Nuclear energy is experiencing a genuine resurgence, and uranium mining stocks are positioned at the center of this shift. Global demand for nuclear power is climbing as countries prioritize clean energy and energy security.

At Natural Resource Stocks, we’ve analyzed the market dynamics driving this sector forward. This guide covers the opportunities, risks, and strategic factors shaping uranium investments today.

Where Uranium Demand and Supply Stand Today

Nuclear Capacity Expansion Drives Structural Demand

Nuclear energy accounted for roughly 9% of global electricity in 2024, and that share will expand significantly. The World Nuclear Association projects installed nuclear capacity will reach 746 gigawatts by 2040, more than doubling from approximately 398 gigawatts in 2025.

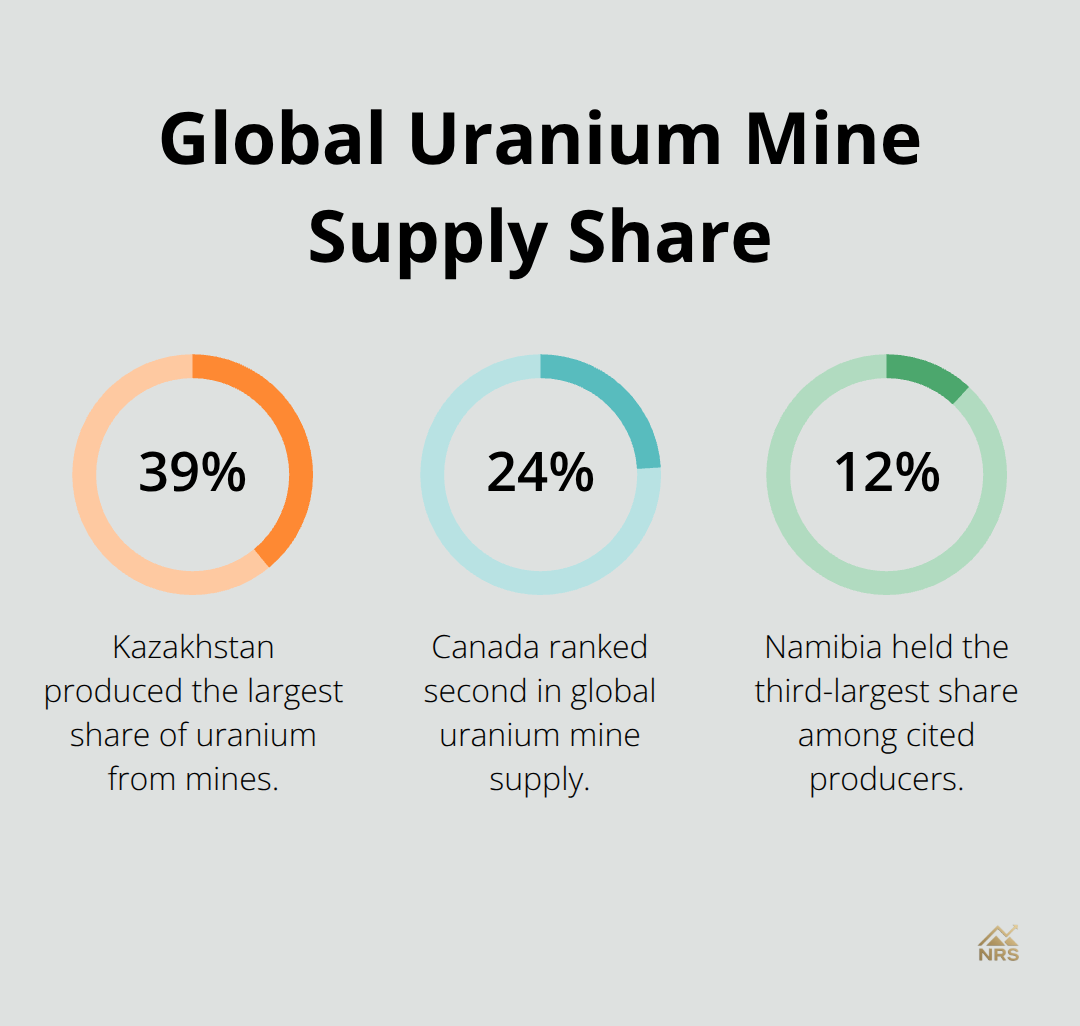

This expansion requires massive amounts of uranium fuel, and here’s where reality gets interesting: Kazakhstan produced the largest share of uranium from mines (39% of world supply), followed by Canada (24%) and Namibia (12%). This concentration signals sustained price pressure and opportunity for mining stocks.

