Gold mining stocks are experiencing a pivotal moment. Macroeconomic shifts, geopolitical tensions, and central bank policies are reshaping demand and valuations across the sector.

At Natural Resource Stocks, we’ve identified both compelling opportunities and real risks that investors need to understand. This analysis breaks down the gold mining stocks outlook to help you make informed decisions.

What’s Driving Gold Prices Right Now

Gold prices surged above $5,300 per ounce in early 2026 due to geopolitical tensions, tariff concerns, and dollar volatility, then retreated below $5,000 as the dollar strengthened. This price action reveals the core drivers shaping the gold mining stocks outlook. Real interest rates and US dollar strength are the primary forces moving gold, according to the World Gold Council and IMF data. When the Federal Reserve signals higher rates or the dollar appreciates, gold becomes less attractive to foreign buyers and carries a higher opportunity cost. Conversely, weakening interest rate expectations or dollar weakness tend to support prices.

Central banks reshape the demand landscape

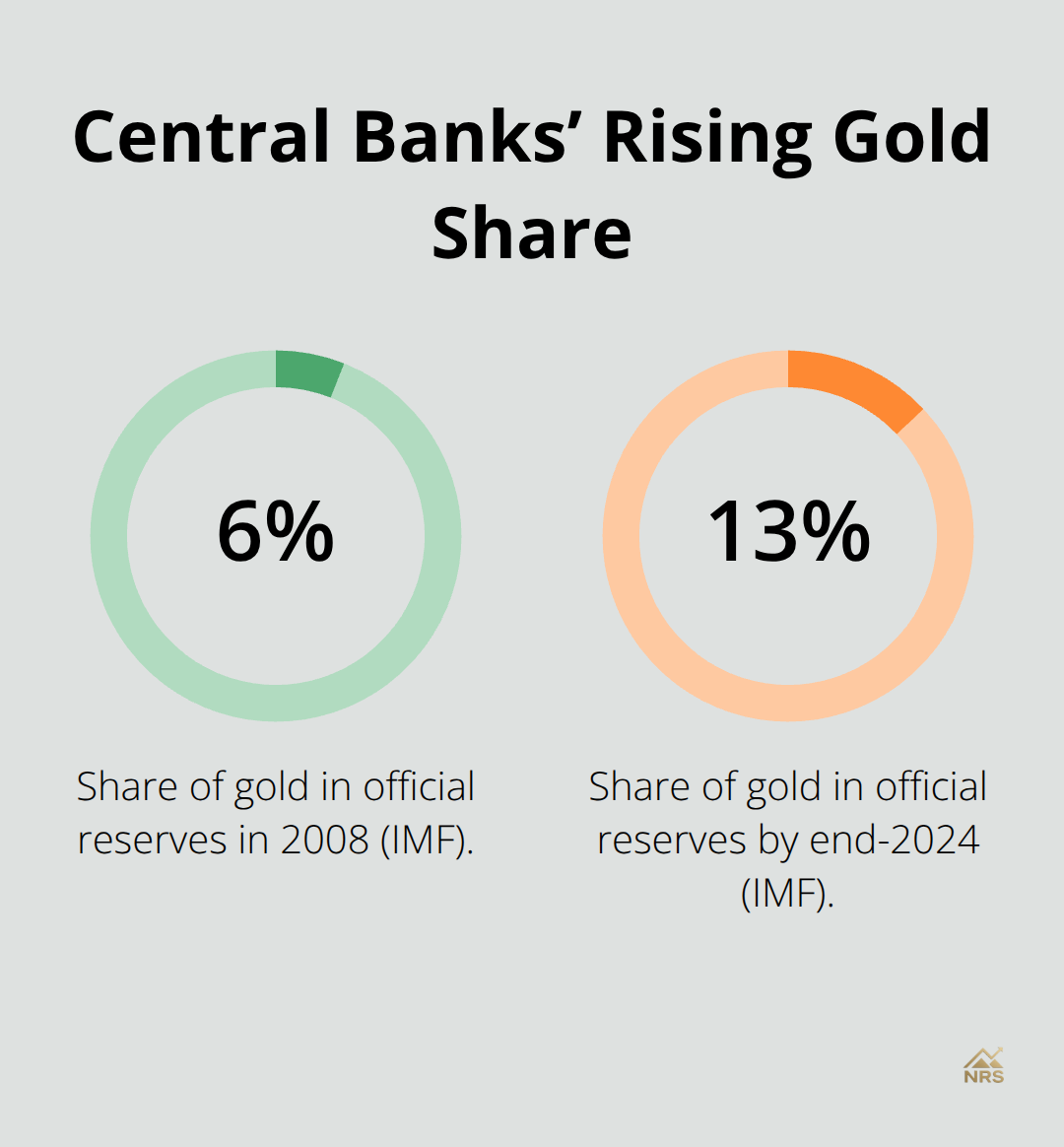

Central banks have become significant buyers, with their share of gold in official reserves rising from about 6% in 2008 to nearly 13% by end-2024 according to IMF figures. This structural shift reflects ongoing concerns about US debt levels and geopolitical risks. If gold prices dip further, central banks may resume or accelerate purchases, providing a price floor that supports mining equities even during macro weakness. This central bank demand creates a stabilizing force that distinguishes gold from other commodities.

Investment flows now dominate market dynamics

Gold investment demand jumped by approximately 990 tonnes in 2025 versus 2024, per World Gold Council data, while silver investment demand rose by about 13.5 million ounces according to the Silver Institute. JPMorgan research shows investors held roughly 2.8% of assets in gold in late 2025, roughly double the level from a decade earlier. This shift toward investment demand matters because investment flows react quickly to macro conditions and prove less stable than jewelry or industrial demand. Investment-driven markets can swing sharply when sentiment shifts, creating both risks and opportunities for mining stock investors.

Silver’s industrial edge offers different upside

Silver presents a different profile, with about 59% of total demand coming from industrial use, including semiconductors and solar applications. Silver could see meaningful upside from increased use in data centers in coming years, making silver-focused miners worth monitoring alongside traditional gold producers. The industrial component of silver demand provides more resilience during periods when investment flows weaken, though it also ties silver more closely to economic cycles.

