Natural gas remains a cornerstone of global energy supply, yet the sector faces mounting pressures from renewable transitions and volatile commodity markets. At Natural Resource Stocks, we believe investors need a clear-eyed view of both the opportunities and risks in this space.

This guide examines the natural gas stocks outlook across production trends, investment potential, and the regulatory headwinds reshaping the industry. Whether you’re seeking income or growth, understanding these dynamics is essential to positioning your portfolio effectively.

Where Natural Gas Markets Stand Today

Price Signals and Storage Dynamics

Henry Hub spot prices hit $4.98 per million BTU in January 2026, marking a sharp move upward from earlier lows and signaling tighter near-term supply conditions. The NYMEX February contract settled at $4.875/MMBtu, while the 12-month strip averaged $3.970/MMBtu, reflecting trader expectations of seasonal storage balance through winter. These price movements directly influence stock valuations across the natural gas sector-when prices spike, producers capture higher margins and boost shareholder returns; when they collapse, even efficient operators struggle.

U.S. working gas in storage stood at 3,065 billion cubic feet as of mid-January 2026, sitting 177 Bcf above the five-year average. However, the withdrawal pace remained 2 percent slower than historical norms, meaning inventories drain more gradually than usual. If this slower drawdown continues through March, end-of-season storage could land near 1,995 Bcf-roughly 177 Bcf above the five-year average. This surplus cushion matters enormously for natural gas equities because bloated inventories typically suppress prices heading into spring, limiting upside potential for producers and midstream operators alike.

