we’ve identified three critical areas where investors can capitalize on this shift: understanding demand drivers, selecting the right mining stocks, and timing entries around market catalysts. This guide walks you through each.

Why Uranium Demand Is Outpacing Supply

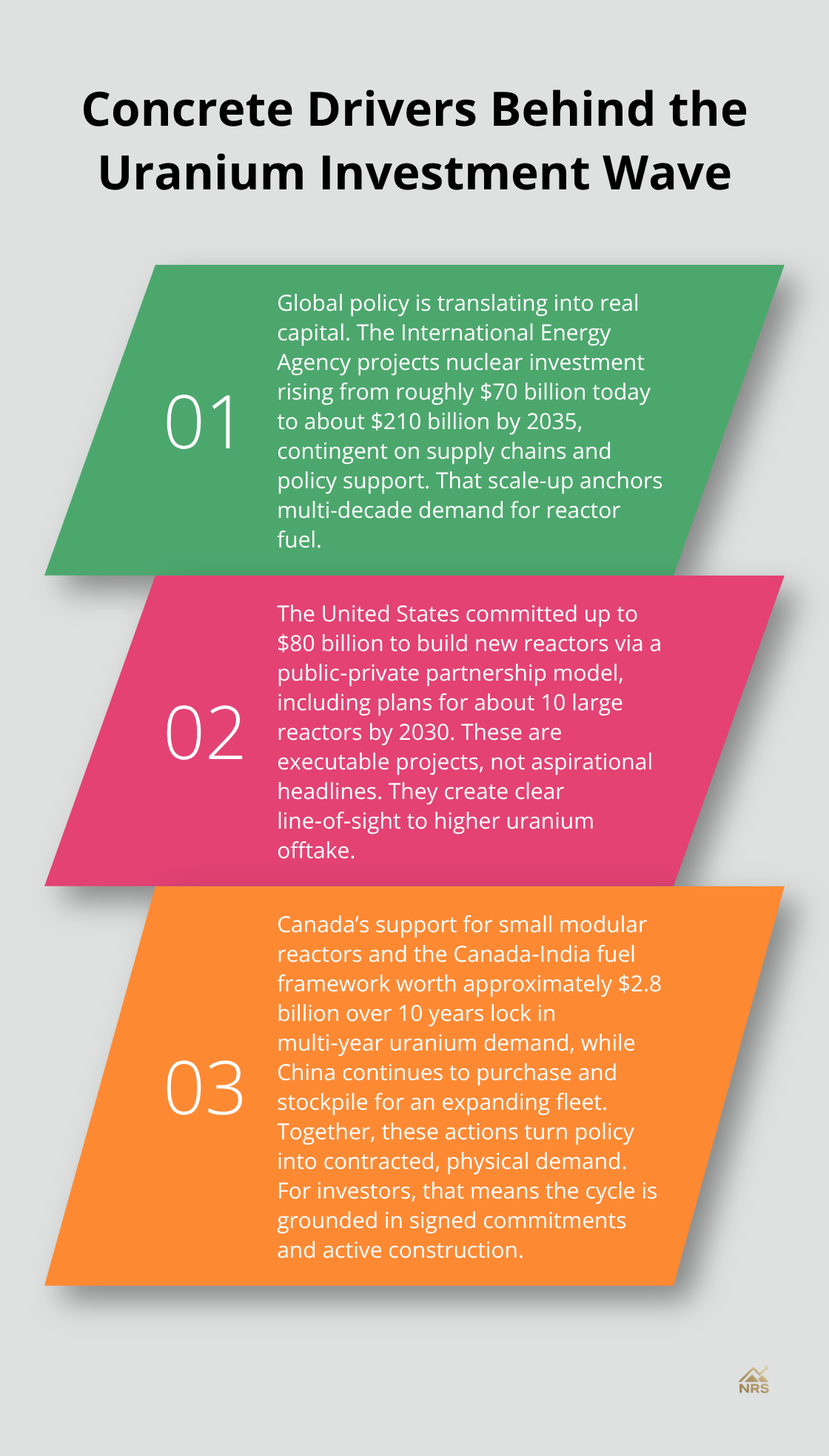

Nuclear Investment Commitments Are Accelerating

Nuclear energy has moved from the margins into mainstream energy strategy. The International Energy Agency projects total nuclear investment rising from roughly $70 billion today to approximately $210 billion by 2035, contingent on robust supply chains and policy support. This acceleration stems from concrete policy commitments, not speculation. The U.S. government committed up to $80 billion to build new reactors through a public-private partnership model, with plans for about 10 new large reactors by 2030. Canada funds small modular reactors at substantial scale, and a bilateral Canada-India fuel framework worth approximately $2.8 billion over 10 years locks in multi-year uranium demand. China continues purchasing and stockpiling uranium for its expanding reactor program, adding structural demand that won’t reverse. These represent signed commitments and active construction, not aspirational targets.

