Platinum remains one of the most misunderstood precious metals in investment circles, yet its market dynamics shape opportunities across automotive, industrial, and energy sectors.

At Natural Resource Stocks, we’ve tracked platinum market trends closely and noticed how supply disruptions, geopolitical tensions, and shifting demand patterns create distinct entry points for investors. Understanding these cycles isn’t optional-it’s the foundation of smart portfolio positioning in this volatile market.

Where Platinum Stands Today

South Africa is projected to mine 60–70% of the world’s platinum, dominating global supply chains and creating the market’s defining characteristic: structural scarcity that amplifies price swings. According to Trading Economics, platinum traded at 2,027.60 USD per troy ounce on April 27, 2026, down just 0.14% that day but up 105.47% year over year. That dramatic annual gain masks a critical reality. The World Platinum Investment Council forecasts 2025 as the third consecutive annual deficit, with above-ground stocks depleted to roughly five months of demand cover. This inventory drain removes the safety net that typically stabilizes markets during demand downturns. When physical supply tightens this severely, even modest demand disruptions trigger sharp price moves. The platinum lease rate, which measures the cost of borrowing physical metal, averaged around 12% year-to-date in 2025 according to LBMA data, up from just 1% in 2024. That ten-fold jump signals dealers and refiners scrambling to secure actual metal rather than paper contracts.

Supply Constraints Run Deep

Mining output from South Africa faces mounting pressure from aging infrastructure and power costs that make new project economics unattractive. Platreef and similar ventures offer limited production upside. Russia’s platinum output will fall further due to sanctions, removing another significant supply source. Recycling has improved but remains insufficient to offset declining mine production. The World Platinum Investment Council expects mine supply to rise only 2% year-over-year in 2026 after falling 5% in 2025, while recycling grows 10% annually. This gap between declining primary supply and growing recycling reveals that the market cannot replace lost mine output fast enough. For investors, this matters because price floors rise when physical scarcity persists. Platinum’s price peaked at 2,923.70 USD per troy ounce in January 2026 before declining, yet Trading Economics projects prices around 2,425.92 USD per troy ounce within 12 months. That forecast assumes supply constraints remain active.

Automotive Demand Faces Structural Headwinds

Automotive catalytic converters drive roughly 36-44% of platinum demand according to the World Platinum Investment Council, making the sector platinum’s single largest consumer. Yet this exposure creates vulnerability. The shift toward electric vehicles reduces catalytic converter demand structurally over time, though diesel and gasoline engines will remain part of the drivetrain mix for the foreseeable future with increasing hybridization. This transition unfolds gradually, not overnight, which means automotive demand will remain substantial for years to come. Industrial applications including petroleum refining, nitric acid production for fertilizers, and glassmaking account for 23-35% of demand and provide more stable consumption patterns than automotive alone.

Hydrogen and Emerging Technologies Offer Growth

Hydrogen fuel cells represent the emerging opportunity, using platinum catalysts in proton exchange membrane technology that produces green hydrogen for power, heating, steelmaking, and sustainable aviation fuels. This application could offset some automotive losses as energy transition accelerates. Jewelry demand ranges from 24-30% of total platinum consumption, with particular strength in the US market for engagement rings and long-standing preference in Japan. Investment demand has swung wildly between negative 8% and positive 14% of total demand over the past five years, reflecting sentiment shifts more than fundamental supply-demand balance.

