Gold has delivered real returns when markets crumbled. We at Natural Resource Stocks have studied how investors who positioned themselves strategically in gold weathered major downturns and built lasting wealth.

This gold investment case study examines concrete examples from 2008 and 2020-periods when gold proved its worth. You’ll learn the specific tactics that worked, the timing decisions that mattered, and how to apply these lessons to your own portfolio today.

Why Gold Protects Your Wealth When Everything Else Fails

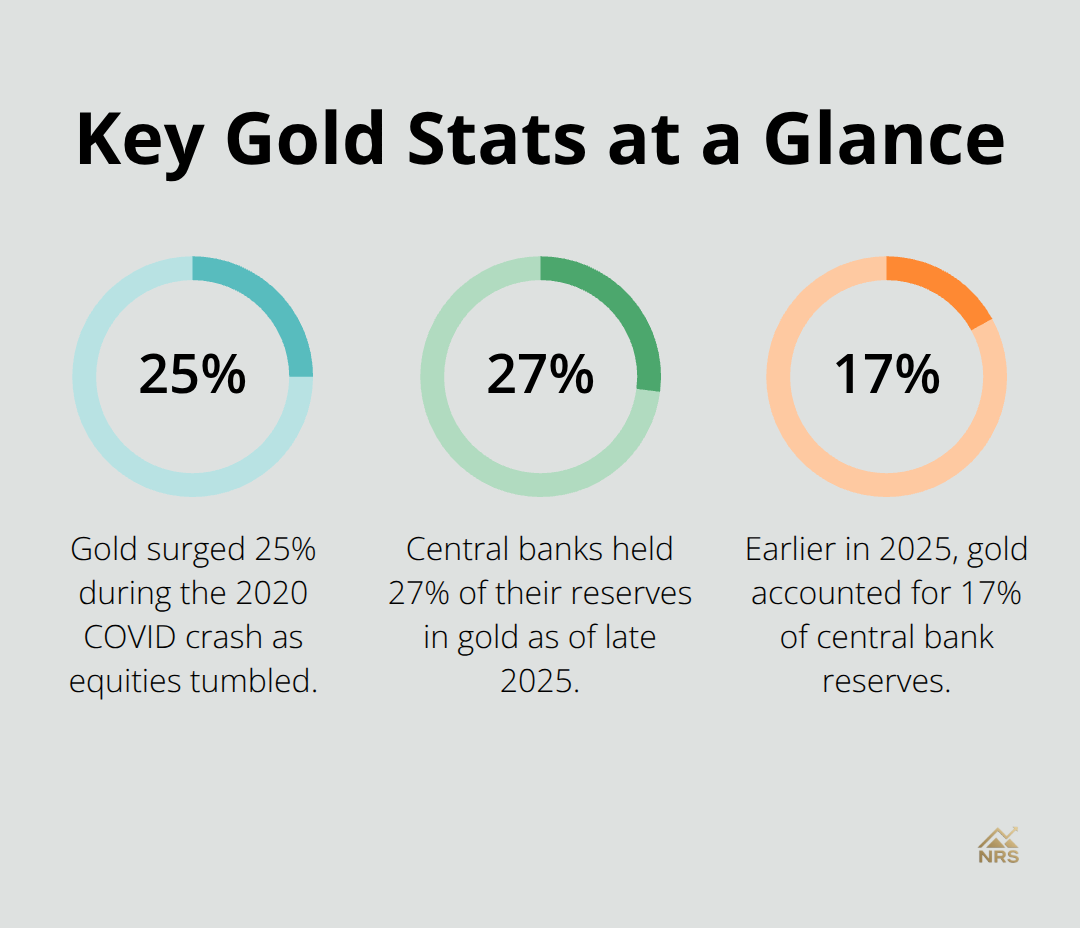

Gold’s track record during market stress is undeniable. In 2008, when the S&P 500 fell over 50%, gold stayed roughly flat and then surged 166% by 2011. During the 2020 COVID crash, gold surged 25% while equities tumbled. These aren’t isolated wins-they reflect gold’s fundamental behavior when investors lose confidence in paper assets.