Reactor Expansion Multiplies Uranium Needs

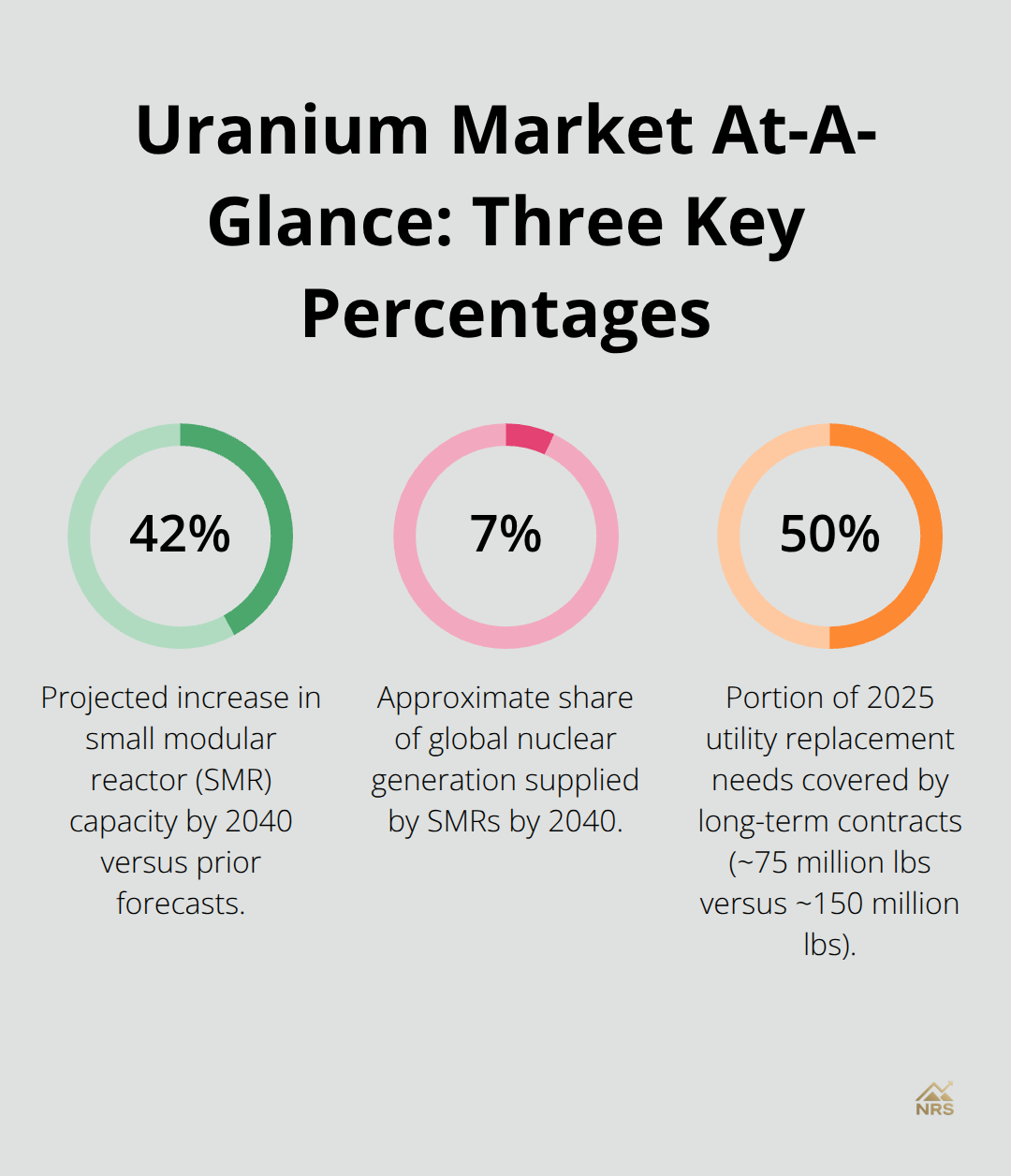

The World Nuclear Association projects small modular reactors will increase capacity by about 42 percent by 2040 versus prior forecasts, with SMRs supplying roughly 7 percent of nuclear generation by 2040. AI-driven electricity demand accelerates U.S. nuclear supply chain expansion, driven by actions from the U.S. Department of Energy and executive orders prioritizing nuclear as critical infrastructure for data centers and industrial power. This demand surge creates a structural floor for uranium consumption that extends decades into the future.