Production Concentration and Resource Constraints

Four producers control the market: Kazakhstan leads global output, Canada ranks second, Namibia third, and Australia fourth. These four nations account for over 82% of global output. Australia holds roughly 28% of the world’s uranium resources-the largest reserve base globally-yet production remains constrained. The World Nuclear Association projects demand will expand to approximately 150,000 metric tons by 2040 from roughly 68,900 metric tons in 2025. This widening gap between supply and projected demand represents the fundamental driver behind uranium stock valuations.

Price Signals Reflect Market Tightness

Uranium hit just above 100 dollars per pound in January 2026, and as of April 29, 2026, spot prices stood at 87 dollars per pound, up 27.94% year-over-year and 3.69% in the past month alone. Long-term contract prices reached approximately 90 dollars per pound at the end of Q1 2026-the highest level since 2008. Trading Economics forecasts suggest uranium will reach 92.75 dollars per pound within 12 months. These price movements reflect genuine supply tightness rather than speculation.

Corporate and Policy Tailwinds Accelerate Demand

Meta signed agreements for up to 7.8 gigawatts of nuclear capacity to power AI services, while Microsoft secured agreements to renew reactors supplying over 800 megawatts for AI datacenter operations. Government deregulation on construction and permits for uranium converters and enrichers, combined with deals for new power plant construction, signals serious policy backing. Centrus and two other reactor and enrichment operators received approximately 2.7 billion dollars in contracts. Geopolitical risks-including sanctions on Russia’s nuclear fuel supply-create sustained upside pressure on prices.

The Multi-Year Supply Gap Creates Opportunity

Bringing new uranium mines online requires substantial capital and multi-year timelines, meaning the supply gap will persist into the 2030s. This structural tightness, paired with corporate and policy tailwinds, positions uranium mining stocks in a sector with genuine fundamental support. The combination of constrained supply, expanding demand, and government backing creates conditions where individual mining companies can capture significant value. Understanding which producers and developers will benefit most from this dynamic requires examining their operational performance and growth prospects.