European Demand Collapse and LNG Reorientation

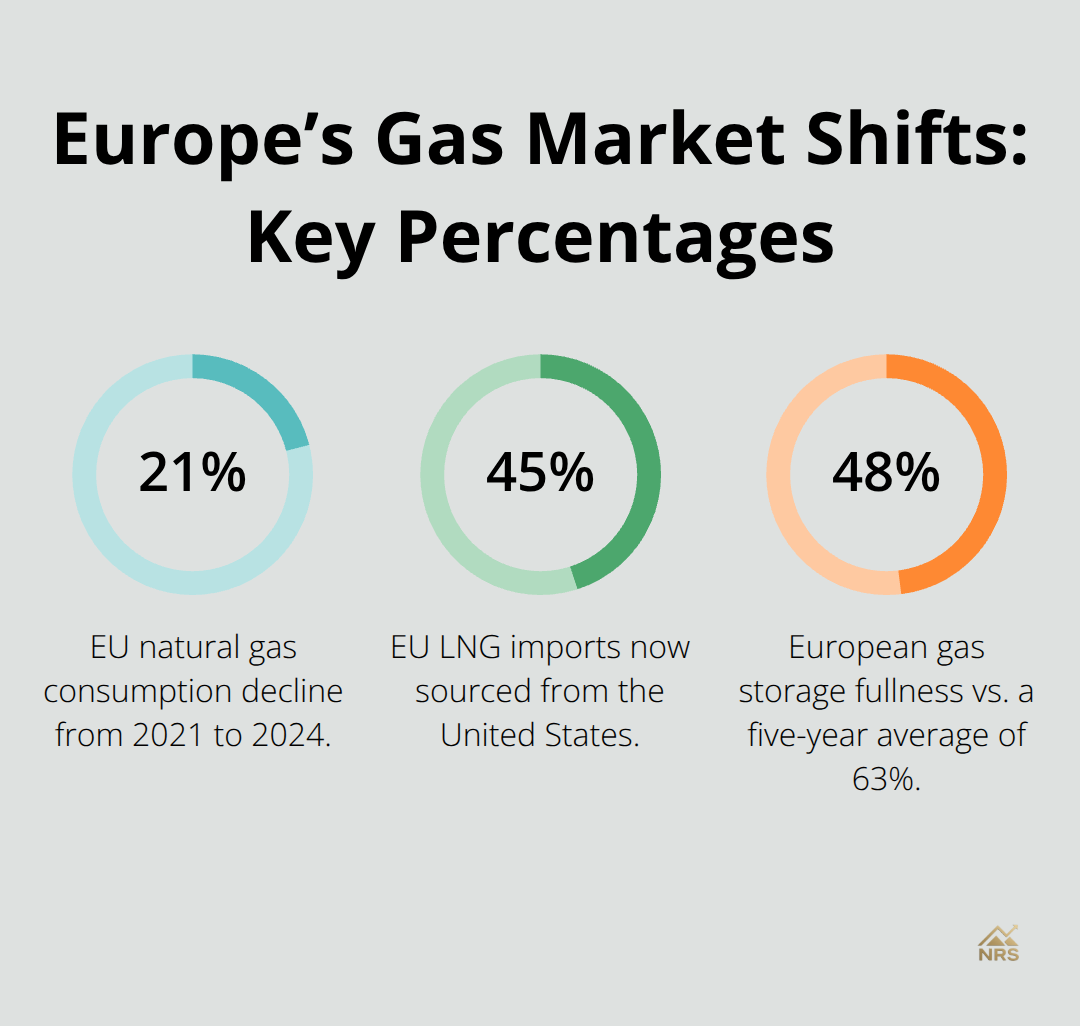

Global supply dynamics amplify this pressure considerably. European natural gas consumption fell from 421 billion cubic meters in 2021 to just 332 bcm in 2024, a 21 percent decline driven by renewable buildouts and industrial weakness. The EU now sources almost 45 percent of its LNG from the United States, a dramatic shift away from Russian pipeline gas. This reorientation reshapes global LNG flows and creates new competitive dynamics for U.S. producers.

Asia’s LNG demand remains robust, with East Asia prices hovering around $10.73/MMBtu in January 2026. This creates genuine tension: when Asian buyers bid aggressively for LNG cargoes, Europe faces tighter supplies despite having 33 operational LNG terminals with 215 bcm/year regasification capacity. U.S. LNG export activity stayed brisk through January with 37 vessels departing U.S. ports. This export strength supports domestic producer revenues, but it also diverts gas away from domestic markets, keeping Henry Hub prices elevated.

Production Capacity and Geopolitical Risks

The U.S. natural gas rig count stood at 122 rigs as of mid-January, down from historical peaks but still indicating sustained production capacity. Geopolitical risks-particularly around the Suez Canal and Hormuz Strait for LNG shipping, plus ongoing tensions affecting Russian pipeline flows-mean supply disruptions remain a real threat. Europe’s storage sits at only 48 percent full versus a five-year average of 63 percent, leaving the continent vulnerable to cold snaps or export interruptions.

For natural gas stock investors, this combination of factors translates to elevated volatility and unpredictable margin swings. Supply tightness in one region can quickly shift to oversupply elsewhere, and global LNG competition means U.S. producers face both tailwinds and headwinds depending on where international demand peaks. Understanding these cross-currents becomes essential as you evaluate which natural gas equities offer the best risk-adjusted returns in this environment.

Where Natural Gas Stock Value Lies

Value Plays in Mature Infrastructure

Phillips 66 trades near $139 with a market cap around $59.5 billion and offers a 3.3 percent dividend yield alongside a lean 0.42 price-to-sales ratio. The company completed the DCP Midstream acquisition in 2023 and plans the Pinnacle Midland deal to expand gas processing capacity, positioning it to capture margin expansion as volumes flow through its infrastructure. Ovintiv represents better value at $46.57 with a 6.58 price-to-earnings ratio and 2.58 percent yield, supported by aggressive share buybacks renewed through October 2024. Coterra Energy trades at $26.85 with 78 percent of its 2023 natural gas output from Marcellus Shale, a prolific and low-cost basin that should benefit from sustained higher prices. Analysts assign a consensus price target of $34.47 on Coterra, implying 28 percent upside from early 2026 levels.

Growth Opportunities with Higher Valuation Risk

EQT Corporation deserves serious consideration despite its 27.6 price-to-earnings multiple. The company operates as the largest U.S. natural gas producer and pursues vertical integration with Equitrans Midstream, a move that locks in midstream margins and reduces earnings volatility. Analysts project 249 percent earnings growth for EQT, reflecting both production ramp and margin capture from the integrated structure. Southwestern Energy, formed from the Chesapeake merger, carries analyst projections for 89.8 percent earnings growth and roughly 23 percent upside from 2024 valuations. These growth plays carry higher valuation risk, but they offer exposure to production expansion precisely when global LNG demand remains competitive and U.S. export infrastructure operates near capacity.

Income-Focused Strategies

Dividend-focused investors should examine Kimbell Royalty Partners, which yields 11.15 percent and trades at only 27.9 times earnings, though the high yield reflects execution risk typical of smaller partnerships. The company’s distribution structure appeals to income seekers willing to accept volatility in exchange for substantial cash returns.