China Reshapes Investment Flows

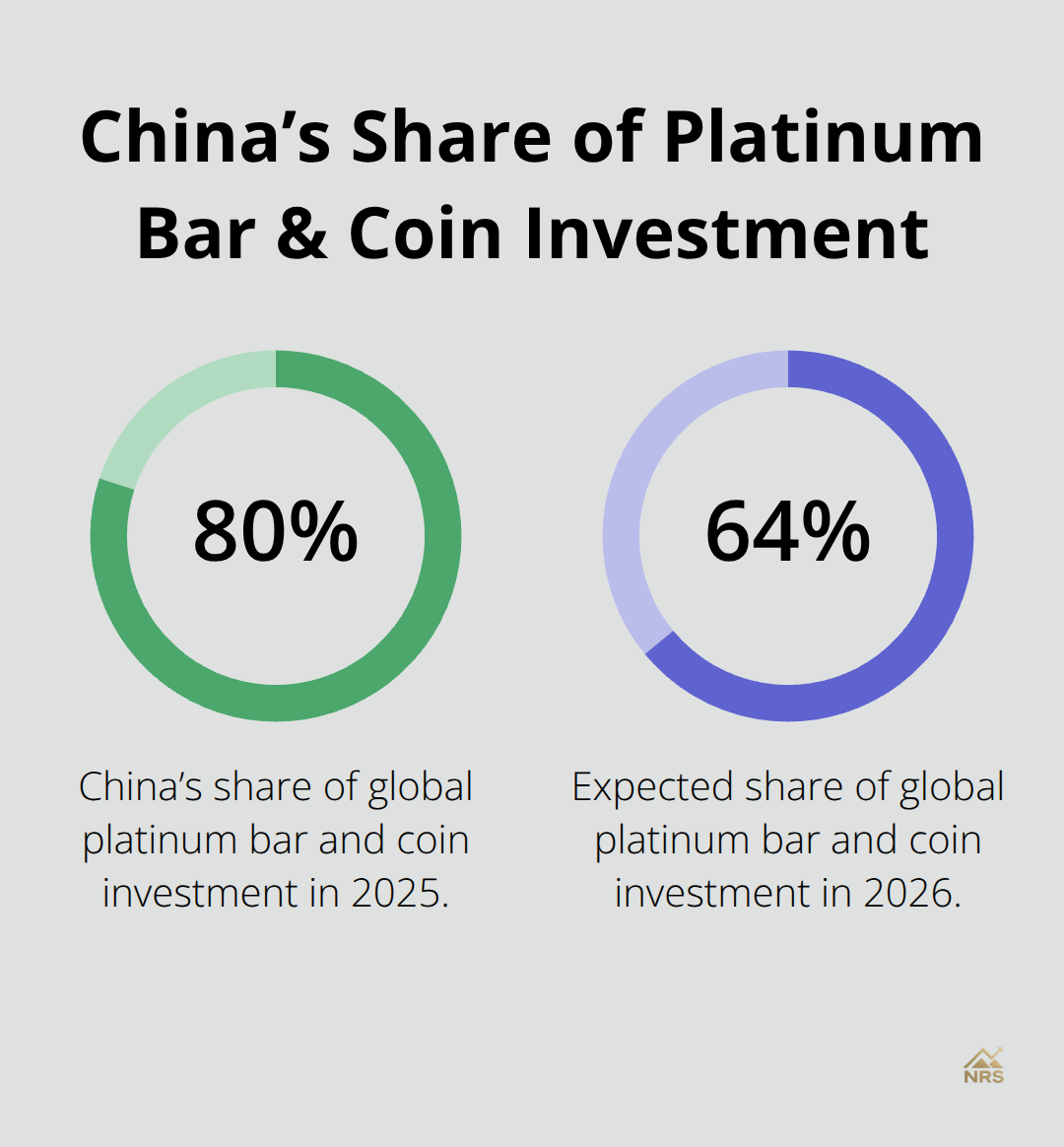

China became the largest market for platinum bar and coin investment in 2025, accounting for roughly 80% of that segment before moderating to an expected 64% share in 2026 as other markets grow. This geographic concentration in investment demand creates both opportunity and risk, as Chinese investor sentiment can amplify or dampen price moves. The reintroduction of platinum Panda coins by the People’s Bank of China signals official support for retail platinum accumulation, potentially sustaining investment flows even as Western markets remain cautious.