Price forecasts and entry timing

Haywood Securities forecasts gold averaging $4,906 per ounce in 2026 and $5,000 in 2027, providing a constructive price backdrop for miners. Near-term weakness may present attractive entry points for investors with longer time horizons, as the long-run demand trend remains positive despite short-term volatility. Gold and silver mining stocks will remain sensitive to macro flows and central bank actions, particularly during periods of dollar strength or rising rates. Understanding these price drivers helps investors position for the opportunities that emerge in the next phase of the sector cycle.

Where to Find Real Opportunity in Gold Mining Right Now

Senior producers deliver stability with meaningful upside

Senior gold producers trading at 9.6x next-12-month cash flow represent the core opportunity for investors seeking stability with upside. These established miners generate substantial free cash flow in the current price environment, with 2026 expected to deliver strong returns due to favorable gold prices and high margins, per BMO Capital Markets analysis. Senior miners like Equinox Gold stand out for their scale and ability to deliver consistent production. Equinox’s Valentine and Greenstone projects could each produce over 500,000 ounces annually once fully operational, providing meaningful leverage to sustained higher gold prices. Senior producers with lower all-in sustaining costs outperform during price weakness, making cost structure a critical evaluation metric when comparing mining equities.

Development-stage companies offer outsized returns for patient investors

Exploration and development-stage companies offer outsized returns if projects reach production. Troilus Mining demonstrates the leverage available at current gold prices, with an after-tax net present value around $7.3 billion at $5,000 per ounce and an internal rate of return near 47%, according to Haywood Securities. The company expects a construction decision by year-end, creating a near-term catalyst for investors who identify winners before major value inflection points. Newcore Gold’s Enchi project in Ghana will deliver a pre-feasibility study in June, providing another near-term catalyst to monitor. Thesis Gold’s Lawyers-Ranch project in British Columbia could rank among Canada’s top-tier gold-silver mines, offering early-stage exposure to projects with genuine production potential in stable jurisdictions. These development-stage opportunities require more research and carry execution risk, but the potential returns justify the additional due diligence for investors with appropriate risk tolerance.

