Nuclear energy is experiencing a genuine resurgence. Governments worldwide are backing atomic power as a climate solution, and uranium demand is climbing to match.

At Natural Resource Stocks, we’re tracking how these policy shifts are reshaping the uranium mining stocks outlook. This guide shows you where the real opportunities lie.

Where Uranium Demand Stands Today

The Structural Shift in Global Nuclear Policy

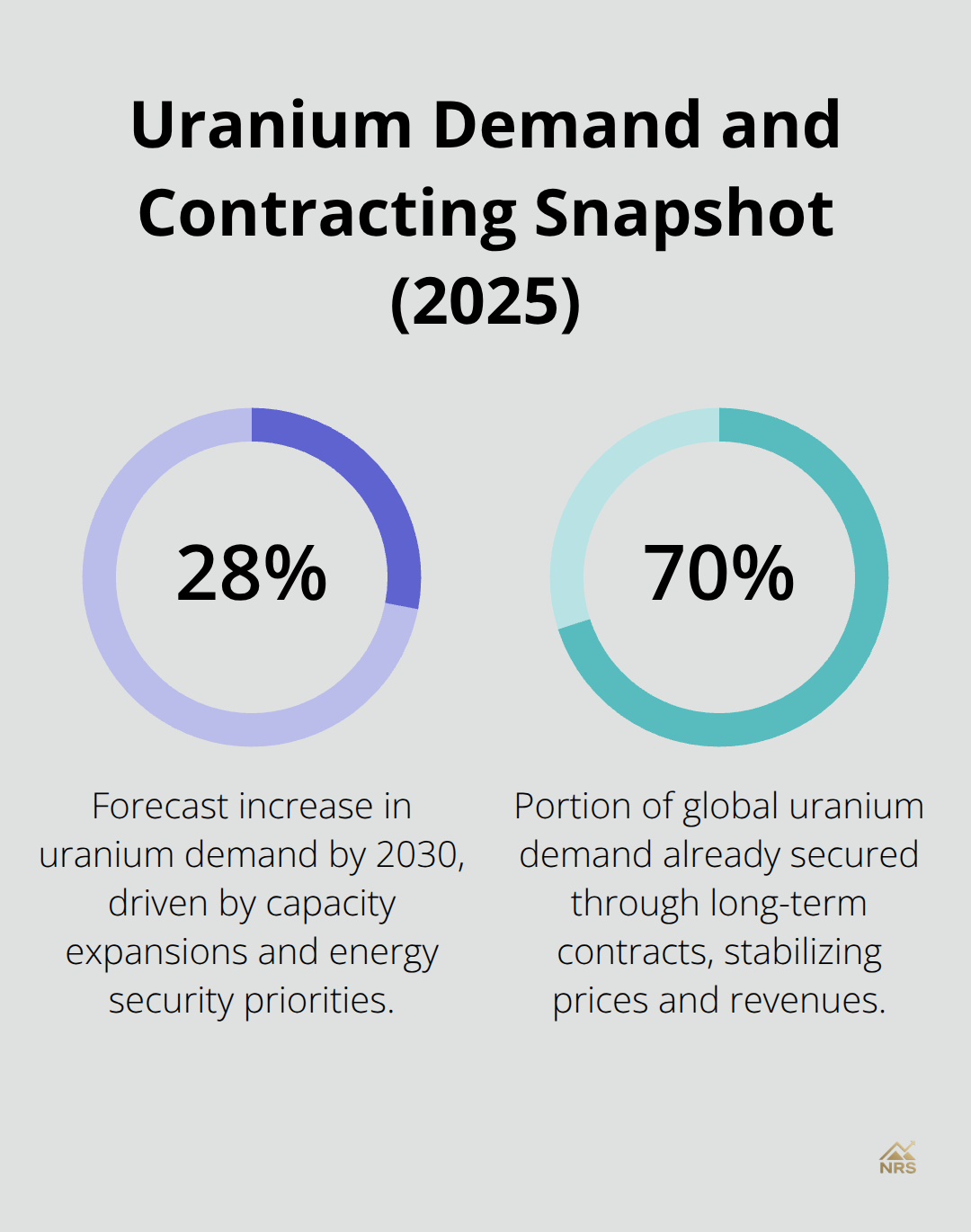

Uranium demand will rise 28% by 2030 according to current market forecasts, driven by nuclear capacity expansions and energy security needs across North America, Europe, and Asia. More than 69 reactors under construction globally create immediate demand pressure, and governments committed real capital to nuclear infrastructure. The World Bank reversed its nuclear financing ban in June 2025 and partnered with the IAEA to extend reactor fleet life, removing a major barrier to investment. China signals substantial growth in nuclear capacity toward 2040, while the Czech Republic pursues an $18 billion nuclear plant with South Korea, the UK allocated £14.2 billion to Sizewell C, and Belgium abandoned its nuclear phaseout entirely. These announcements represent a structural shift in global energy policy that directly translates to sustained uranium consumption.