These supply constraints, demand shifts, and investment dynamics converge to create distinct opportunities for investors who understand where platinum sits in its market cycle. The next section examines how these factors translate into specific price drivers and the timing signals that separate profitable entry points from costly mistakes.

What Drives Platinum Prices

Platinum prices respond to four distinct forces that operate on different timescales, and understanding which one dominates at any moment separates profitable trades from costly guesses. Automotive demand sets the floor because catalytic converter manufacturing consumes 36-44% of annual platinum supply according to the World Platinum Investment Council. When vehicle production slows, platinum prices typically fall within weeks as fabricators reduce orders. The 2015 Volkswagen diesel scandal demonstrated this dynamic brutally: diesel vehicle sales collapsed, catalytic converter demand cratered, and platinum prices tumbled despite tight physical supply.

Why Automotive Demand No Longer Controls Prices

However, automotive demand alone cannot explain platinum’s current strength. Industrial applications including petroleum refining catalysts, nitric acid production for fertilizer manufacturing, and glassmaking represent 23-35% of consumption and follow different cycles than automotive. These sectors demand platinum regardless of recession risk because the chemical processes depend on platinum’s unique catalytic properties.

Jewelry consumption at 24-30% of demand provides the most stable anchor, particularly in the US engagement ring market and Japan where platinum holds generational preference. The critical insight: automotive weakness no longer dominates platinum’s price direction as it did a decade ago.

Supply Tightness Overrides Demand Weakness

The World Platinum Investment Council forecasts total platinum demand will fall 6% year-over-year in 2026, yet mine supply will grow only 2% while recycling increases 10% annually. This structural mismatch means supply tightness overrides demand weakness as the primary price driver. Geopolitical disruptions amplify this effect dramatically. South Africa accounts for roughly 70% of global platinum output, and aging infrastructure combined with power constraints have already reduced production capacity. Russia’s sanctions-related output declines remove another significant supply source permanently.

The platinum lease rate jumped from 1% in 2024 to 12% year-to-date in 2025 according to LBMA data, signaling that physical metal scarcity has become acute enough that dealers now pay substantially to borrow actual platinum rather than trade paper contracts. This lease rate behavior predicts price moves because it reflects real supply stress before spot prices adjust. Monitor lease rates as a leading indicator: when they exceed 5%, supply constraints are tightening faster than the market prices them in.

Hydrogen Technology and Chinese Investment Shape the Outlook

Hydrogen fuel cell technology represents platinum’s growth wildcard, though current demand contribution remains negligible. Proton exchange membrane electrolyzers use platinum catalysts to produce green hydrogen for power generation, industrial heating, steelmaking, and sustainable aviation fuels. As energy transition accelerates and hydrogen infrastructure expands, this application could offset automotive losses structurally. However, hydrogen demand remains nascent and won’t materially impact platinum consumption for at least 3-5 years.

Investment flows from China created the sharpest price volatility in 2025, with Chinese bar and coin demand accounting for approximately 80% of investment platinum before moderating to an expected 64% in 2026. The People’s Bank of China reintroduction of platinum Panda coins signals official encouragement for retail accumulation, potentially sustaining Chinese demand even as Western investors remain skeptical. This geographic concentration means platinum prices now correlate more closely with Chinese economic sentiment than Western recession fears.