Investment Opportunities in Uranium Mining Stocks

Established Producers Offer Stability Over Explosive Growth

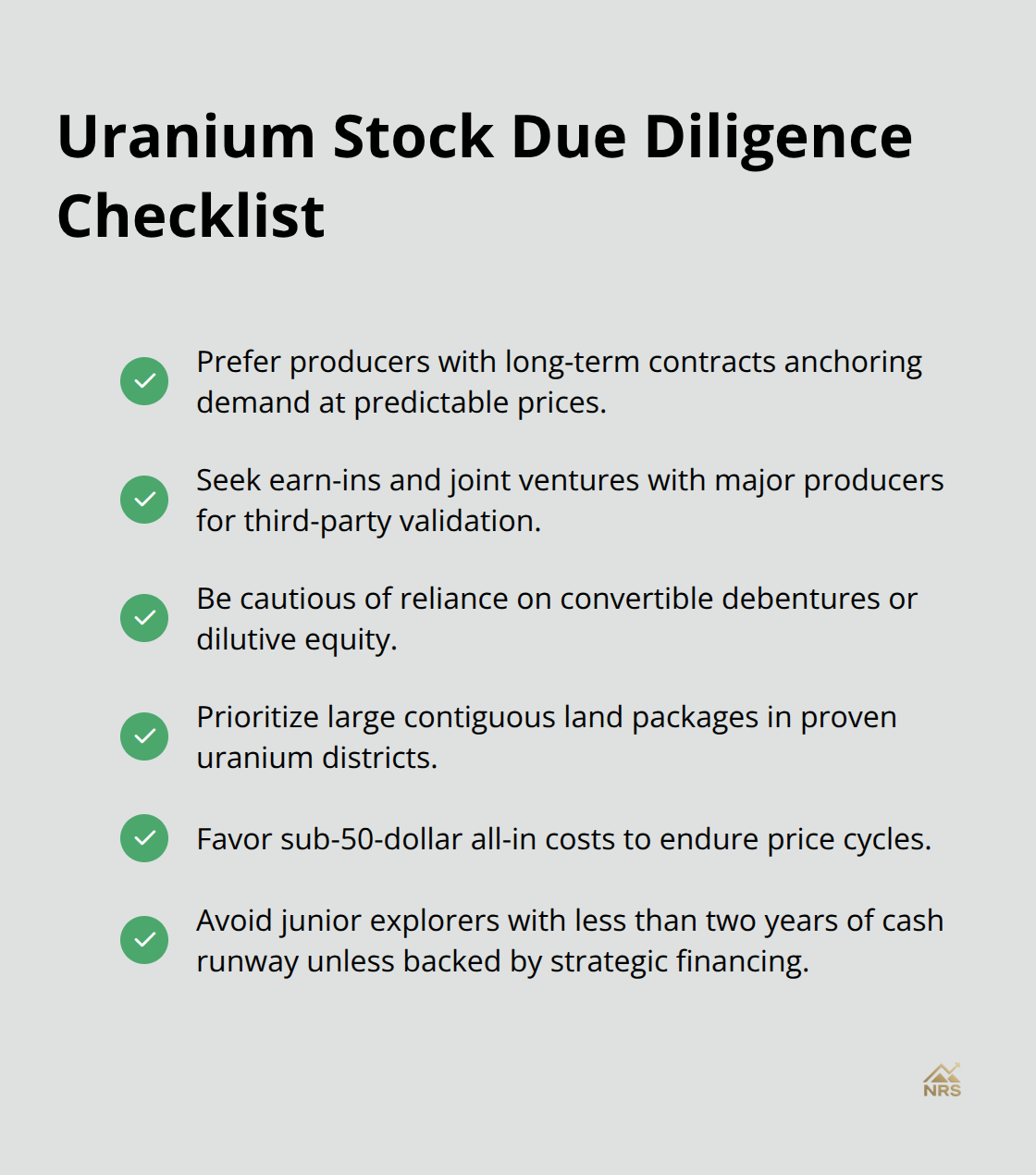

Cameco, Paladin Energy, Boss Energy, Energy Fuels, and Kazatomprom represent the most established uranium producers, and they warrant close examination because their operational track records and cost structures directly influence returns. Cameco operates the world’s largest high-grade uranium mines in the Athabasca Basin and benefits from long-term contracts that anchor demand at predictable prices. Paladin Energy operates in Namibia and Australia, providing geographic diversification that reduces concentration risk in Kazakhstan or Canada. These major producers offer relative stability compared to junior explorers, but they also carry lower upside potential because production capacity is already known and largely reflected in current valuations.

Emerging Developers Control the Real Upside

The real opportunity sits with emerging developers and explorers that control substantial land packages in prospective regions like the Athabasca Basin, where new discoveries are made on average every 18 months. Companies controlling over 200,000 hectares in proven uranium districts have meaningfully higher odds of converting exploration spending into economic discoveries. However, this path requires patience and capital discipline-successful exploration programs spend tens of millions before drilling begins, with geophysics and geochemistry work preceding expensive drilling campaigns. The distinction matters enormously: established producers generate cash flow today, while developers and explorers offer multi-year payoff horizons tied to discovery success and commodity price appreciation.

Financing Structures Reveal Asset Quality

Evaluating uranium stocks demands scrutiny of financing structures and management execution. Companies funded through earn-ins and joint ventures with major producers demonstrate third-party validation of their assets, whereas those relying solely on convertible debentures or dilutive equity raise flags about asset quality and sponsor confidence.

Management teams matter more in this sector than most because exploration success depends on geological judgment and capital allocation discipline over multi-year cycles. Review whether the company controls large contiguous land packages in districts with historical production or major discoveries-isolated claims in unproven regions represent speculation, not investment.