Approximately 70% of global uranium demand is already secured through long-term contracts, which stabilizes prices and gives miners predictable revenue streams.

The Contracting Gap and Price Dynamics

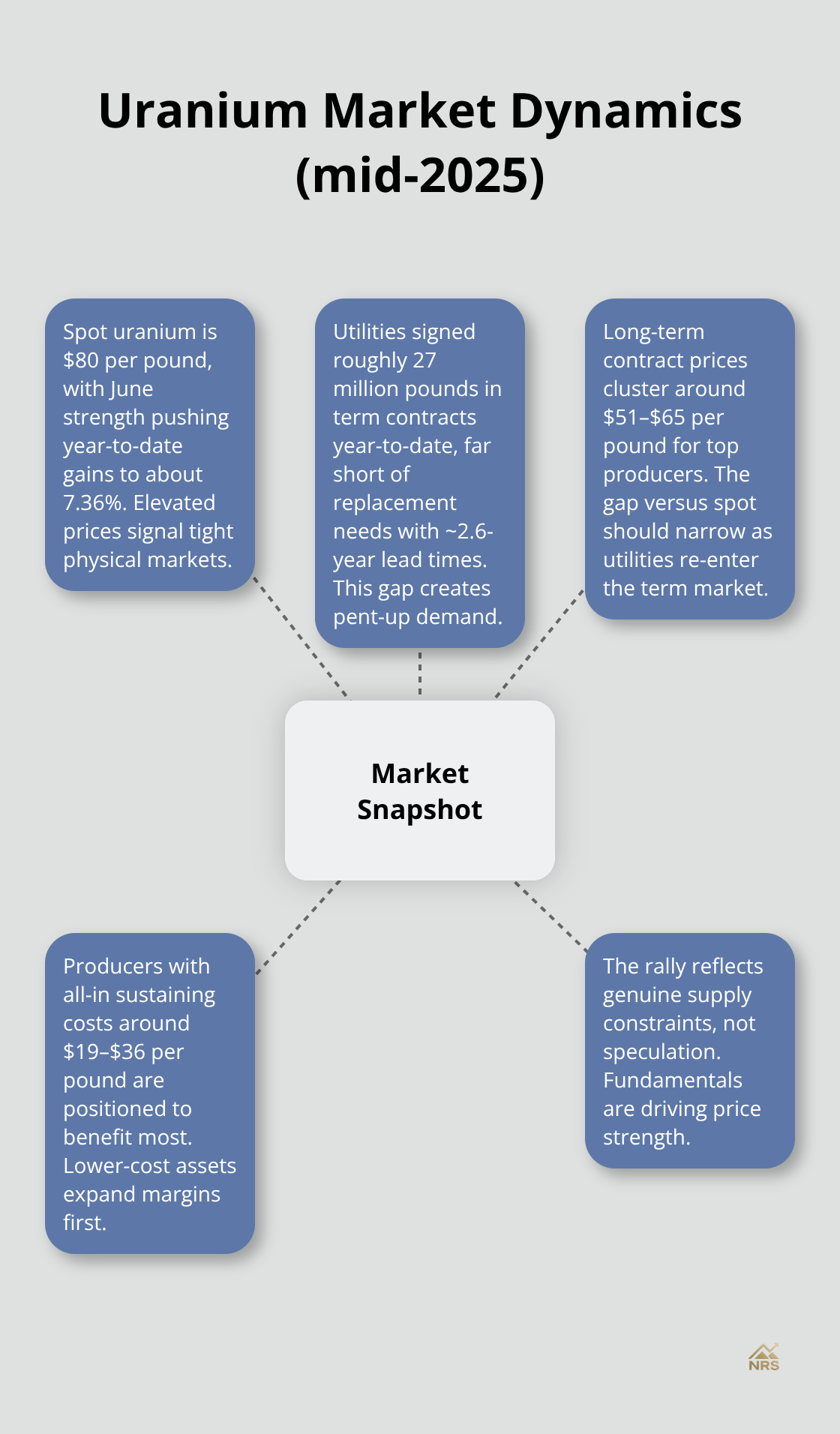

Utilities signed roughly 27 million pounds in term contracts year-to-date in 2025, but this falls far short of replacement needs given term-lead times around 2.6 years. This gap creates significant pent-up demand ahead. Spot uranium reached $80 per pound as of mid-2025, with June strength contributing year-to-date gains of approximately 7.36%. This rally reflects real supply constraints rather than speculation.