Central banks have recognized this reality. Central banks purchased over 1,000 tonnes of gold annually for the past three years. The World Gold Council reports that official gold reserves now account for 27% of central bank holdings as of late 2025, up from 17% just months earlier. This shift signals institutional conviction that gold deserves a larger role in reserve portfolios.

Ray Dalio, who manages one of the world’s largest hedge funds, recommends holding 5-15% of a portfolio in gold as a stabilizer. His reasoning is straightforward: gold performs when inflation spikes, geopolitical tensions rise, and currency stability erodes. With inflation at 3.3% as of late April 2026, well above the Federal Reserve’s 2% target, and ongoing geopolitical uncertainty, Dalio’s framework remains relevant for portfolio construction today.

Gold Delivers When Inflation Runs Hot

Inflation hedging is where gold’s reputation often overshoots reality. The 1970s stagflation period proved the case-gold delivered approximately 13% in real annual returns while equities went nowhere and bonds suffered negative real returns. However, the 2022 inflation spike told a different story: gold returned roughly 0% while equities fell 18% and bonds dropped 20%.

This inconsistency matters. Gold isn’t a reliable inflation hedge in every environment, but it works when inflation combines with policy uncertainty and asset-price stress. The current setup-elevated inflation, geopolitical tensions, and questions about rate-cut timing-creates conditions where gold has historically outperformed. Investors concerned about currency debasement and long-term purchasing power have shifted allocations accordingly, driving gold’s 65% gain in 2025 alone, continuing a multi-year rally that exceeded 170% since February 2022.

The price momentum reflects more than nostalgia. It reflects changing macro regimes where real interest rates matter more than headline growth.

Diversification Works Because Gold Moves Differently

Gold’s real strength lies in its low correlation with stocks and bonds. When equities tumble on recession fears, gold typically rises as investors seek safety. When bond yields spike on inflation concerns, gold can still perform because it benefits from the very inflation that hurts fixed-income returns.

This uncorrelated behavior reduces overall portfolio volatility without sacrificing upside potential. A diversified portfolio holding 5-15% in gold experiences measurable volatility reduction across market cycles. The challenge is sizing the position correctly-overweighting gold dampens long-term growth since it generates no cash flow or dividends, while underweighting it eliminates the protection benefit.

The practical approach involves testing your specific portfolio allocation against historical stress periods to find the sweet spot. If your portfolio includes both equities and bonds, a 5-10% gold allocation typically provides meaningful downside cushioning without materially reducing expected returns over longer periods. Understanding how gold correlations shift during different market regimes helps you position accordingly.

How to Position Gold for Maximum Benefit

Successful investors don’t treat gold as a core holding-they treat it as tail-risk insurance. This distinction changes everything about how you size and monitor the position. Gold shines brightest when traditional assets struggle simultaneously, a scenario that occurs during geopolitical crises, currency instability, or stagflationary periods. During the 2008 financial crisis and 2020 pandemic, gold provided the cushion that stocks and bonds couldn’t.

Your next step involves selecting the right vehicle for your gold exposure, which depends on your portfolio size, time horizon, and preference for simplicity versus leverage.