Cost Structure and Cash Runway Determine Survival

Long-term contract prices at 90 dollars per pound and spot prices near 87 dollars per pound create favorable economics for even marginal deposits, but this advantage erodes quickly if commodity prices decline. Companies with sub-50-dollar all-in costs will survive and profit through price cycles, while higher-cost operators face margin compression in downturns. Most critical: avoid junior explorers with less than two years of cash runway unless they’ve secured strategic partnerships or financing commitments, because uranium exploration timelines stretch far longer than most investors anticipate.

Research Intensity Pays Off in a Concentrated Market

The sector concentrates around roughly 20 producers, 20 developers, and 20 exploration companies-a small enough universe that focused research on financial statements, land positions, and management track records yields clearer insights than broad-brush sector exposure. This concentrated structure means that identifying which companies will capture value from the supply-demand tightness requires examining their specific operational advantages, financing health, and exploration productivity rather than betting on sector-wide tailwinds alone.

Policy Support and Geopolitical Risk Shape Uranium Economics

Government Commitment Translates to Sustained Demand

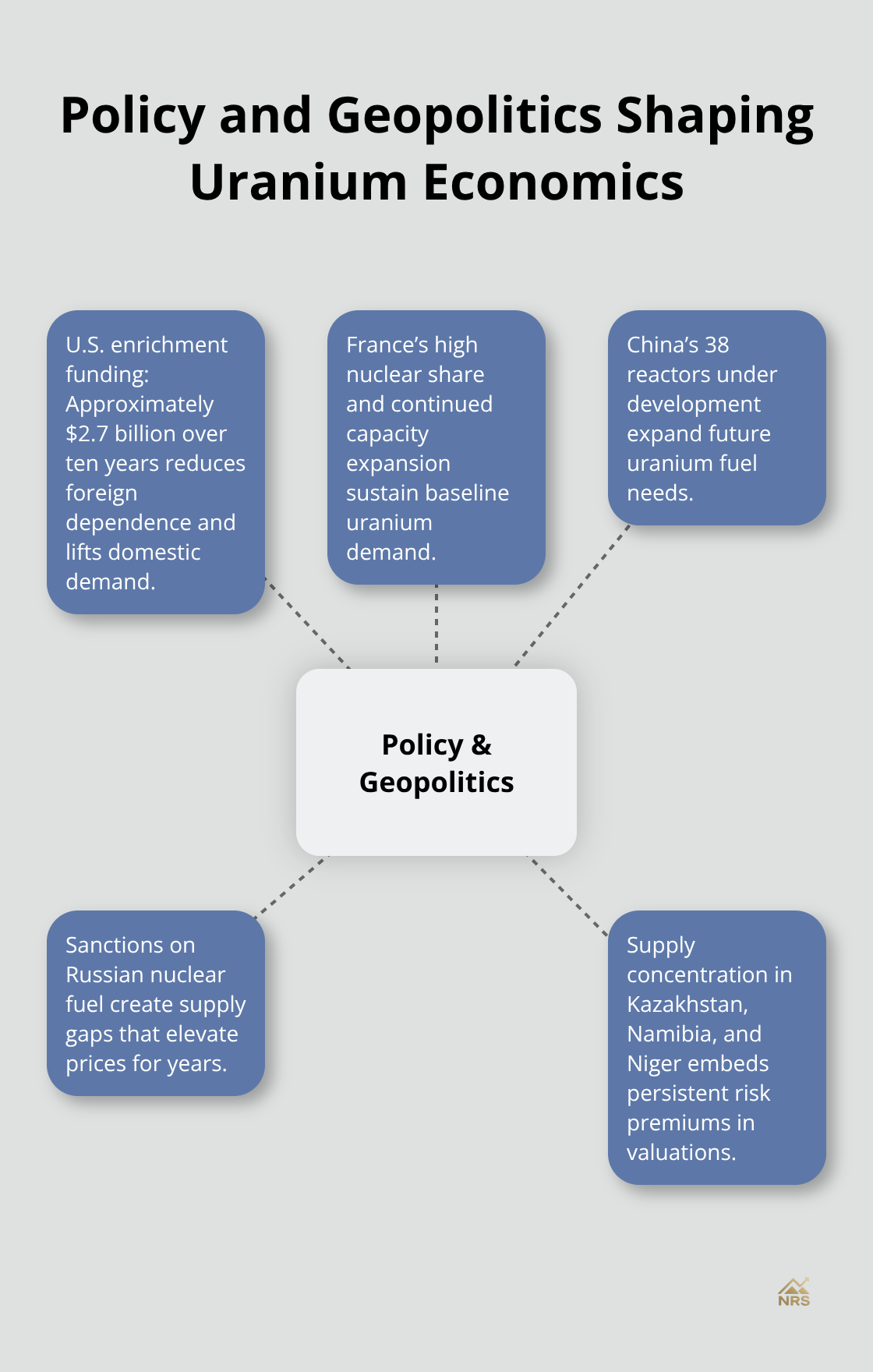

Government backing for nuclear energy has shifted from theoretical support to concrete action, and this matters far more for uranium stocks than most investors realize. The United States government awarded approximately $2.7 billion to strengthen domestic enrichment services over the next ten years, signaling serious commitment to reducing dependence on foreign fuel supplies. This spending directly increases demand for domestically sourced uranium and creates pricing floors that protect mining economics. France maintains the highest nuclear share of electricity generation globally and continues expanding capacity, while China leads construction activity with 38 reactors currently under development. These policy signals translate to sustained uranium demand that extends far beyond commodity cycles, anchoring long-term contracts at elevated prices and reducing downside risk for mining stocks.

Supply Concentration Creates Permanent Price Support

Geopolitical supply constraints operate as a permanent tailwind for uranium prices and mining company valuations. Sanctions on Russian nuclear fuel supply create immediate supply gaps that other producers must fill, and this disruption will not reverse quickly given the multi-year timelines required to bring new mines online. Kazakhstan produced 43 percent of global uranium supply in 2019 according to the World Nuclear Association, making it indispensable to global fuel supply chains, yet political instability in the region creates persistent uncertainty that keeps prices elevated. Namibia and Niger, which together supply roughly 20 percent of global uranium, face their own geopolitical risks that periodically disrupt production.