Supply Cannot Match Demand Growth

Global industry demand sits around 185 million pounds per year, but the replacement rate-the amount needed to sustain current reactors-hovers near 150 million pounds annually. Through early December 2025, utilities had contracted only about 75 million pounds, roughly 50 percent of replacement needs, according to Sprott’s uranium market analysis. This contraction deficit signals deferred demand will hit the market aggressively as utilities lock in long-term coverage at higher prices. The structural supply deficit reaches forecast near 197 million pounds by 2040, underscoring the urgency of mine restarts and new production capacity.

Production Lags Behind Requirements

Production has responded slowly to rising demand. McArthur River output reduced in 2025, Kazatomprom signaled lower nominal 2026 production, and in-situ recovery restarts in the U.S. proceeded more slowly than planned. Kazakhstan tightened access to uranium supply through policy moves that reweight ownership toward Kazatomprom, reinforcing price discipline and control over primary supply. Niger governance risk intensified when the junta took control of SOMAÏR in July 2023, with no production from that facility in 2025, highlighting supply-security concerns for European utilities.

Geopolitical Constraints Reinforce Scarcity

Sanctions, export bans, and the Russia-Ukraine conflict continue constraining the nuclear fuel cycle, increasing reliance on non-Western supply and elevating security-of-supply risk for Western buyers. This supply tightness is real and structural, not temporary. These constraints create the conditions where investors can identify which mining companies will benefit most from the price recovery ahead.

Which Uranium Stocks Actually Deliver Returns

Production Scale and Reserve Quality Separate Winners from Losers

Cameco stands alone as the only choice for investors seeking immediate production scale paired with genuine upside leverage. The company controls roughly 14 percent of global uranium reserves at high-grade deposits, trades at about $45.1 billion market cap according to CompaniesMarketcap data, and delivered approximately 70 percent year-to-date gains in 2025. This performance reflects what happens when a producer holds tier-1 assets during a supply crunch: margins expand faster than spot prices climb. Kazatomprom, the world’s largest uranium producer by volume, sits fourth globally at $18.1 billion market cap and maintains supply discipline by resisting sales at depressed prices, which supports the pricing environment for all producers. Energy Fuels trades at roughly $4.0 billion market cap with a 7.0 percent dividend yield, offering income alongside capital appreciation if uranium prices sustain above $75 per pound long-term.

Cost Structure Determines Profit Expansion

The critical insight lies in production cost structure. Cameco’s all-in sustaining costs run substantially below current spot prices, meaning every dollar the market prices uranium higher flows directly to profit. Junior explorers like Denison Mines at $2.85 billion market cap or Uranium Energy Corp near $5.8 billion carry higher leverage to price moves but depend entirely on permitting timelines and funding availability. Several uranium mines will obtain environmental permits in Q1 2026, which will directly trigger production ramp-ups and supply additions that constrain further price upside for later entrants.

Long-Term Contracts Drive Stock Performance, Not Spot Prices

Timing entry points requires abandoning the notion that spot prices drive uranium equities. Long-term contracting at $70 to $80 per pound now determines mining economics, not the spot price bouncing between $63 and $82 in 2025. About 116 million pounds of uranium was placed under long-term contracts by utilities in 2025, creating a procurement deficit that forces aggressive contracting into 2026 and 2027. This deferred demand historically arrives in waves, pushing term prices higher and triggering stock rallies before spot prices visibly move.

Building a Diversified Uranium Portfolio

Diversified exposure through the Sprott Uranium Miners ETF under ticker URNM eliminates single-company risk while capturing upside across producers, mid-tier developers, and fuel-cycle names like BWX Technologies at $18.1 billion market cap. The Sprott Physical Uranium Trust provides physical uranium exposure without mining company execution risk. Pure plays in junior explorers work only if you monitor permit approvals and financing announcements weekly, since these catalysts move stocks 30 to 50 percent in days. Established producers demand less monitoring but deliver slower gains.