Income streams from dividends and streaming arrangements

Streaming and royalty companies like Franco-Nevada collect production shares from miners without operational risk, typically offering dividend growth characteristics approaching dividend aristocrat status. Senior producers with strong cash generation increasingly return capital through dividends as record margins persist. BMO Capital Markets highlights Aris Mining, Discovery Silver, Montage Gold, and Newmont as top picks, each offering different exposure profiles from pure gold to precious metals diversification. The merger and acquisition activity reshaping the sector supports valuations across the board, with high-quality development projects commanding significant takeout premiums that benefit shareholders of acquired companies. This consolidation trend creates multiple pathways for investors to capture value, whether through direct ownership of acquired assets or through the appreciation that precedes takeover announcements.

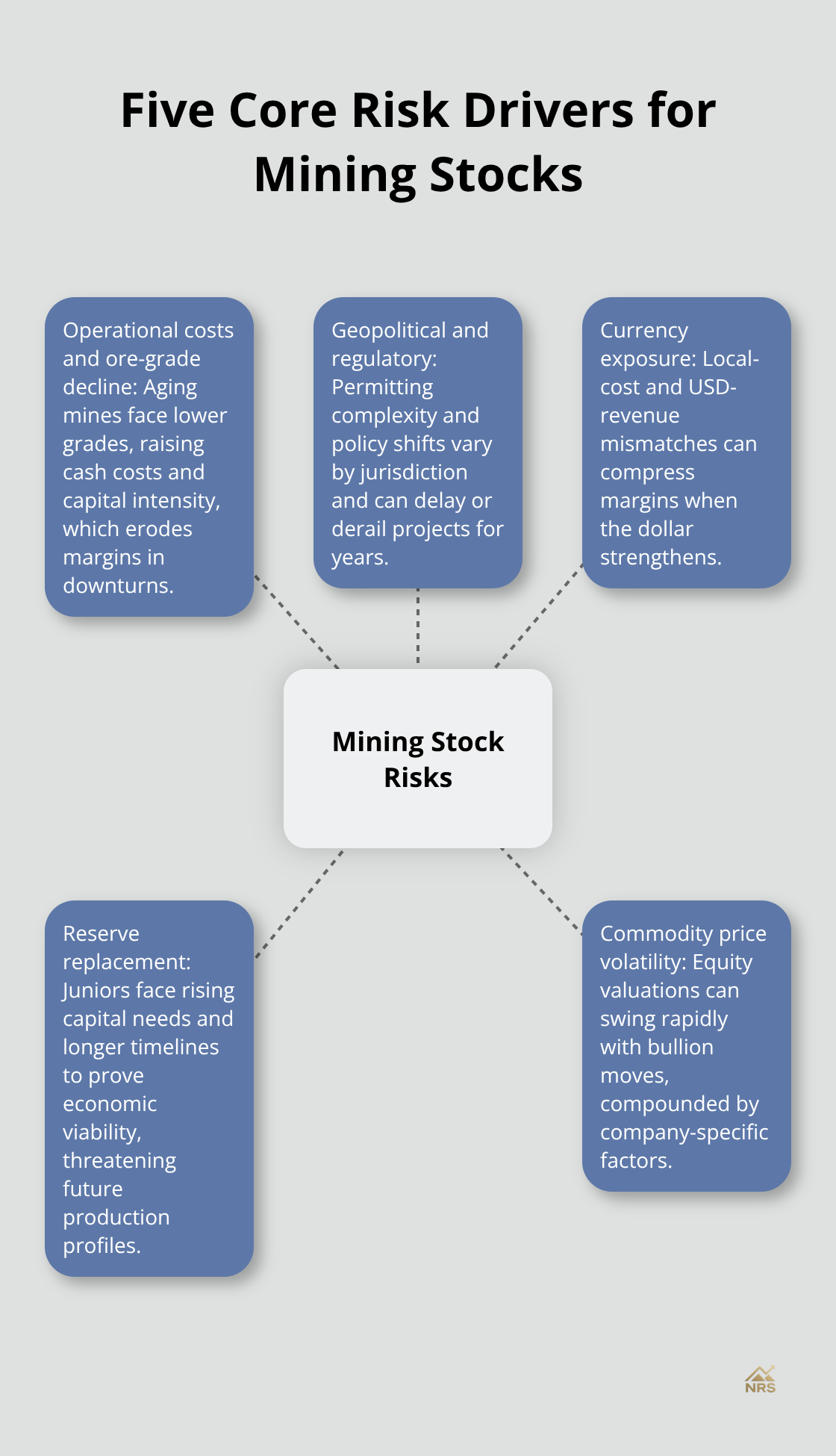

Real Risks That Can Derail Mining Stock Returns

Gold mining stocks carry operational, regulatory, and market risks that can wipe out gains faster than rising prices create them. Understanding these risks helps investors avoid costly mistakes when evaluating mining equities.