Resource Bases and Regulatory Barriers

Australia holds 28 percent of global uranium resources but operates under strict environmental regulations that slow new project development. This geographic concentration of supply in politically unstable or heavily regulated regions means supply disruptions will remain a feature of the market, not an anomaly.

For uranium stock investors, this reality means that commodity price declines will compress less severely than in other mining sectors because geopolitical risk premiums permanently support valuations.

Geographic Advantages Drive Valuation Premiums

Companies operating in stable jurisdictions like Canada, particularly those in the Athabasca Basin, command valuation premiums precisely because they avoid the political and regulatory risks that plague other major producing regions. Investors who prioritize operational stability over speculative upside should focus on producers and developers with assets in jurisdictions where policy frameworks support rather than obstruct uranium development.

Final Thoughts

The uranium market stands at an inflection point where structural demand, constrained supply, and government backing converge to create genuine investment opportunity. Established producers like Cameco and Paladin Energy generate cash flow from existing operations while capturing upside from higher prices and long-term contracts locked in at 90 dollars per pound. Emerging developers control exploration assets in proven districts where discoveries occur regularly, offering multi-year payoff potential tied to successful drilling and commodity appreciation.

Geopolitical concentration in Kazakhstan, Canada, and Namibia creates permanent price support because supply disruptions cannot be quickly remedied. This reality means uranium mining stocks will compress less severely during commodity downturns than peers in other mining sectors. However, this advantage does not eliminate risk-regulatory changes, exploration failure, financing challenges, and commodity price declines remain genuine threats to individual company valuations.

The strategic approach involves examining specific companies rather than betting on broad sector exposure. Scrutinize management track records, land positions in prospective regions, cost structures, and financing health. Visit Natural Resource Stocks for expert commentary and market insights on uranium mining stocks, where video content and analysis of geopolitical factors shaping resource valuations will help you conduct thorough research and maintain a long-term perspective.