Practical Positioning Requires Real-Time Monitoring

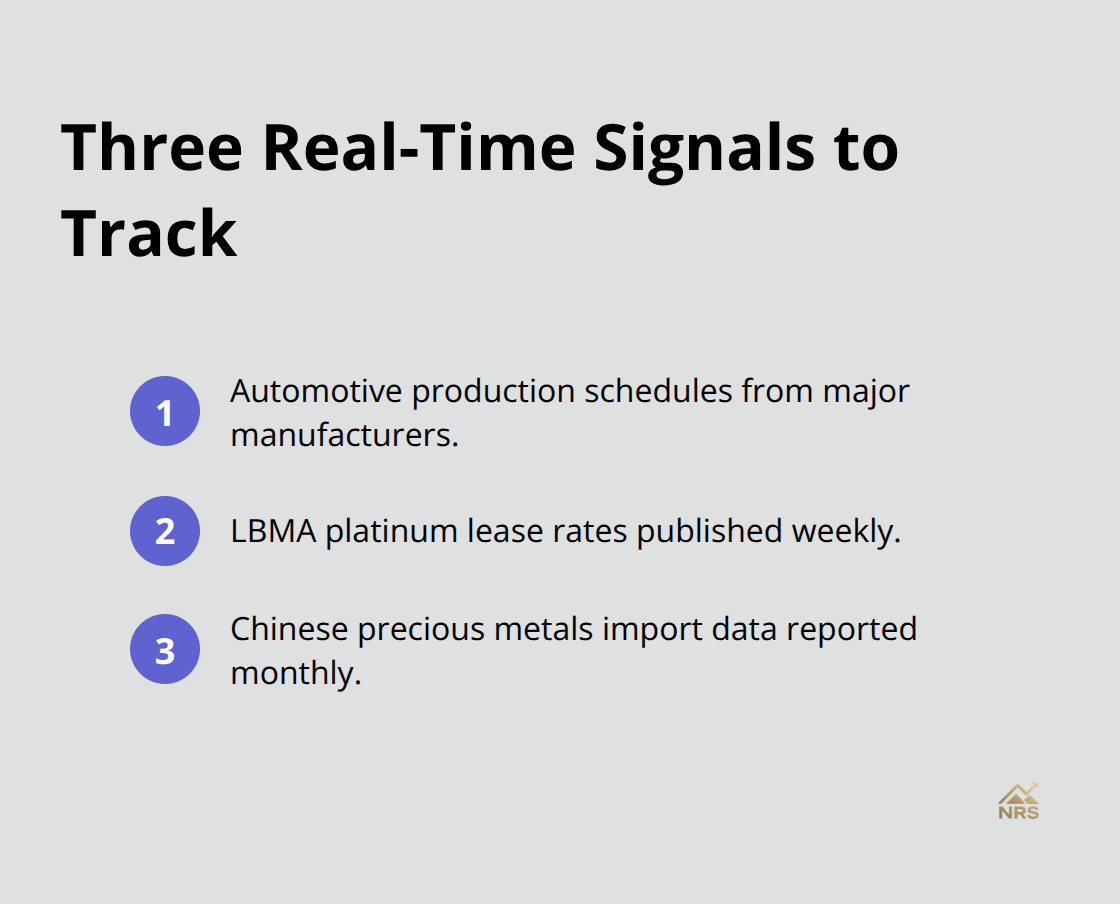

Track three data points simultaneously to position effectively: automotive production schedules from major manufacturers, LBMA lease rates published weekly, and Chinese precious metals imports reported monthly by Chinese customs. When automotive production falls while lease rates remain above 8% and Chinese imports continue growing, platinum becomes undervalued relative to supply fundamentals.

Conversely, if Chinese investment demand reverses while automotive production strengthens, supply tightness alone may not prevent price declines.

The World Platinum Investment Council projects prices around 2,425.92 USD per troy ounce within 12 months, but this assumes supply constraints persist and geopolitical tensions don’t escalate further. Weight supply scarcity more heavily than demand forecasts when making entry decisions. These price drivers set the stage for understanding where platinum sits within its broader market cycle and which investment vehicles offer the best risk-adjusted exposure to platinum’s structural supply deficit.

How to Position Platinum in Your Portfolio Right Now

Platinum’s structural supply deficit creates a narrow window for entry that closes as prices rise. The World Platinum Investment Council expects above-ground stocks to remain depleted through 2026 and beyond, meaning supply tightness will persist as the primary price driver. This isn’t speculative positioning based on sentiment swings; it’s capital deployment into a market where supply cannot match demand structurally. When supply cannot match demand structurally, prices move higher over time. Current entry levels near 2,027.60 USD per troy ounce on April 27, 2026 offer reasonable risk-reward for investors willing to hold through near-term volatility.