Allocation Strategy for the Next Cycle

The practical approach combines 60 percent allocation to large-cap producers like Cameco for stability, 25 percent to mid-tier players offering dividend yields, and 15 percent to explorers with funded development pipelines and near-term permitting visibility. This structure positions your portfolio to capture gains from both immediate price recovery and longer-term supply tightening. With production constraints intensifying and contracting momentum accelerating, the next phase of the cycle hinges on which companies can actually deliver metal to utilities locked into multi-year agreements.

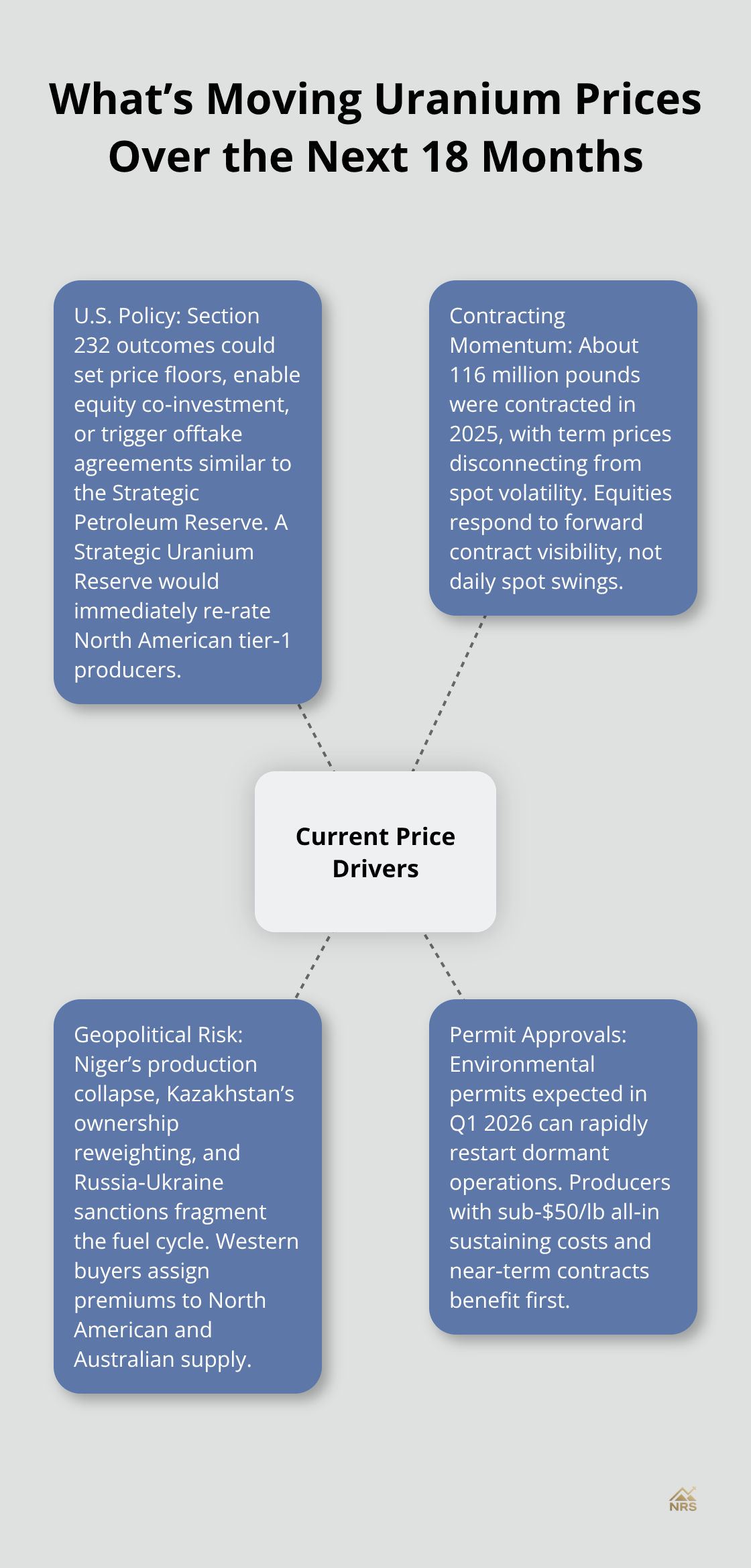

What Moves Uranium Prices and Stocks Right Now

U.S. Policy Creates the Pricing Floor

U.S. policy decisions will drive the next 18 months of uranium pricing more than any other single factor. The Section 232 review on uranium and critical materials was implemented on January 14, 2026, and the outcomes will reshape domestic supply strategy through potential price floors, equity investments, or offtake agreements modeled after the Strategic Petroleum Reserve. This review matters because it signals whether the government will actively support domestic production through direct intervention or rely on market mechanics alone. A Strategic Uranium Reserve announcement would immediately trigger a repricing higher for producers with tier-1 North American assets, particularly those with near-term permitting visibility.