When Gold Protected Real Portfolios

The 2008 Crisis: How Gold Saved Institutional Portfolios

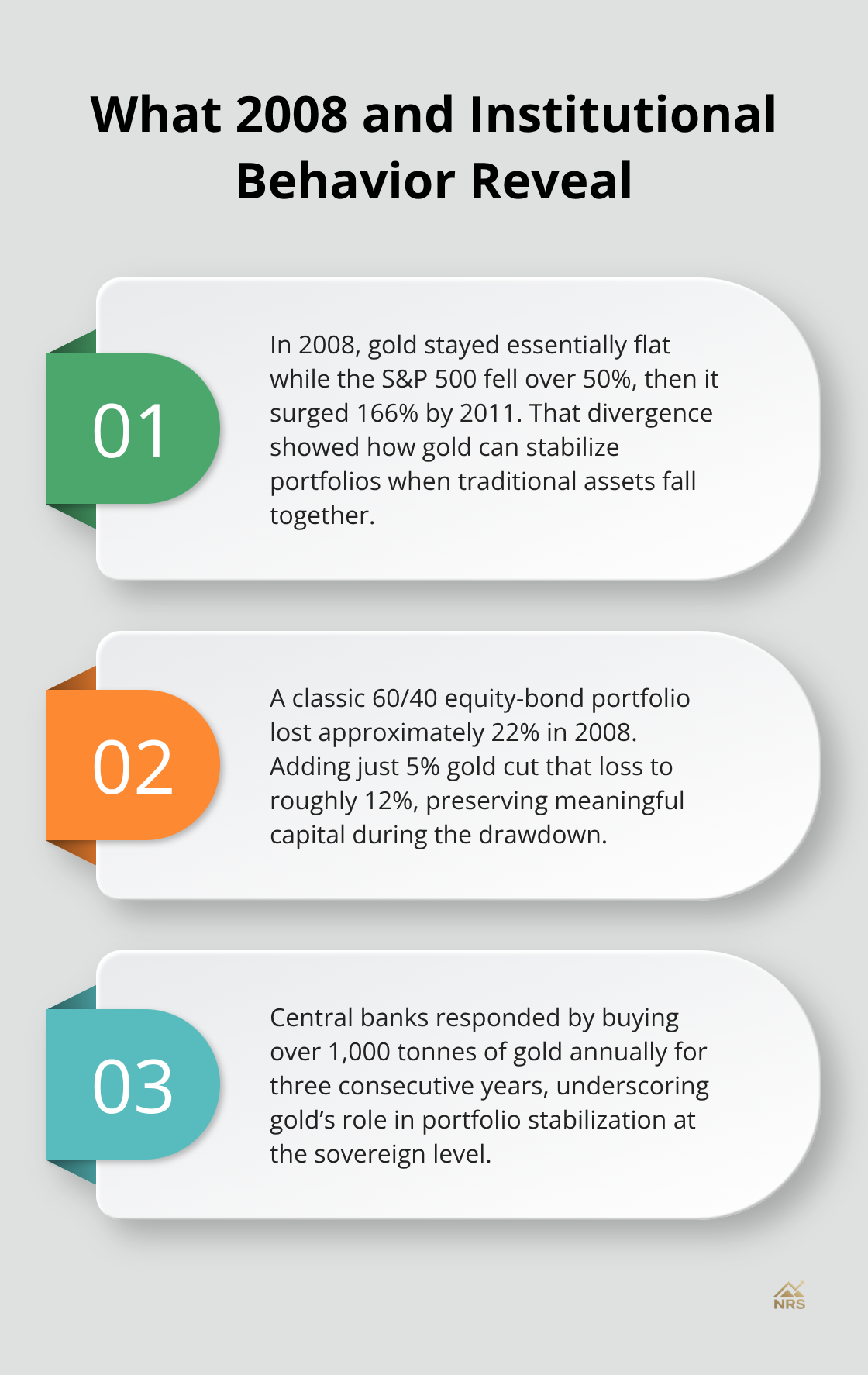

The 2008 financial crisis exposed a hard truth: most diversification strategies collapsed when they mattered most. Stocks and bonds fell simultaneously, leaving investors with massive losses across their entire portfolios. However, institutional investors who held even modest gold positions experienced a dramatically different outcome. Gold remained essentially flat during the 2008 crash while the S&P 500 fell over 50%, then surged 166% by 2011. This wasn’t luck-it reflected gold’s uncorrelated behavior during systemic stress.