Long-term contract prices typically range from $51 to $65 per pound for top producers, while spot prices now sit at $80, creating a pricing gap that utilities will eventually close through new contracting. This dynamic favors producers with robust reserve bases and low all-in sustaining costs around $19 to $36 per pound depending on their asset mix and geographic footprint.

Supply Concentration and Market Tightness

Kazatomprom leads global production at roughly 23,000 tonnes of U3O8 annually, followed by Cameco at approximately 18,000 tonnes, but this combined output still falls short of rising demand. Kazakhstan’s production cuts remove 7 to 10 million pounds from global supply, tightening markets quickly. The Northshore Global Uranium Mining Index jumped 18.19% in June alone, while junior uranium miners rose 17.94%, signaling strong institutional capital inflows into the sector.

Evaluating Producer Fundamentals

Cameco trades near $14.5 billion in market cap with roughly 28 years of reserve life and an all-in sustaining cost near $32 per pound. Kazatomprom sits around $12.8 billion with 24 years of reserve life and an AISC near $19 per pound, making it the lowest-cost major producer but carrying Kazakhstan geopolitical risk. Orano operates at approximately $6.2 billion in market cap with 22 years of reserve life and costs around $36 per pound, but faces African project stability concerns.

What to Prioritize in Your Analysis

Focus first on all-in sustaining cost per pound-this metric reveals which producers will remain profitable during price downturns and which will struggle. Second, examine reserve life and geographic diversification. Producers with assets across Canada, Australia, and the United States face fewer concentrated geopolitical risks than those dependent on single jurisdictions. Third, assess contract exposure: firms with heavier long-term contract exposure enjoy steadier cash flow, while spot-heavy producers capture more upside during rallies but face sharper downside during weakness. Finally, validate reported reserves independently and monitor ESG practices closely, as regulatory delays and licensing issues increasingly impact project timelines in developed mining jurisdictions. These fundamentals will shape which uranium stocks outperform as utilities move to lock in supply over the next two to three years.

How Policy Shifts Are Reshaping Uranium Economics

The Structural Reversal in Global Nuclear Financing

The nuclear policy environment shifted decisively in 2025, and uranium producers now capitalize on concrete government commitments rather than vague climate promises. The World Bank reversed its nuclear financing ban in June 2025 and partnered with the IAEA to extend reactor fleet life, removing a structural barrier that had constrained uranium investment for years. This action opened public financing channels for nuclear projects globally. Simultaneously, the Trump administration issued executive orders targeting accelerated deployment of new nuclear reactor technologies and expansion of American nuclear energy capacity, with accelerated permit reviews compressed to 18 months and licensing reforms that reshape uranium demand fundamentally. If enacted, these reforms lift U.S. uranium requirements from roughly 50 million pounds annually to approximately 200 million pounds, effectively doubling global mine output demand.

Policy Momentum Across Major Economies

New York’s commitment to a 1 GW nuclear plant specifically to power AI data centers signals state-level momentum beyond federal initiatives. The Czech Republic pursues an $18 billion nuclear project with South Korea, the UK allocated £14.2 billion to Sizewell C, and Belgium abandoned its nuclear phaseout entirely. These announcements represent coordinated European momentum toward atomic energy, not isolated policy experiments. Each commitment translates directly into fuel procurement timelines and long-term contracting activity that uranium producers can forecast with reasonable confidence.

The Contracting Acceleration Ahead

Utility contracting will accelerate sharply in 2025 and 2026 as these policy signals translate into actual reactor construction and fuel procurement. Producers with long-term contract exposure locked in at $55 to $62 per pound will see margin expansion as spot prices remain elevated near $80 per pound. The real opportunity lies with junior explorers and mid-tier producers positioned to supply new demand tranches. Companies with low all-in sustaining costs around $19 to $32 per pound will capture outsized returns if uranium prices remain above $70 per pound for the next five years, which current policy trajectories make increasingly likely.

Timing the Contracting Window

The contracting gap we identified earlier-with only 27 million pounds signed year-to-date against replacement needs requiring significantly more-will compress rapidly as utilities execute 2.6-year lead-time contracts ahead of reactor startups. Monitor the World Nuclear Association’s September demand forecast closely; if revised upward to reflect policy acceleration, term activity will spike immediately. This creates a narrow window to position in producers with proven reserve bases and execution capability before institutional capital fully prices in the structural uranium deficit that policy has now crystallized. The next section examines which specific producers offer the strongest fundamentals to capture this opportunity.