Investors should monitor the USGS critical minerals list and Section 232 developments monthly, since policy shifts cascade into stock movements within days of announcements.

Contracting Momentum Signals Structural Demand

The uranium industry faces a contracting inflection point that investors must track weekly. In 2025, approximately 116 million pounds U3O8 were placed under long-term contracts, still below annual utility uranium requirements. This deferred procurement will compress into late 2026 and 2027, forcing utilities to accept higher long-term contract prices as inventory buffers deplete. The November 2025 contracting surge of 27 million pounds across 14 deals signals utilities are beginning to move, but the backlog remains enormous. Long-term uranium prices reached approximately $86 per pound in 2025, up roughly 8.9 percent year-to-date, yet spot prices rose only 3.6 percent, revealing that term pricing is disconnecting sharply from spot volatility. This separation matters because mining stocks respond to forward contract visibility, not daily spot noise. Investors should monitor monthly contracting volumes released by UxC and Sprott; when monthly volumes exceed 20 million pounds consistently, equity markets typically surge 15 to 25 percent within 60 days as investors recognize the structural floor beneath uranium pricing.

Geopolitical Risk Favors North American Producers

Supply disruptions now carry geopolitical weight that fundamentally alters investment decisions. Niger’s production collapse in 2025 after the July 2023 junta takeover removed meaningful European supply security, forcing Western utilities to compete harder for North American and Australian uranium. Kazakhstan’s policy tightening toward Kazatomprom ownership reweighting signals that the world’s largest producer will maintain disciplined supply and resist panic selling during price dips, which historically props up pricing floors. Russia-Ukraine sanctions continue fragmenting the fuel cycle, and Western buyers face genuine supply-chain vulnerability that justifies premium valuations for producers outside geopolitical risk zones. This reality favors Cameco, Energy Fuels, and other North American operators over junior explorers dependent on permitting in contested regions.

Permit Approvals Trigger Production Ramps

Environmental permits expected in Q1 2026 will trigger rapid production ramp-ups at several dormant operations, which means investors entering after permit announcements face compressed timelines and higher entry prices. The practical implication for investors is straightforward: allocate capital toward companies with immediate production in tier-1 jurisdictions and locked forward contracts rather than speculation on exploration upside. Utilities facing uncovered requirements will aggressively contract into 2026, creating a supply-demand compression that rewards investors positioned in producers with cost structures below $50 per pound all-in sustaining costs.

Final Thoughts

The uranium cycle ahead rewards investors who prioritize production certainty over exploration speculation. Established producers with cost structures below $50 per pound all-in sustaining costs will capture margin expansion as term prices climb toward $90 and beyond, while mid-tier operators offering dividend yields provide income during the contracting surge. Junior explorers work only if you monitor permit approvals and financing announcements with weekly discipline, since environmental permits expected in Q1 2026 will trigger rapid production ramp-ups that compress entry timelines and raise prices for later investors.

Risk management demands you avoid concentration in single junior explorers dependent on permitting timelines outside your control. Build your core position in Cameco or through diversified exposure via the Sprott Uranium Miners ETF, allocate a smaller portion to dividend-yielding mid-caps, and reserve only 15 percent for higher-risk development plays with near-term catalysts. This structure protects you if geopolitical disruptions accelerate supply tightening faster than expected, while capturing upside if policy support materializes through a Strategic Uranium Reserve or Section 232 interventions.

Track contracting volumes released by UxC and Sprott monthly; when monthly volumes exceed 20 million pounds consistently, equity markets typically surge within 60 days. Watch long-term contract pricing relative to spot prices, and follow USGS critical minerals announcements and Section 232 developments, since policy shifts trigger stock movements within days. Natural Resource Stocks provides expert video and podcast content, in-depth market analysis, and insights into macroeconomic factors affecting uranium prices and geopolitical impacts on supply chains to help you position yourself ahead of the next 18 months of structural demand signals.