Access Platinum Without Retail Premiums

The platinum lease rate confirms that physical scarcity has become acute enough to reward patient capital. However, retail coin and bar purchases cost investors 6% to 47% in premiums and VAT according to BullionVault research. Instead, access wholesale platinum through vaulted storage starting from just 1 gram at live market prices published by the London Bullion Market Association. This approach eliminates the buy-back liquidity problems that plague physical coins and removes VAT charges when metal remains in professional vault storage under LPPM standards. You can trade 24/7 in USD, EUR, or GBP without forex fees.

Physical ETFs offer another practical route for investors seeking exposure without storage logistics. Monitor fund flows closely since Chinese investment demand accounted for a significant share of platinum bar and coin investment before moderating in 2026. When Chinese flows reverse, ETF outflows can accelerate quickly and pressure prices temporarily.

Position Platinum as an Inflation and Supply-Chain Hedge

Hydrogen fuel cell technology represents platinum’s true diversification edge within a resource portfolio, though the timeline for material demand contribution stretches 3-5 years minimum. Proton exchange membrane electrolyzers power green hydrogen production for steelmaking, sustainable aviation fuels, and industrial heating. This application will eventually offset automotive catalytic converter losses as electrification advances. Platinum transforms from a pure cyclical commodity dependent on automotive production into a structural growth story tied to energy transition.

Position platinum as your hedge against both inflation and supply-chain fragmentation rather than a traditional precious metal bet on central bank monetary policy. The concentration of production in South Africa and Russia creates permanent supply risk that central banks cannot solve through policy adjustments alone.

Monitor Real-Time Signals for Entry Timing

Diversification within platinum itself matters operationally: combine physical holdings in professional vault storage with ETF exposure to capture both stable long-term accumulation and tactical trading opportunities. Track LBMA lease rates weekly and Chinese customs data monthly for import trends. When lease rates exceed 8% while Chinese imports remain strong, platinum’s risk-reward tilts decisively toward accumulation.

Trading Economics projects platinum could reach higher levels by quarter-end 2026, but this assumes supply constraints ease moderately. Geopolitical escalation or further South African production disruptions could easily push prices higher within months, creating capital gains that dwarf typical resource stock returns.

Final Thoughts

Platinum market trends reveal a commodity fundamentally reshaped by supply scarcity rather than demand cycles. The structural deficit persisting through 2026 and beyond creates a rare opportunity: a market where physical supply cannot match consumption regardless of economic conditions. South Africa’s aging mines and Russia’s sanctions-related output declines have created a permanent supply constraint that prices must eventually reflect, with above-ground stocks depleted to five months of demand cover removing the inventory buffer that historically stabilized prices during downturns.

The long-term investment case rests on three pillars that transform platinum from a pure cyclical bet into a supply-constrained asset with multiple demand anchors. Automotive demand will remain substantial for years despite electrification, with diesel and gasoline engines persisting through increasing hybridization, while industrial applications in petroleum refining, fertilizer production, and glassmaking provide stable consumption independent of recession cycles. Hydrogen fuel cell technology represents genuine structural growth (though material demand contribution requires 3-5 years minimum), offsetting automotive losses as energy transition accelerates.

We at Natural Resource Stocks believe platinum deserves a meaningful allocation within resource portfolios precisely because supply tightness persists while most investors remain skeptical. Current entry levels near 2,027.60 USD per troy ounce offer reasonable risk-reward for capital deployed into structural scarcity, and the World Platinum Investment Council projects prices around 2,425.92 USD per troy ounce within 12 months. Monitor LBMA lease rates and Chinese import data monthly to confirm supply constraints remain active, then explore resource investment strategies for expert analysis on metals, energy, and macroeconomic factors shaping commodity markets.