Matching Strategy to Market Conditions

Value and growth opportunities coexist in natural gas equities right now, but they reward different investor temperaments and time horizons. Producers with established midstream integration or cost advantages in low-decline basins tend to outperform when prices normalize downward, while pure-play upstream companies capture the most upside when international LNG competition stays hot and storage remains tight. This divergence in performance patterns means your stock selection must align with your outlook on near-term price direction and your tolerance for earnings volatility. As regulatory pressures mount and the energy transition accelerates, understanding which business models withstand structural headwinds becomes the next critical filter for portfolio construction.

Why Natural Gas Stocks Face Structural Headwinds

Renewable Energy Reshapes Gas Demand Patterns

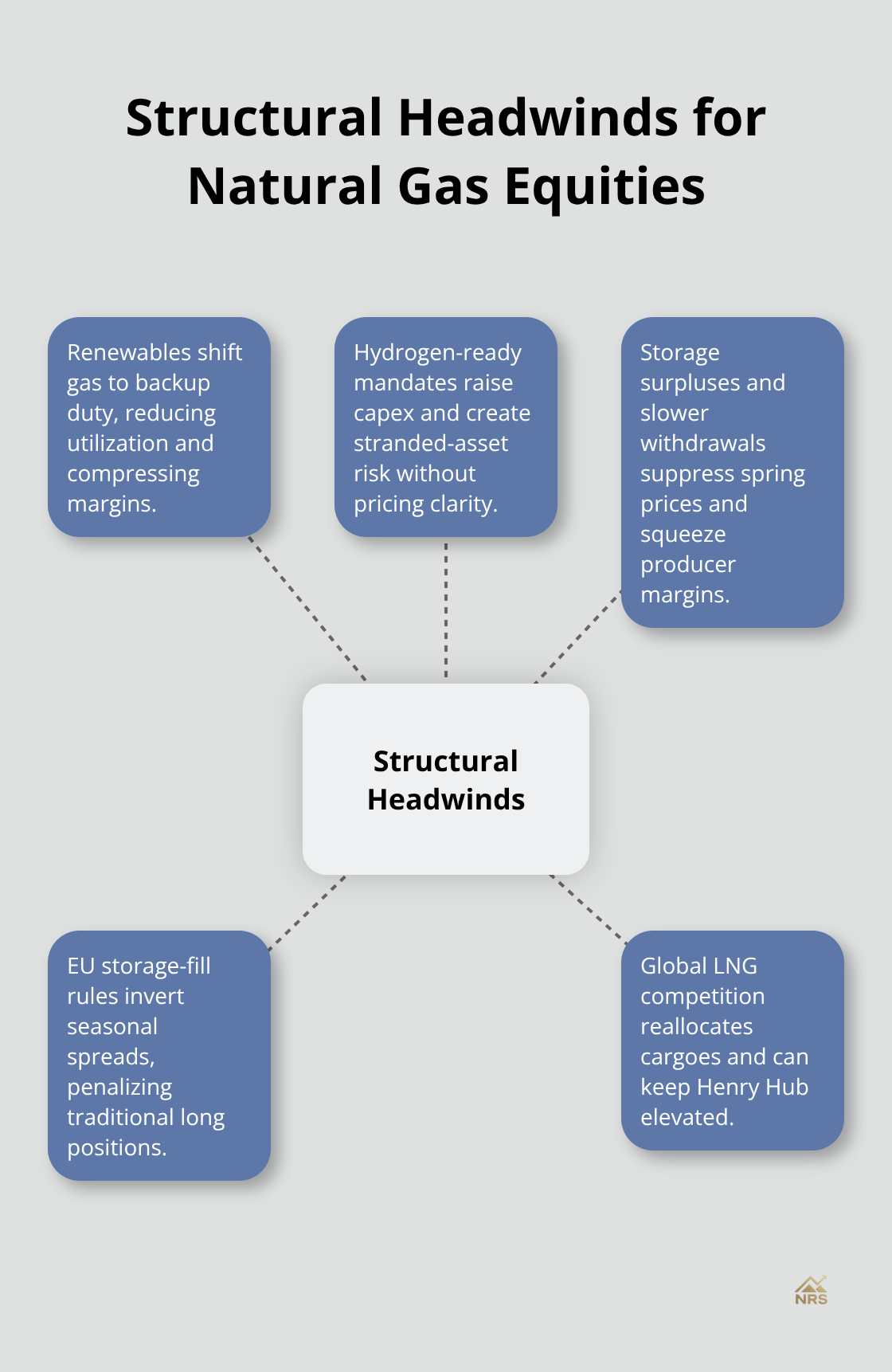

Renewable energy transition actively reshapes electricity grids across Europe and North America right now. Germany’s natural gas consumption accounted for 25.9 percent of primary energy in 2024, yet the country targets peak electricity demand rising from 75-80 GW today to 100 GW by 2035 and 135 GW by 2050, driven almost entirely through electrification and renewable capacity additions. This matters for natural gas investors because higher renewable penetration doesn’t eliminate gas demand-it fragments it. Gas plants increasingly operate as backup capacity rather than baseload generation, which compresses utilization rates and margin stability. EU gas consumption will drop 22 percent from 2024 to 2035 while LNG imports rise, meaning producers must compete harder for shrinking domestic markets while exporting more volume at potentially lower realized prices.

Hydrogen Requirements Create Stranded Asset Risk

Germany’s policy response reveals the structural challenge ahead. The government targets up to 20 GW of new gas-fired capacity by 2030 via a technology-neutral mechanism, but these plants must be hydrogen-ready to justify long-term investment. This regulatory requirement forces producers and midstream operators to fund expensive infrastructure retrofits without guaranteed hydrogen supply or pricing clarity, which creates stranded asset risk for companies slow to adapt. Investors holding equities in firms without hydrogen transition plans face significant downside exposure as regulators tighten environmental standards across jurisdictions.

Storage Surplus Suppresses Spring Prices

Commodity price volatility remains the most immediate threat to portfolio returns, and recent storage dynamics illustrate the danger clearly. The EIA reported U.S. storage 177 Bcf above the five-year average in January 2026, with withdrawal rates running 2 percent slower than historical norms-a seemingly modest detail that could translate to 1,995 Bcf in end-March inventories, another 177 Bcf surplus. This storage cushion directly suppresses spring prices and