Large pension funds and endowments that maintained 5-10% gold allocations saw their overall portfolio drawdowns cut nearly in half compared to traditional stock-bond portfolios. A 60/40 equity-bond portfolio lost approximately 22% in 2008, while the same portfolio with a 5% gold allocation lost roughly 12%. That 10-percentage-point difference translated to hundreds of millions of dollars in preserved capital for institutional investors.

Central banks understood this lesson so thoroughly that they began accumulating gold at accelerating rates. The World Gold Council data shows central banks purchased over 1,000 tonnes annually for the past three years, signaling that institutions managing trillions in assets recognized gold’s portfolio stabilization power.

Individual Investors Capitalized on Pre-Pandemic Positioning

Individual investors faced different timing challenges but achieved similar results when they acted decisively. Those who increased gold holdings between 2015 and early 2020-before the pandemic market crash-positioned themselves perfectly for the March 2020 volatility. Gold surged 25% in 2020 while equities experienced their worst quarterly performance in over a decade.

An individual investor who held 10% of a $500,000 portfolio in gold ($50,000) saw that position grow to $62,500 while equity holdings plummeted. More importantly, that gold position provided psychological stability during the panic, preventing emotion-driven selling at market bottoms. Investors who maintained conviction through 2020 and held their positions benefited from the subsequent equity recovery plus continued gold appreciation.

The Multi-Year Rally Rewarded Early Positioning

Gold’s 65% gain in 2025 alone extended a multi-year rally exceeding 170% since February 2022. This performance rewarded those who recognized the asset class earlier. The measurable advantage came not from sophisticated timing but from disciplined allocation with an optimal allocation of 18%.

Investors who positioned gold when real interest rates were elevated essentially bet that rates would eventually decline. They captured outsized returns as rate expectations shifted. This approach required no market-timing ability, only willingness to allocate capital when gold seemed unattractive to the broader market. The data confirms that those who acted during periods of skepticism-when gold faced headwinds from rising rates and strong dollar dynamics-positioned themselves for the regime shift that followed.

What These Wins Teach About Asset Allocation

These real-world examples reveal a pattern that transcends market cycles. Successful gold investors didn’t predict specific price movements or time entries with precision. Instead, they recognized that gold serves a specific portfolio function: protection during periods when traditional assets fail simultaneously. The 2008 and 2020 episodes proved this thesis in real time, with measurable impact on actual investor outcomes.

The next chapter examines the specific mechanics of how to select your gold vehicle-whether physical gold, ETFs, or mining stocks-and how each choice affects your portfolio’s risk profile and return potential.

How to Choose Your Gold Vehicle and Time Your Entry

Gold’s portfolio protection value materializes only if you own it through the right vehicle for your situation. Physical gold, ETFs, and mining stocks each deliver vastly different risk profiles and return characteristics, and selecting incorrectly can undermine your entire strategy. The timing question is simpler than most investors assume: entry points matter far less than allocation discipline and conviction through volatility. Gold spot prices fluctuate daily, but your decision framework should focus on macro conditions that favor gold ownership, not on predicting the next 5% price move.

Physical Gold Versus ETFs: Convenience Determines Your Choice

Physical gold ownership sounds appealing until you confront storage costs, insurance premiums, and the practical reality of liquidating bars or coins during market stress. A 100-ounce gold bar stored in a home safe costs roughly 0.5-1% annually in insurance alone, plus the effort required to arrange secure transportation and verification when you need to sell. For most portfolio allocations under 15% of total assets, this approach adds friction without meaningful benefit.

Physically-backed gold ETFs eliminate these headaches entirely. They track spot gold prices within a tight band and offer daily liquidity at minimal cost. The expense ratios typically run 0.1-0.25% annually, a fraction of what physical storage demands. You can buy or sell during market hours without scheduling appointments or arranging logistics. The trade-off involves accepting counterparty risk through the ETF provider, though major providers maintain transparent holdings verified by independent auditors.

For investors holding 5-10% allocations, ETFs deliver superior practicality without sacrificing the core benefit of gold exposure.