Which Uranium Producers Offer Real Upside Right Now

The Major Producers: Stability Over Growth

Cameco trades at roughly $14.5 billion in market cap with 28 years of reserve life and all-in sustaining costs near $32 per pound. The company locks in contract prices between $55 and $62 per pound while spot uranium trades at $80, creating immediate margin compression risk if long-term contracts roll off without renewal at higher prices. This positions Cameco as a stable cash generator rather than an explosive growth story. Kazatomprom sits around $12.8 billion with the lowest AISC among major producers at $19 per pound and 24 years of reserve life, but Kazakhstan’s geopolitical exposure makes it unsuitable for risk-averse investors given recent supply cut announcements. Orano operates at $6.2 billion in market cap with acceptable fundamentals, yet its heavy African project exposure creates regulatory and execution risk that investors rarely price in adequately.

Mid-Tier Producers: Where Real Opportunity Lies

The real opportunity lies with mid-tier and junior producers positioned to capture incremental demand as utilities accelerate contracting over the next 24 months. Energy Fuels trades around $1.5 to $2.1 billion and produces roughly 1,000 tonnes of U3O8 annually with US-focused diversification that positions it as a domestic supply solution if North American uranium requirements genuinely double as policy suggests. Paladin Energy operates at approximately $1.8 billion in market cap with production around 1,800 tonnes annually and is restarting its Langer Heinrich mine in Namibia, offering production growth without the geopolitical baggage of Kazakhstan. Denison Mines trades near $0.9 to $1.2 billion and controls high-grade Athabasca Basin assets in Canada with reserve life exceeding 30 years, making it a pure-play on Canadian uranium expansion if licensing accelerates.