Operational challenges compound as mines age

War-driven energy-cost pressures remain a genuine concern, though BMO Capital Markets argues the issue is overdone in the near term and miners should source fuel without major shortages. The real operational risk lies elsewhere: ore grade declines increase cash costs and capital intensity, forcing miners to process more material to sustain output. This problem compounds over time as mines age and operators exhaust higher-grade ore bodies. Miners with higher all-in sustaining costs face margin erosion faster during price downturns, making cost structure analysis essential before committing capital to any mining equity.

Geopolitical and regulatory hurdles vary sharply by location

Geopolitical risk varies sharply by jurisdiction. Mining operations in stable countries like Canada and Australia face different regulatory hurdles than projects in emerging markets where permitting delays and policy changes can derail development timelines entirely. Fury Gold Mines illustrates this dynamic, positioned as a potential takeover target partly because its Eau Claire asset sits in Quebec’s James Bay region where consolidation pressures are intense. Environmental and ESG regulations elevate operating costs substantially, particularly for newly developing projects in jurisdictions with stricter standards. The World Bank notes that permitting complexity now extends project timelines by years in many regions, directly pressuring returns on capital.

Currency exposure amplifies during dollar strength

Currency exposure creates another layer of risk that many investors overlook. Miners with local costs in weaker currencies but revenue primarily in US dollars benefit from favorable exchange rates, yet face margin compression when the dollar strengthens. This dynamic amplifies during periods of dollar strength like early 2026, when gold prices retreated below $5,000 despite strong fundamentals. Investors should monitor currency trends alongside metal prices when evaluating mining stocks with significant international operations.

Reserve replacement and execution delays threaten long-term production

Reserve replacement risk remains a persistent long-term constraint. Exploration success and new reserve discovery directly influence future production profiles, yet junior explorers face mounting capital requirements and longer timelines to establish economic viability. First Mining Gold awaits an environmental assessment decision for Springpole in Ontario, and 1911 Gold targets Canadian producer status by 2027 with the True North project, but execution delays can push these timelines further out. These project-specific risks require thorough due diligence before investors commit capital to development-stage companies.

Commodity price volatility remains the dominant risk factor

Gold equities tend to move with bullion prices but carry additional company-specific risks such as project execution and balance-sheet health. Miners with lower all-in sustaining costs outperform during price weakness, making cost structure a critical evaluation metric when comparing mining equities. Commodity price volatility remains the dominant risk factor that can rapidly shift mining stock valuations regardless of operational performance.

Final Thoughts

The gold mining stocks outlook reflects a sector positioned between structural tailwinds and near-term volatility. Central banks shifted their reserve composition toward gold, rising from 6% in 2008 to nearly 13% by end-2024, creating a stabilizing demand floor that distinguishes this cycle from previous ones. Investment demand jumped 990 tonnes year-over-year in 2025, signaling institutional conviction despite price swings, and these fundamentals support a constructive long-term case for mining equities even as short-term weakness creates entry opportunities for disciplined investors.

The opportunities reward selectivity across multiple segments. Senior producers trading at 9.6x next-12-month cash flow offer stability with meaningful upside as record margins persist, while development-stage companies like Troilus Mining present outsized returns for investors willing to accept execution risk, with potential internal rates of return exceeding 40% at current gold prices. Streaming and royalty companies provide income streams with lower operational complexity, and sector consolidation benefits shareholders of acquired assets through multiple pathways to capture value.

The risks demand equal attention before committing capital. Ore grade declines and rising all-in sustaining costs compress margins as mines age, making cost structure analysis non-negotiable, while geopolitical and regulatory hurdles vary sharply by jurisdiction with permitting delays now extending project timelines by years in many regions. Currency exposure amplifies during dollar strength, directly pressuring returns on international operations, and reserve replacement risk threatens long-term production profiles, particularly for junior explorers facing mounting capital requirements. We at Natural Resource Stocks provide expert analysis and market insights to help you navigate these dynamics and balance opportunity against risk through disciplined research and diversification.