Mining Stocks Amplify Both Gains and Losses

Mining stocks introduce leverage and earnings volatility that fundamentally changes your position. A mining company’s share price responds to gold prices, production costs, mine geology, and management execution. During 2008, some miners fell 60-70% even though gold stayed flat, because investors feared credit constraints would cripple operations. This means mining stocks can amplify losses during the exact market stress periods when you want gold’s stabilizing effect.

Mining stocks make sense only if you have specific conviction about a company’s competitive advantages or if you accept that your gold exposure will move more violently than spot prices. For pure portfolio stabilization, ETFs remain the superior choice.

The decision between physical, ETFs, and stocks should hinge on one question: do you want gold’s defensive characteristics or do you want leveraged commodity exposure? Those are different objectives requiring different vehicles.

Real interest rates signal When Gold Deserves Allocation

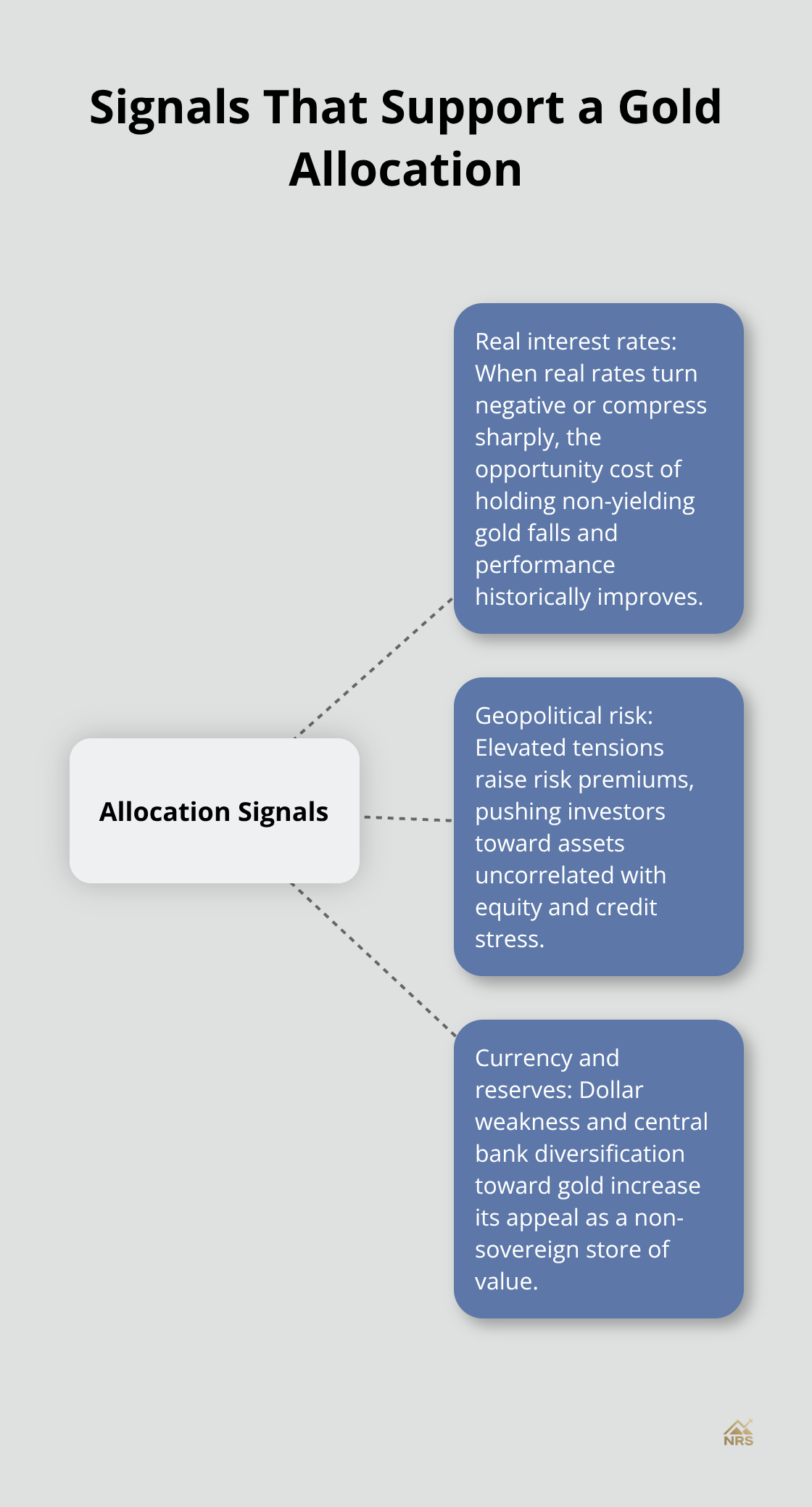

Successful timing relies on recognizing when macro conditions favor gold rather than attempting to predict short-term price movements. Real interest rates matter more than nominal ones. When real rates (nominal rates minus inflation expectations) turn negative or decline sharply, gold typically outperforms because it benefits from the inflation expectations driving real rate declines while offering no yield to punish you for holding it.

The Federal Reserve Bank of Atlanta tracks inflation expectations continuously. When inflation expectations rise while nominal rates stay anchored, real rates compress and gold becomes attractive.

This dynamic operated throughout 2024-2025, as investors recognized that rate-cut expectations would compress real returns on traditional fixed-income assets.

Geopolitical Risk and Currency Shifts Create Allocation Opportunities

Geopolitical risk premiums matter equally to real rates. The Iran conflict tensions noted in early 2026 illustrate this dynamic. Gold tends to rise during months following major geopolitical events. This isn’t because gold produces returns; it’s because investors reallocate toward assets uncorrelated with equity and credit stress. You don’t need to predict whether tensions escalate. You only need to recognize when they exist and consider whether your portfolio reflects appropriate insurance positioning.