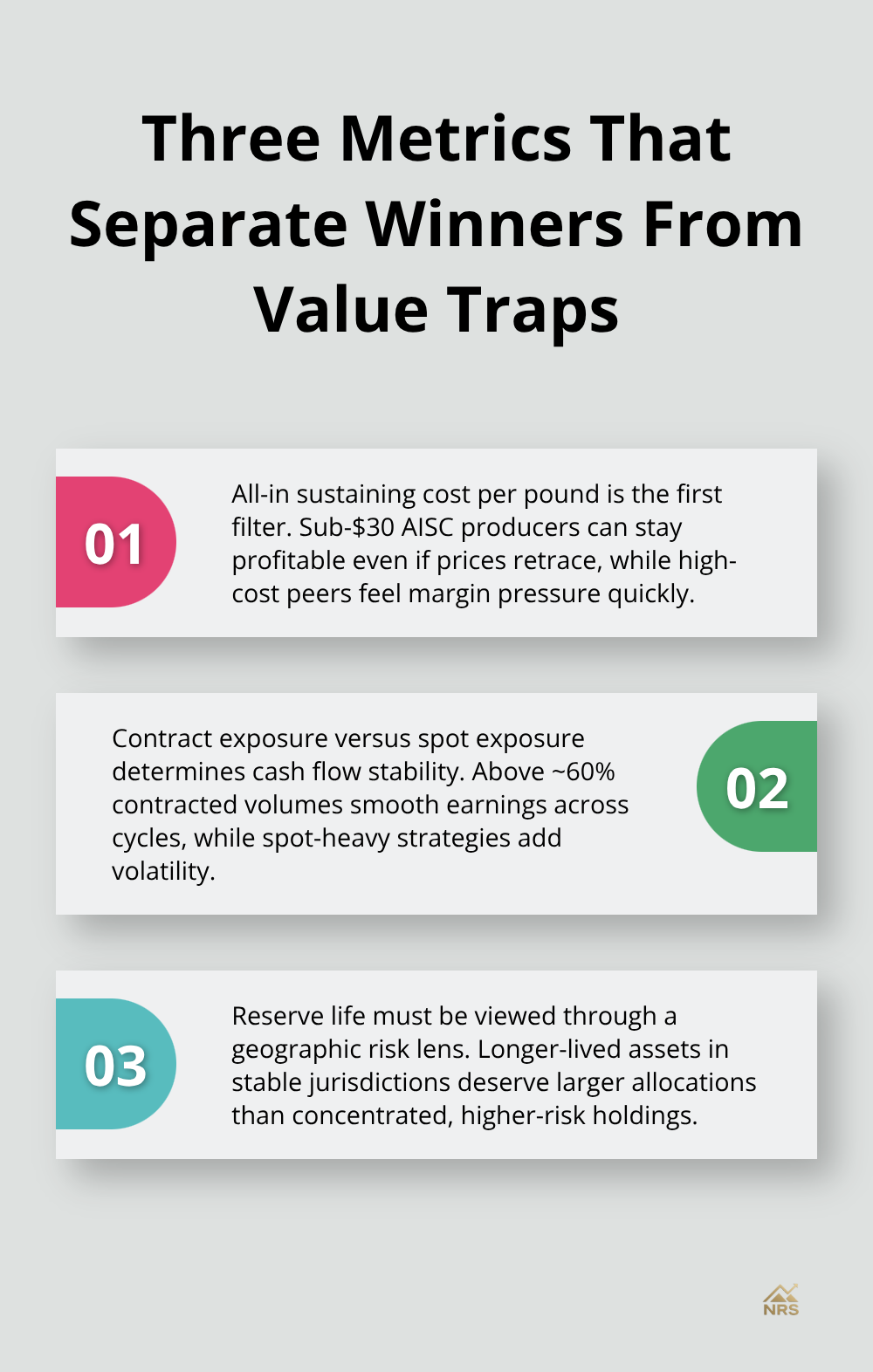

Three Metrics That Separate Winners From Value Traps

Compare these producers directly on three metrics that matter: all-in sustaining cost per pound, contract exposure versus spot exposure, and reserve life adjusted for geographic risk. Producers with AISC below $30 per pound remain profitable even if uranium crashes to $50, while those above $35 face margin pressure quickly. Contract exposure above 60 percent of annual production provides cash flow stability through price cycles, while spot-heavy producers capture upside but suffer outsized losses during corrections. This matters because execution risk separates winners from value traps in uranium mining.

Operational Edges and Regulatory Advantages

Denison’s in-situ recovery technology deployment in Canada deserves scrutiny because ISR cuts environmental impact and regulatory approval timelines compared to conventional mining, yet most investors overlook this operational edge. Monitor ESG practices intensely because regulatory delays now routinely extend project timelines by two to three years in developed jurisdictions. Companies that publish robust sustainability reporting, carbon footprints, and traceability frameworks face fewer approval delays than those that treat compliance as an afterthought. Ignore feasibility studies commissioned by the companies themselves and instead validate project pipelines through independent assessment.

Portfolio Construction for Uranium Exposure

For portfolio positioning, avoid concentrating capital in Cameco or Kazatomprom despite their size; instead, build a core position in one mid-tier producer with proven reserve base and low AISC, then add selective exposure to junior explorers with high-grade assets and realistic funding paths. This structure captures the structural uranium deficit while limiting single-company execution risk. Size positions inversely to reserve life: smaller positions in companies with 20-year reserves make sense, while larger allocations fit companies with 30-plus year reserve bases. Test your thesis across multiple uranium price scenarios spanning $50 to $100 per pound over a five-year horizon, calculating free cash flow and dividend sustainability under each case. Companies with positive cash flow above $60 per pound offer margin of safety that those dependent on $80-plus prices do not provide.

Final Thoughts

The uranium mining stocks outlook has fundamentally shifted due to policy reversals from the World Bank, accelerated nuclear licensing in the United States, and coordinated European momentum toward atomic energy. These developments have crystallized a structural uranium deficit that will persist for years, with utilities facing a contracting gap of roughly 27 million pounds year-to-date against replacement needs and 2.6-year lead times that compress rapidly as reactor construction accelerates. This narrow window allows producers with proven reserve bases and low all-in sustaining costs to capture outsized returns before institutional capital fully prices in the supply tightness that policy has now guaranteed.

The real opportunity lies not with mega-cap producers like Cameco or Kazatomprom, but with mid-tier and junior explorers positioned to supply incremental demand over the next 24 months. Energy Fuels offers domestic supply exposure, Paladin Energy brings production growth through mine restarts, and Denison Mines controls high-grade Canadian assets with superior regulatory positioning. Focus your analysis on three metrics: all-in sustaining cost per pound below $30, contract exposure above 60 percent of annual production, and reserve life adjusted for geographic risk.

Monitor the World Nuclear Association’s September demand forecast closely, as an upward revision will spike term activity immediately and reprice valuations sharply. Watch for utility contracting announcements and track geopolitical developments in Kazakhstan and Niger, where supply concentration creates execution risk. We at Natural Resource Stocks track these catalysts continuously through expert analysis and market commentary, helping you position your portfolio before the structural uranium deficit becomes consensus and prices reflect the full magnitude of policy-driven demand growth ahead.