crushes producer margins precisely when natural gas equities need positive catalysts. Regional volatility compounds this pressure: Southeast consumption surged 26 percent week-over-week in January through heating demand, yet this regional spike doesn’t sustain prices at Henry Hub because storage remains abundant nationally. Investors holding pure upstream producers face this asymmetry constantly-a cold snap drives regional premiums that vanish once storage reaches seasonal targets.

Regulatory Mandates Distort Market Spreads

Regulatory tightening amplifies commodity exposure rather than reducing it. The EU’s 90 percent storage-fill mandate by November 1st created negative summer-winter spreads in 2024, which forced traders to pay for physical gas in summer and accept losses when selling into winter-an inverted market that penalizes traditional long positions.

Producers relying on commodity price strength without integrated midstream or downstream operations face margin compression from both directions: storage abundance suppresses absolute prices while regulatory mandates distort seasonal spreads. Your equity selection must account for this reality through favoring producers with contracted volumes, diversified geographic exposure, or midstream integration that locks in processing margins independent of price direction.

Final Thoughts

Natural gas stocks reward investors who match their equity selection to realistic market conditions rather than chase structural tailwinds that no longer exist. Storage surpluses will suppress spring prices, regulatory mandates increasingly favor hydrogen-ready infrastructure over traditional gas plants, and global LNG competition forces U.S. producers to export volume at whatever price international markets dictate. Value investors should focus on established players like Phillips 66 and Ovintiv that offer reasonable dividend yields and lean valuations, while growth-oriented portfolios can justify higher valuations for EQT and Southwestern Energy only if you believe sustained LNG export demand will support production ramps through the 2030s.

The structural transition reshaping energy markets means natural gas will remain essential for decades, but as backup generation rather than baseload power. This shift compresses utilization rates and margin stability for pure upstream producers while favoring integrated operators and infrastructure companies. Your positioning should reflect this reality through diversification across value, growth, and income strategies rather than concentrated bets on any single business model.

The natural gas stocks outlook depends on your ability to monitor storage data, regulatory developments, and global LNG flows rather than rely on passive exposure to commodity price movements. Visit Natural Resource Stocks to access in-depth commentary on macroeconomic factors and geopolitical impacts shaping resource markets. Building a resilient natural gas portfolio requires ongoing analysis of these dynamics across your holdings.