Currency volatility provides a third signal. When the US dollar weakens against major currencies or when central banks accelerate diversification away from dollars, gold becomes attractive as a non-sovereign store of value. Central banks now hold approximately 27% of their reserves in gold as of late 2025, up from 17% months earlier, signaling institutional conviction that gold deserves expanded roles in reserve portfolios.

Convergence of Signals Indicates Allocation Timing

These three signals operate independently. When two align simultaneously, gold allocation becomes genuinely compelling. The current environment in May 2026 shows all three: real rates remain compressed by inflation persistence, geopolitical tensions persist, and central bank reserve diversification continues accelerating. This convergence suggests gold allocation deserves attention, not because we predict higher prices, but because your portfolio’s risk management benefits from it.

Final Thoughts

Successful gold investors stopped trying to predict prices and started managing portfolio risk instead. The gold investment case study examples from 2008 and 2020 reveal that timing entry points matters far less than recognizing when your portfolio needs protection. Those institutional investors who held 5-10% allocations during the financial crisis didn’t forecast the crash-they simply understood that gold serves a specific function when traditional assets fail simultaneously.

The lessons translate directly to your situation today. Gold belongs in your portfolio not as a growth engine but as insurance against the scenarios you genuinely fear: inflation eroding purchasing power, geopolitical instability disrupting markets, or currency debasement. The vehicle matters enormously-physically-backed ETFs deliver gold’s defensive characteristics without the storage costs and liquidity friction of physical bars, while mining stocks introduce leverage that undermines the stabilization benefit you’re seeking. Ray Dalio’s 5-15% framework provides a practical range, and most investors benefit from positioning at the lower end around 5-10%.

The current macro environment supports allocation: real interest rates remain compressed, geopolitical tensions persist, and central banks continue accelerating reserve diversification toward gold. We at Natural Resource Stocks provide expert analysis on macroeconomic factors affecting resource prices and geopolitical impacts on markets. Visit Natural Resource Stocks to access in-depth market analysis and expert commentary that helps you understand when gold allocation aligns with your portfolio’s risk management needs.